GLOBAL ECONOMY

In the Global Economy, President Donald Trump announced a 90-day suspension of tariffs targeting dozens of countries, offering a temporary reprieve to global trading partners. However, this pause excludes China, which now faces a steep tariff hike from 104% to 125%. The decision came after over 75 nations reached out to negotiate trade terms following the initial rollout of tariffs. While the baseline 10% tariff on all imports remains in effect, the suspension provides a window for diplomatic discussions.

The annual Inflation rate in the US eased for a second consecutive month to 2.40% in March 2025, down from 2.80% in February. Month-on-month, it fell by 0.10% in March 2025, following a 0.20% increase in February. The annual Core Consumer Price Inflation rate in the United States, which excludes volatile items like food and energy, eased to 2.80% in March 2025, down from 3.10% in February. The decline in the Inflation rate was due to decreases in fuel prices and transportation costs.

The British economy grew by 0.50% in February, above the 0.10% forecast by economists. Mining led gains, as gold prices continued to rally. The British pound also climbed past £1/$1.30, after UK GDP data was released, five times the expected pace.

The Euro continued its rally, climbing above €1/$1.11, after the European Union announced a 90-day suspension of new tariffs on the U.S. to allow for trade negotiations supported by broad-based dollar weakness as markets continued to digest the escalating US-China trade war. On the monetary policy front, the European Central Bank (ECB) is widely expected to cut interest rates by 25bps this month.

The Yuan slipped to ¥7.31/$1 on Friday, as investors weighed escalating US-China trade tensions. China’s Ministry of Finance announced it will increase tariffs on American goods to 125% from the previous 84%, set to take effect on April 12. China’s retaliatory measures, including an 84% tariff on U.S. goods, have further strained relations, underscoring the complexities of the global trade landscape.

Next week in the US, investors will focus on key economic data releases, including the Export and Import levels of the US for the past month, following the ongoing trade war.

GLOBAL MARKETS

US stocks rallied on Friday, closing out a turbulent week as hopes for a potential US-China trade deal lifted investor sentiment. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices increased by 7.29%, 5.70% and 4.95% to 16,724.46, 5,363.36 and 40,212.71, respectively.

European stock markets reversed early gains to close lower, after a week dominated by trade tensions between the US and China, which reignited fears of a global recession and triggered a flight away from US assets. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices decreased by -1.13%, -2.34% and -1.30% to 7,964.18, 7,104.80 and 20,374.10, respectively.

Asian stocks dipped as concerns over a deepening Sino-US trade conflict weighed on sentiment. The Hang Seng index decreased by -8.47% to 20,914.69 while the Japanese Topix index fell by -0.61% to 2,466.91.

Next week, global markets are set to remain highly sensitive as Investors continue to monitor developments on the trade front.

DOMESTIC ECONOMY

Nigeria’s Oil Reserves Reach 37.28 Billion Barrels, Gas Reserves Hit 210.54 trillion cubic feet

The Nigerian Upstream Petroleum Regulatory Commission (NUPRC) announced that Nigeria’s crude oil reserves stand at 37.28 billion barrels and its gas reserves hit 210.54 trillion cubic feet (tcf) at the beginning of the year. This shows Nigeria’s commitment to maintaining its position as a key player in the global energy landscape, while also ensuring resource sustainability.

Nigeria Achieves Balance of Payments Surplus Driven by Economic Reforms

The country recorded its first balance of payments surplus in three years, a total of $6.83billion in 2024 compared to a $3.34billion deficit in the previous year. This is credited to a series of impactful reforms, including increased oil and gas production, the removal of fuel subsidies, and the adoption of a free-floating naira policy. These measures have strengthened economic fundamentals and stabilized the nation’s external accounts. Key drivers of the surplus include a $17.20billion surplus in the capital and financial account, fueled by increased gas and non-oil exports and a reduction in imports, particularly petroleum imports, which declined by 23%. Remittance inflows also surged, rising by 8.90% to $20.90billion, with inflows from International Money Transfer Operators (IMTOs) increasing by 43.50% to $4.73billion.

