GLOBAL ECONOMY

US and China’s Senior Government Officials met in London last week to begin a new round of talks signaling an easing in the trade wars as they reach a framework for implementing the Geneva agreement. The US annual Inflation rate rose to 2.40% in May with food, transportation, and vehicle prices edging up, as shelter costs dipped and energy prices continued to fall while core inflation held steady at 2.80% lowest since 2021. Initial jobless claims in the US held steady at 248,000, despite expectations for a drop while continuing claims surged to 1.96 million, with claims from Federal Employees going up amid recent Government layoffs tied to the Department of Government Efficiency (DOGE). The US budget deficit also fell to $316billion, driven by a surge in customs duties to $23billion, due to the new tariffs.

The British Pound slipped to £1/$1.35, as tensions escalated between Israel and Iran. The UK economy shrank by 0.30% month-on-month in April, driven by a rise in Stamp Duty Tax, and the impact of US tariffs. The UK trade deficit widened sharply to £7.03billion, as exports fell by 3.40% and imports rose by 1.00%. The UK unemployment rate rose by 4.60% largely linked to the slower wage growth following payroll tax hikes and a low 6.70% increase in the national minimum wage.

The Eurozone’s trade surplus shrank to €9.90billion in April, below €37.30billion in March, largely due to a significant decline in the chemicals sector surplus, which fell from €42.80billion to €22.10billion, Exports declined 1.40% year-on-year to €243billion, led by steep falls in mineral fuels (-25.3%) and machinery and transport equipment (-5.60%), while total imports edged up 0.10% to €233billion, driven by higher purchases of chemicals (+6.20%), food and drink (+6.80%). Eurozone industrial production also fell by 2.40% month-on-month, reversing March’s equally strong gain of 2.60%.

The Offshore Yuan slipped to ¥7.18/$1 on Friday, as Investors flocked to the US Dollar amid heightened geopolitical tensions. China’s consumer prices fell by 0.10% year-on-year and 0.20% month-on-month in May 2025, underscoring persistent deflationary pressures amid weak domestic demand, trade tensions with the US, and job market concerns. Meanwhile, core inflation rose to 0.60%, the highest since January, suggesting some underlying price stability when excluding food and energy. China’s trade surplus surged to $103.22billion, beating expectations and marking a sharp rise from $81.74billion a year earlier. The increase was fueled by a 4.80% rise in exports to $316.10billion and a 3.40% drop in imports to $212.90billion.

Next week, geopolitical tensions and economic developments will be closely monitored, especially in the Middle East, amid fears of escalation and changes in tariff wars.

GLOBAL MARKETS

Last week, US stocks closed sharply lower on Friday as risk appetite faded after Iran denounced Israel’s airstrikes as a “declaration of war” and responded with missile attacks late Friday. Compared to last week, the Dow Jones, S&P 500 and Nasdaq indices decreased by -1.32%, -0.39% and -0.63% to close at 42,197.79, 5,976.97 and 19,406.83 respectively.

In the UK and across Europe, major stocks fell following the tensions in the Middle East sparking a broad-based sell-off across global equity markets. The London’s Financial Times Stock Exchange (FTSE) 100 indices increased marginally by 0.14% to 8,850.63, while the France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices decreased by -1.54% and -3.24% to 7,684.68 and 23,516.23 respectively.

The Asian stock market was laced with uncertainty this week as geopolitical risks weighed on global investors, thus, stocks struggled for clear direction. The Hang Seng index increased by 0.42% to 23,892.56 while the Topix index decreased by -0.46% to 2,756.47.

We expect cautious trading this week as global Investors adopt a cautious approach, navigating geopolitical tensions, monetary decisions, and economic data to be released next week.

DOMESTIC ECONOMY

World Bank Holds Nigeria’s 2025 Growth at 3.60% Amid Global Trade Turmoil

Despite mounting global trade tensions and a downgraded global growth outlook, the World Bank has maintained its 2025 GDP growth forecast for Nigeria at 3.60%, up from 3.40% in 2024. The services sector, particularly Financial Services and ICT, remains the primary growth engine, while the Industrial Sector continues to be weighed down by weak oil output. The Bank credited Nigeria’s bold reforms including the floating of the naira and fuel subsidy removal for improving fiscal health, boosting state revenues, and attracting investment. Inflation is expected to decline gradually, supported by tight monetary policy, though it remains above target. Overall, Nigeria is seen as weathering global shocks better than many peers, with growth projected to average 3.80% in 2026–2027.

