GLOBAL ECONOMY

The US annual Inflation rate rose for the second consecutive month to 2.70% in November 2024 from 2.60% in October. The Consumer Price Index increased 0.30% month-on-month in November 2024, slightly above October’s 0.20%, while core inflation remained unchanged month-on-month and year-on-year at 3.30% and 0.30% respectively. The Initial Jobless Claims for the week rose by 17,000 to 242,000 above market expectations that they would fall to 220,000.

The UK’s trade deficit increased to £3.72billion in October 2024, from £3.46billion in September. Imports rose 1.30% to £72.60billion, while exports grew by 1.00% to £68.88billion. Goods imports rose by 5.80%, primarily due to a £0.50billion increase in imports of machinery and transport equipment from the EU. Manufacturing Production and Industrial Production in the UK both fell 0.60% month-on-month in October 2024 as the British economy contracted by 0.10% month-over-month in October, following a similar decline in September and falling short of market forecasts of a 0.10% expansion.

The European Central Bank (ECB) has decided to cut rates for the fourth time this year. The Key Interest Rate was reduced by 25 bps in December 2024, as expected, from 3.40% to 3.15%. This move reflects a more favorable inflation outlook and improvements in monetary policy implementation. The ECB also cut its Key Deposit Rate by 25bps to 3.00% in its final meeting of 2024, as well as the Key Marginal Lending Rate by 25bps to 3.40%.

China’s annual inflation rate unexpectedly fell to 0.20% in November 2024 from 0.30% in the previous month, falling short of market forecasts of 0.50% and marking the lowest figure since June. This reduction highlighted mounting deflation risks in the country despite recent stimulus measures from Beijing and the Central Bank’s supportive monetary policy stance. China’s trade surplus surged to $97.44billion in November 2024 from $69.45billion in the same period last year, surpassing expectations of $95billion.

We await the Federal Reserve’s (Fed) decision next week concerning the interest rate cuts at its last meeting for the year.

GLOBAL MARKETS

The US stock market showed mixed performance, with concerns over the Federal Reserve’s upcoming policy decision and economic conditions limiting further gains, given the rise in the Inflation rate for November. The Nasdaq index closed positive, increasing by 0.73% to 21,780.25, while the S&P 500 and Dow Jones indices fell by -0.64% and -1.82% to 6,051.09 and 43,828.06.

Stock prices in the UK slipped on Friday, reversing earlier gains, after UK GDP data showed the economy contracted by 0.10% in October. This unexpected decline marked the second straight monthly drop and fell short of expectations for modest growth. The weak data drove hopes for earlier rate cuts from the Bank of England next year. Consumer confidence also remained down in December, with households cautious about spending on costly items ahead of the holidays. The London’s Financial Times Stock Exchange (FTSE) 100 and Cotation Assistée en Continu (CAC) 40 indices closed negative, decreasing by -0.10% and -0.23% to 8,300.33 and 7,409.57 while the Germany’s Deutscher Aktien (DAX) index increased by 0.10% to 20,405.92.

Asian indices declined slightly on Friday, albeit at higher levels than the previous week, following a high-level policy meeting where Chinese leaders, led by President Xi Jinping, reaffirmed a recent shift in economic strategy, highlighting plans to boost growth. However, the policy announcements failed to impress investors amid a lack of details on the size of potential stimulus considering persistent economic challenges and the ongoing threat of U.S. tariffs. The Hang Seng and Topix indices increased by 0.53% and 0.71% to close at 19,971.24 and 2,746.56, respectively.

We expect cautious trading in the Global Equities market next week, as investors await the Fed’s decision regarding rate cuts.

DOMESTIC ECONOMY

Nigeria’s money supply (M3) dropped to ₦107.66trillion in October 2024, reflecting a 1.60% month-on-month decrease from ₦109.41trillion in September 2024 according to the Money and Credit statistics of the Central Bank of Nigeria (CBN). This is the second decline recorded in 2024, as the government’s tightening fiscal measures continue to impact liquidity in the economy. Narrow money (M1), which comprises the most liquid forms of money such as currency in circulation and demand deposits, dropped by 3.40% to ₦34.65trillion in October 2024 from ₦35.86trillion in September 2024.