Fitch Upgrades Nigeria’s Credit Rating Amid Economic Reforms

Fitch Ratings has upgraded Nigeria’s credit rating to ‘B’, reflecting increased confidence in the country’s economic reforms and policy direction. This marks a significant improvement in Nigeria’s financial standing, though it remains within the speculative-grade category. The upgrade is attributed to key reforms implemented since mid-2023, including exchange rate liberalization, tighter monetary policies, and the removal of fuel subsidies. These measures have enhanced policy credibility, reduced economic distortions, and bolstered macroeconomic stability.

We await the release of the Inflation data for March 2025 by the National Bureau of Statistics (NBS).

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity opened the week positive with a surplus of ₦906.85billion. However, it declined mid-week due to CBN FX settlements and NTB Auction debits, closing at ₦303.04billion. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) increased by 8bps and 10bps to 26.58% and 26.96%, respectively.

The Nigerian Treasury Bills (NTB) market average yield increased by 5bps to 21.04% against 19.99% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor increased by 1bps and 4bps, to 18.99% and 19.04% respectively, while the average yield for the Long-tenor Bonds decreased by 18bps to 17.65%.

We anticipate cautious trading next week as investors closely watch the Fixed-Income Yield direction.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization depreciated by 0.90% and 0.67% to close the week at 104,563.34 and N65.71trillion respectively from 105,511.89 and ₦66.15trillion the previous week.

A total turnover of 2.09 billion shares worth ₦52.97billion in 64,612 deals was traded this week by investors on the floor of the Exchange in contrast to a total of 1.18 billion shares valued at ₦28.87billion that exchanged hands last week in 42,397 deals. On a sectoral basis, the Banking, Industrial Goods, Insurance, Consumer Goods and Oil and Gas indices closed negative, at -2.20%, -0.26%, -4.57%, -0.761% and -0.50%, respectively.

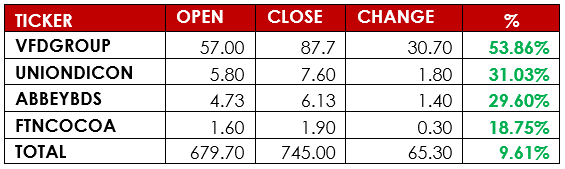

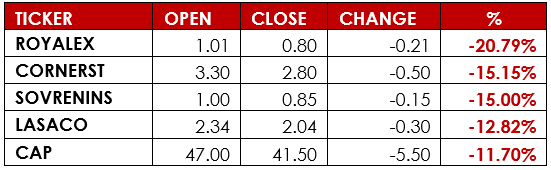

Notable gainers this week were VFD Group and Union Dicon Salt Plc, while notable losers were Royal Exchange Plc and Cornerstone Insurance Plc.

LISTING

First HoldCo Plc additional 5,982,548,799 ordinary shares of 50 Kobo each at N25.00 per share were listed on the Nigerian Exchange Limited (NGX) on April 7, 2025. This arose from First HoldCo Plc’s Rights Issue, which was 125.46% subscribed. Following the listing, the company’s total issued and fully paid-up shares increased from 35.89 billion to 41.88 billion ordinary shares.

We expect cautious trading in the Equities market amid ongoing global market conditions.

CURRENCY

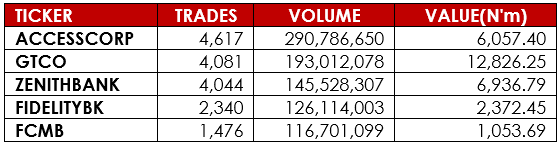

TOP TRADES BY VOLUME

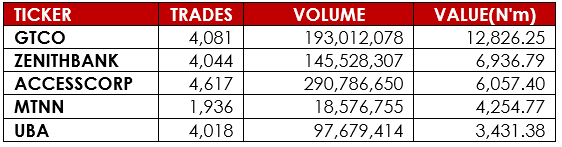

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, BusinessDay, Alpha10 Research