GLOBAL ECONOMY

In the US, President Trump announced sweeping tariffs ranging from 25% to 50% on over 20 countries, including key partners like Japan, South Korea, Canada, and Brazil, with copper and pharmaceuticals among the most heavily targeted sectors and an additional 10% tariff on countries who align themselves with the “Anti-America Policies” of the BRICS, effective from August 1st 2025. Initial jobless claims fell to 227,000, with continuous claims rising by 10,000 to 1,965,000.

UK economy showed signs of strain with the Pound weakening to £1/$1.354, driven by economic concerns and global trade tensions, especially following tariffs on UK goods. Manufacturing output fell to -1.00% from -0.70% month-on-month with Industrial production also declining to -0.90% from -0.60%, while construction output dropped 0.60% monthly but rose 1.20% year-on-year. The services sector offered a slight rebound, growing 0.10%, led by a 3% surge in IT and consultancy. The trade deficit narrowed to £5.70billion in May as exports rose 1.20% to £74.31billion, driven by fuel shipments to the EU and chemical exports to the U.S while imports remained nearly flat.

The Euro declined to €1/$1.17, weighed down by renewed trade tensions between the US and the EU. Meanwhile, trade negotiations with the UsS remain tense but ongoing, with EU officials hopeful for a deal before the extended August 1st 2025, deadline. Talks include potential protections for the EU auto industry, such as tariff cuts and export-based credits.

The offshore Yuan strengthened past ¥7.16/$1, supported by a strong People’s Bank of China’s (PBoC) fixing the exchange rate at 7.15 supporting the Yuan and limiting depreciation. Foreign exchange reserves rose by $32.20billion to $3.32trillion, while gold reserves increased to 73.90 million ounces. Producer prices fell 3.60% year-on-year in June, while consumer inflation edged up 0.10% and core inflation rose to 0.70%. China also retaliated against the EU’s procurement restrictions by banning government purchases of EU medical devices over ¥45million and tightening import rules.

Investors globally will monitor developments on the US trade policy as they continue to affect the outlook of the global economy.

GLOBAL MARKETS

Last week, US stocks closed lower following Trump’s announcement of a 35% tariff on Canadian imports and threats of broader global tariff hikes. Compared to last week, the Dow Jones, Nasdaq and S&P indices decreased by -1.02%, -0.31% and -0.08% to close at 44,371.51, 20,585.53 and 6,259.75 respectively.

In the UK and across Europe, major stocks slipped amidst trade tension however closing positive. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices increased by 1.34%, 1.73% and 1.97% to 8,941.12, 7,829.29 and 24,255.31 respectively.

The Asian stock market closed mixed last week with major stocks trimming gains as Investors sentiment remained cautious. The Hang Seng increased by 0.93% to 24,139.57 while the Topix indices decreased by -0.17% to 2,823.24 respectively.

This week, Investors will look ahead to trade data, macro-economic data released globally to further guide sentiments and Investment decisions.

DOMESTIC ECONOMY

JUNE PMI: CBN Warns of Inflation Risk as Input Costs Outpace Output Prices Across Key Sectors

The Central Bank of Nigeria (CBN) has flagged rising input costs as a potential trigger for future inflation, citing June 2025 PMI data showing businesses especially in agriculture are absorbing unsustainable cost pressures. The agriculture sector recorded the highest input-output price gap at 9.80 index points, while the composite Purchasing Managers Index (PMI) stood at 52.30, marking six straight months of economic expansion. Despite growth across Industry (51.40), Services (51.30), and Agriculture (55.20), the CBN warns that continued cost absorption may soon lead to price hikes, fueling inflationary pressures.

CBN Sets July 14 Deadline for Banks’ Capital Restoration Plans as Forbearance Era Ends

Nigerian banks are racing to meet the CBN’s July 14 2025, deadline to submit Capital Restoration Plans, marking the end of the COVID-era regulatory forbearance. The directive targets banks with credit exposure and Single Obligor Limit breaches, requiring detailed strategies for restoring compliance, including CAR calculations, risk reduction, and cost optimization. GTCO and Stanbic IBTC have already exited the regime, while others like UBA, Fidelity, and FCMB are finalizing submissions. The move aims to strengthen capital buffers and ensure long-term financial stability across the sector.

