GLOBAL ECONOMY

The yield on the US 10-year Treasury note rose to 4.54% on Friday as traders assessed President Trump’s trade policies and key economic data within the week. Trump signed a directive instructing the US Trade Representative and Commerce Secretary to propose new country-specific tariffs, delaying implementation till April 2025. The annual inflation rate in the US increased to 3.00% in January 2025, compared to 2.90% in December 2024 and above market forecasts of 2.90%, indicating slow progress in curbing inflation. The annual core consumer price inflation rate in the United States also increased to 3.30% in January 2025, from 3.20% in the prior month and surpassing market expectations of 3.10%.

The British economy expanded by 0.10% quarter-on-quarter in Q4 2024, following no growth in Q3, and beating forecasts of a 0.10% contraction, while expanding by 0.90% for the year 2024, compared to 0.40% in 2023, led by a 1.30% growth in the services sector. Month-on-month, the British economy expanded 0.40% in December 2024, compared to a 0.10% rise in November and well above forecasts of 0.10%.

The Eurozone’s annual GDP growth rate was 0.90% in Q4, 2024, unchanged from the previous quarter. This marked the expansion since early 2023, driven by lower borrowing costs and easing inflationary pressures. Spain led with a 3.50% growth, followed by the Netherlands (1.80%), France (0.70%), and Italy (0.50%). In contrast, Germany, the Eurozone’s largest economy, remained in contraction, shrinking by 0.20%.

China’s 10-year government bond yield rose to around 1.65%, as investors digested the People’s Bank of China’s (PBoC) latest policy signals. The Central Bank pledged to adjust monetary policy as needed to support economic growth, emphasizing liquidity management and targeted measures to stabilize the financial system. Meanwhile, US President Donald Trump delayed the implementation of reciprocal tariffs, easing concerns about escalating trade tensions. In response, Chinese producers are diversifying away from the U.S. market, focusing on Europe and emerging markets, which could lead to price wars abroad and economic challenges at home.

Next week in the US, investors will focus on the release of the Federal Open Market Committee (FOMC) minutes and speeches by several Federal Reserve officials in the US.

GLOBAL MARKETS

This week in the US, markets held steady after a volatile week of policy shifts, including new tariff plans from President Trump and Ukraine peace talks. Investors welcomed a delay in tariffs, helping stocks make weekly gains. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices increased by 2.90%, 1.47% and 0.55% to 22,114.69, 6,114.63 and 44,564.08, respectively.

European stocks closed lower on Friday, easing from the record highs touched during the week but higher than last week as markets continued to assess the likelihood of armistice in Ukraine this year and the impact of potential tariffs from US President Trump. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices increased for the second time in a row to 0.37%, 3.33% and 2.58% to 8,732.46, 8,178.54 and 22,513.42, respectively.

After the People’s Bank of China pledged to support the economy with loose monetary policy and the delay in tariffs, Asian stocks closed higher this week. The Hang Seng index increased by 7.04% to 22,620.33 while the Japanese Topix index rose by 0.80% to 2,759.21.

We expect traders to focus on the directions of the FOMC minutes and await the release of further policies from the Trump administration.

DOMESTIC ECONOMY

The Nigerian Export Promotion Council (NEPC) stated that Nigeria’s trade volume in 2024 reached 7.2 metric tons, with a 20.70% increase in value, totaling $5.45billion. Dr. Nonye Ayeni, Executive Director of NEPC, disclosed this on Monday during the Ministry of Industry, Trade, and Investment’s retreat in Abuja. She highlighted an export expansion to 126 countries, signaling Nigeria’s export progress. France emerged as the top destination for Nigerian exports in 2024, accounting for 11.09% of the total export value, followed by Spain (10.56%), the Netherlands (8.85%), India (8.41%), and the United States (6.84%). These countries primarily imported Nigeria’s crude oil and gas products, reflecting strong energy trade ties.

The Central Bank of Nigeria (CBN)’s economic report for November 2024 showed that the net Foreign Exchange (FX) flows through the economy rose to $5.95billion as of November 2024, compared to $4.86billion in October 2024 and $1.70billion in November 2023. The net FX flow indicates the difference between the total inflows and outflows of foreign exchange. Aggregate foreign exchange inflow declined to US$8.40billion, from US$9.15billion in October 2024. Similarly, foreign exchange outflow decreased to US$2.45billion, from US$4.29billion in the previous month.