Nigeria’s Trade Surplus Hits ₦5.17trillion in Q1 2025 as Non-Oil Exports Surge

Nigeria recorded a ₦5.17trillion trade surplus in Q1 2025, the highest in nearly two years driven by a 7% drop in imports and a rise in non-oil exports, which reached ₦3.17trillion, their largest share of total exports in over a year. While crude oil remained dominant, its value slipped by over ₦800billion to ₦12.96trillion from ₦13.78trillion in Q4 2024. In contrast, agricultural exports soared 65% year-on-year to ₦1.70trillion, led by cocoa beans, cashew nuts, and sesame seeds. Other strong performers included urea, LNG, and cocoa-based products, reflecting the government’s push for export diversification. India topped the list of export destinations, followed by the Netherlands, US, France, and Spain.

Nigeria’s Pension Assets Hit ₦23.32trillion in March 2025, Driven by FGN Securities and Diversified Investments

Nigeria’s pension fund assets rose to ₦23.32trillion in March 2025, from ₦15.58trillion in March 2023, marking an 18.06% year-on-year increase and a modest 0.27% gain from February. The growth was fueled by higher pension contributions and strong performance in Federal Government securities, which now account for over 62% of total assets. Non-traditional investments like mutual funds, REITs, and commercial papers posted double and triple-digit gains. Retirement Savings Account RSA membership rose to 10.69 million, reflecting steady participation.

NNPC Reports ₦748 Billion Profit in April, Advances Key Gas Projects

The Nigerian National Petroleum Company Limited (NNPC Ltd) posted a profit after tax of ₦748 billion and revenue of ₦5.89trillion in April 2025, according to its latest monthly report. Crude oil and condensate production averaged 1.60 million barrels per day, while natural gas output reached 7,473 million standard cubic feet per day (mmscf/d).

We await the release of the Consumer Price Index (CPI) and Inflation figures by NBS and the imminent Q1 2025 GDP release by the Central Bank of Nigeria (CBN).

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System Liquidity stayed robust during the week with ₦363billion inflows from OMO, NTB Maturities and derivation funds. Consequently, short-term rates remained stable, as the Open Repo Rate (ORR) remained unchanged at 26.50% while the Overnight Rate (O/N) increased slightly by 3bps to close at 26.99% respectively.

The Nigerian Treasury Bills (NTB) market average yield increased by 232bps to 21.11% last week. In the Bonds market, the average yield for the short-tenor bond increased by 1bp to 19.24%, while mid-tenor bond decreased by 4bps to 18.98% and long-tenor bond remained unchanged at 17.70% respectively.

We expect trading activities to pick up as sentiments improved also with the Treasury Bills Auction happening on Wednesday where the DMO is offering ₦162billion against ₦27billion Maturing.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 0.71%to close the week at 115,429.54 and ₦72.79trillion respectively, compared to 114,616.75 and ₦72.28trillion last week.

A total turnover of 2.06 billion shares worth ₦51.02billion in 65,016 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 3.21 billion shares valued at ₦76.35billion that exchanged hands last week in 64,156 deals.

On a sectoral basis, the Banking index closed flat at 0.00%, Insurance and Oil and Gas indices both closed negative at -0.11% and -1.22%, while Consumer Goods and Industrial Goods indices closed positive at 1.32% and 1.21% respectively.

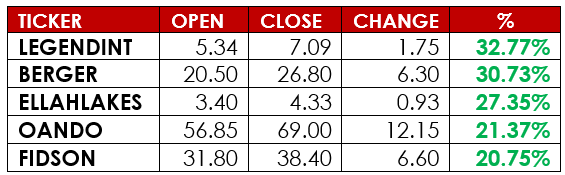

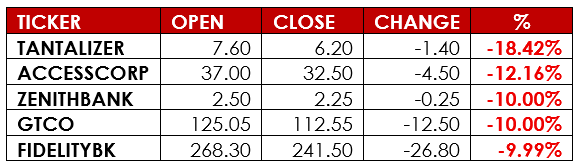

Notable gainers this week were Legend Internet PLC and Berger Paints PLC, while notable losers were John Holt PLC and Industrial & Medical Gases Nigeria PLC.

We anticipate cautious to mild-bullish trading in the Equities market next week as investors monitor the global geopolitical tension and its effect.

CURRENCY

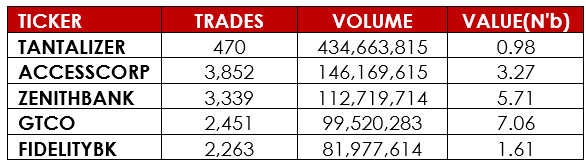

TOP TRADES BY VOLUME

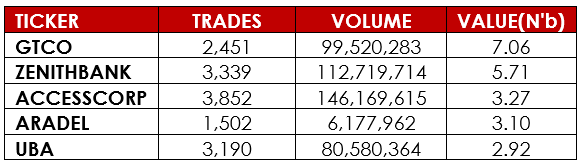

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.