Dangote Refinery Cuts Petrol Price to ₦820/Litre, Launches CNG Tanker Distribution Initiative

Dangote Petroleum Refinery has reduced the ex-depot price of petrol from ₦840 to ₦820 per litre, marking a ₦60 drop within two weeks. The price cut, effective immediately, is expected to lower pump prices below ₦885/Litre, easing consumer costs. The refinery also plans to begin free distribution of petrol and diesel from August 15 using 4,000 new CNG-powered tankers, reinforcing its push for cleaner energy logistics. Located in Lagos’ Lekki Free Zone, the $20billion facility is Africa’s largest and aims to stabilize Nigeria’s fuel supply and reduce import dependence.

UNCTAD: Nigeria, Developing Economies Lag in Q1 2025 Trade and Digital Market Growth

Nigeria and other developing economies saw a decline in imports in Q1 2025, while developed nations led global trade growth with a 4% import surge, according to the United Nations Conference on Trade and Development’s (UNCTAD’s) July 2025 Global Trade Update. Global South–South trade also weakened, excluding East Asia. Despite a projected $300billion global trade rise in H1 2025, developing countries remain sidelined in the digital economy due to poor internet access and infrastructure. The report warns of slower trade growth ahead.

This week, Investors will watch out for the July 14th CBN capital plan deadline and the CPI release by NBS to further guide sentiments.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System Liquidity stayed tight during the week closing in a repo of -₦118.17billion despite a ₦301.94billion injection from the Treasury Bills Maturities. Short-term rates closed higher, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) increased by 467bps and 475bps to 31.50% and 32.17% respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased further by 115bps to 16.93% last week. In the Bonds market, the average yield for the short-tenor, mid-tenor and long-tenor bonds decreased by 33bps, 89bps and 11bps to 17.67%, 16.82% and 16.20% respectively.

We anticipate cautious to bullish sentiments to persist in the market next week.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 4.26% and 4.54% to close the week at 126,149.59 and ₦79.80trillion respectively, compared to 120,989.66 and ₦76.34trillion last week.

A total turnover of 5.39 billion shares worth ₦107.80billion in 134,390 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 5.47 billion shares valued at ₦108.10billion that exchanged hands last week in 118,570 deals.

On a sectoral basis, the Banking, Insurance, Industrial Goods and Consumer Goods indices closed positive at 12.49%, 13.83%, 2.94%, 2.18%, while Oil and Gas index closed negative at -0.72%.

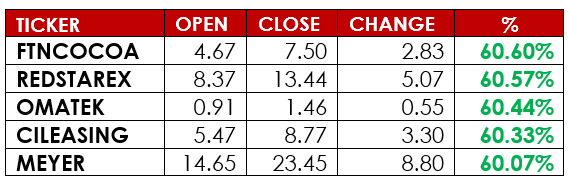

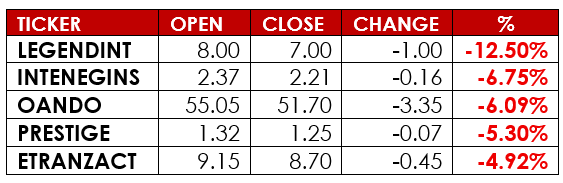

Notable gainers this week were FTN Cocoa Processors PLC and Red Star Express PLC, while notable losers were International Energy Insurance PLC and Legend Internet PLC.

This week, Investors will watch out for corporate actions release even as Nigeria banks gear up to submit their Capital Restoration Plans to CBN.

CURRENCY

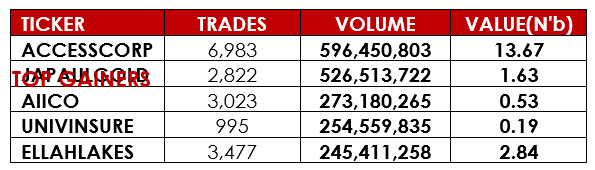

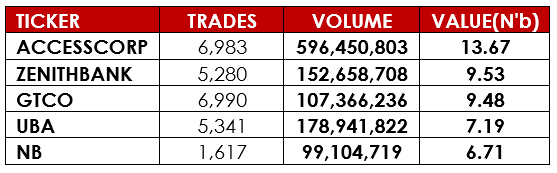

TOP TRADES BY VOLUME

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.