Nigeria’s total Capital Importation for Q3 2024 saw a 51.90% decline from the previous quarter, falling to $1.25billion. This decline, compared to the $2.60billion recorded in Q2 2024, highlights a sharp contraction in foreign investments despite an overall annual increase of 91.35% from Q3 2023. While Nigeria’s capital importation showed substantial growth year-on-year, there was a notable decline in inflows compared to the preceding quarter.

The Nigeria Customs Service (NCS) has revealed that Nigeria earned $1.90billion from non-oil exports between January and November 2024. The announcement highlights progress in the country’s economic diversification efforts. According to the report, a total of 27,595 containers were exported during the 11-month period, consisting of agricultural products, manufactured goods, solid minerals, and other items. The report noted that the Free on Board (FOB) value of these exports amounted to $1.90trillion, showcasing a steady rise in the contributions of non-oil sectors to Nigeria’s export revenues.

We await the release of the Inflation data for November 2024 from the National bureau of Statistics (NBS) on Monday, 16th December 2024.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity was tight this week, worsening after the OMO auction and NTB auction settlement, as Banks depended on the CBN’s lending facility. The liquidity position closed at -₦1.50trillion this week from ₦632.38billion last week. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) increased by 4.87% and 4.75% to 32.54% and 32.92%, respectively.

The Federal Government offered ₦275.71billion at its Treasury Bills Auction which held this week on Wednesday, 11th December 2024. Total subscription was ₦907.85billion, with a total allotment of ₦527.84billion as the 364-day stop rate decreased by 13bps to 22.80%, while the 91-day and 182-day bills remained the same at 18.00% and 18.50% respectively.

We expect the interbank rates to remain at the same levels barring any significant inflow.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 1.19% to close at ₦60.24trillion from ₦59.53trillion and 99,378.06 from 98,210.75 the previous week.

A total turnover of 2.73 billion shares worth ₦49.85billion in 43,298 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 3.89 billion shares valued at ₦87.75billion that exchanged hands last week in 43,868 deals. On a sectoral basis, the Banking, Insurance, Consumer Goods and Oil and Gas indices all closed positive at 0.16%, 5.52%, 1.01% and 7.61%, respectively. The Industrial Goods index was the sole loser, closing at -0.60%.

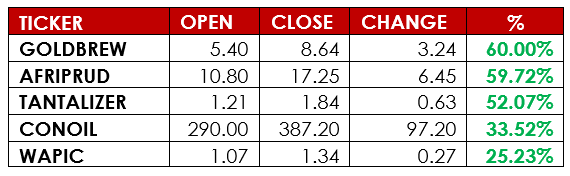

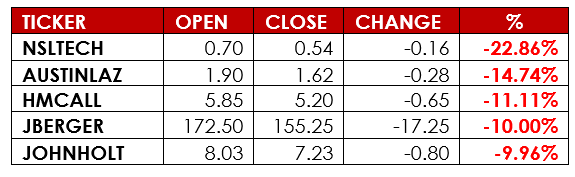

Notable gainers this week were Golden Guinea Breweries Plc and Africa Prudential Plc, while notable losers were Secure Electronic Technology Plc and Austin Laz & Company Plc.

We expect the mixed sentiments in the Equities market to persist next week.

CURRENCY

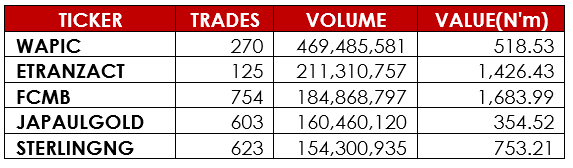

TOP TRADES BY VOLUME

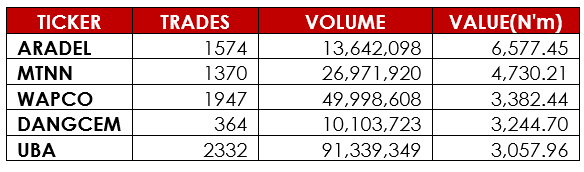

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research