The Senate has passed a harmonized 2024 budget Appropriation Bill totaling ₦54.99trillion for a third reading. The National Assembly also increased the bill by about ₦746billion, moving the budget from the proposed ₦54.20trillion. The budget was passed on Thursday by Godswill Akpabio, the Senate President, after the submission of the budget report by Olamilekan Adeola, the Chairman, of the Senate Committee on Appropriation.

We anticipate CBN’s monetary policy decisions from the upcoming Monetary Policy Committee (MPC) meeting, scheduled to be held on the 19th and 20th of February 2025.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity remained deeply negative throughout the week due to persistent illiquidity amidst absence of inflows, opening at -₦3.10trillion on Friday, compared to -₦315.94billion last week. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) increased by 3bps and 5bps to 32.45% and 32.80%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 45bps to 22.07% against 22.52% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor and Long-tenor Bonds decreased by 52bps, 21bps and 2bps to 20.54% and 20.29% and 18.71%.

The CBN carried out an OMO auction this week, offering two subscription tenors: a 355-day bill and a 362-day bill with an initial offer size of ₦300billion each. Investor interest was tilted to the longer-duration 362-day bill, where total subscriptions rose to ₦1.50trillion and the 355-day bill saw a lower subscription level of ₦415.85billion. The auction was oversold, with an allotment of ₦993billion for the 362-day bill and ₦402.85billion for the 355-day bill. The stop rates for the 362-day and 355-day bills were 21.45% and 21.32%, respectively.

We expect cautious trading next week as investors turn their attention to the NTB auction, which will offer ₦700 billion across three tenors: 91-day, 182-day, and 364-day.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 2.78% and 2.00% to close at ₦67.42trillion from ₦65.59trillion and 108,053.95 from 105,933.03 the previous week.

A total turnover of 2.41 billion shares worth ₦55.51billion in 80,988 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 3.05 billion shares valued at ₦98.35billion that exchanged hands last week in 72,535 deals. On a sectoral basis, the Insurance and Industrial Goods indices closed positive this week, at 2.52% and 10.36%, while the Banking, Consumer Goods and Oil and Gas indices closed negative at -0.24%, -3.63% and -2.30%.

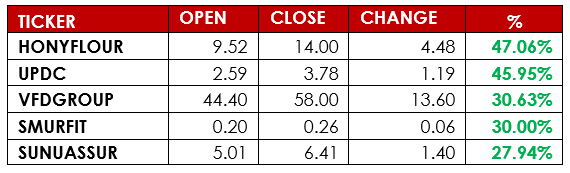

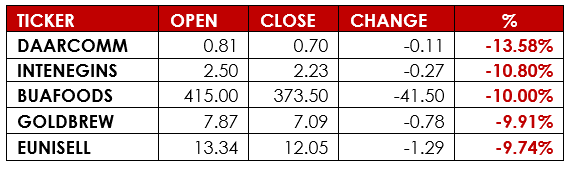

Notable gainers this week were Honeywell Flour Mill Plc and UPDC Plc, while notable losers were Daar Communications Plc and International Energy Insurance Plc.

We expect mixed sentiments next week, as Investors carry out sectoral rotations in light of released financial statements of listed companies.

CURRENCY

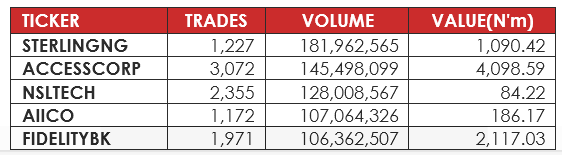

TOP TRADES BY VOLUME

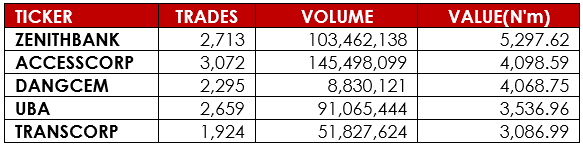

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, BusinessDay, Economic Confidential, Alpha10 Research