GLOBAL ECONOMY

The Dollar index rose this week, as escalating global trade tensions pressured the Euro and other major currencies. On Thursday, President Donald Trump threatened to impose 200% tariffs on all alcoholic products from the European Union, retaliating against the bloc’s 50% tariff on American whiskey and other US goods. He also reaffirmed his stance on implementing reciprocal tariffs on global trading partners, set to take effect on April 2, 2025. The annual inflation rate in the US fell to 2.80% in February 2025 from 3.00% in January, largely driven by a decline in Energy costs and slower price rises in Gasoline and fuel. On a monthly basis, the Consumer Price Index (CPI) rose by 0.20%, down from January’s 0.50% increase.

The British pound moved lower to £1/$1.29 after data showed that the UK economy unexpectedly contracted by 0.10% in January, contrary to market forecasts of a 0.10% expansion, following a 0.40% increase in December 2024. The decline was largely driven by weakness in the production sector. The largest downward contribution came from the production sector, which fell by -0.90%, after a 0.50% rise in the previous period. Manufacturing and Mining and Quarrying shrank by -1.10% and -3.30, with a corresponding -3.70% contraction in extraction of crude petroleum and natural gas and -0.20% decline in Construction.

In the Euro Area, trade tensions escalated after a 25% US tariff on steel and aluminum imports from Canada, Australia, the European Union (EU), and other countries took effect this week, triggering countermeasures from the European Union. The EU announced retaliatory tariffs on €26billion worth of US goods, set to begin in April, covering alcohol, steel, aluminum, textiles, leather goods, poultry, beef, eggs, and other products.

Foreign Direct Investment (FDI) into China sank by 20.40% from 2024 to approximately ¥98billion in the first two months of 2025. The decline from the first two months continued to reflect weaker foreign confidence in the Chinese economy, pressured by risks of a deflationary spiral and the view that the government delayed in its stimulus response. However, at a meeting on Thursday, the Pan Gongsheng, Governor of the People’s Bank of China (PBOC), reiterated pledges to cut interest rates and the Reserve Requirement Ratio (RRR) for commercial banks to boost economic growth.

Next week in the US, Investors will focus on the US Federal Reserve’s interest rate decision, alongside economic and interest-rate projections.

GLOBAL MARKETS

Tariffs imposed by the Trump administration have raised Investors’ fears that inflation could rise, making it harder for the Federal Reserve to cut interest rates, leading to increasing concerns about its potential to trigger a recession. US stocks continued to sell off, with a slight rebound at the end of the week. However, the Nasdaq, S&P 500 and Dow Jones indices decreased for the second consecutive week by -2.46%, -2.27% and -3.07% to 19,704.64, 5,638.94 and 41,488.19, respectively.

European shares traded lower this week as US tariffs on steel and aluminum imports took effect, triggering retaliatory measures from Canada and the EU, amid released data on the contraction of the UK economy. The London’s Financial Times Stock Exchange (FTSE) 100, Germany’s Deutscher Aktien (DAX) and France Cotation Assistée en Continu (CAC) 40 indices decreased by -0.55%, -0.10% and -1.14% to 8,632.33, 22,986.82 and 8,028.28, respectively.

Stock levels in China declined as investors grappled with a lack of market-moving catalysts in China. Analysts have raised concerns about China’s ability to meet its economic targets, as outlined in the recently concluded annual meeting. Additionally, escalating trade tensions weighed on Investors’ sentiment after US President Donald Trump’s steel and aluminum tariffs took effect this week. The Hang Seng index decreased by -1.12% to 23,959.98, while the Topix index increased by 0.27% to 2,715.85.

We expect cautious trading in the Global Equities market amidst ongoing trade tensions among major economies.

DOMESTIC ECONOMY

Nigeria’s total trade exports surged to $50.48billion in 2024, driven by exchange rate depreciation and the elimination of fuel subsidies, which boosted the country’s trade balance. Data from the National Bureau of Statistics (NBS) shows that Nigeria recorded a total trade volume of ₦138trillion, the highest in the country’s history, representing a 106% increase from ₦66.80trillion in 2023.

Nigeria’s petrol imports rose in 2024, despite increased domestic refining capacity, highlighting the country’s persistent reliance on imported fuel. The latest foreign trade statistics report from the National Bureau of Statistics (NBS) revealed that petrol import costs rose by 105.33% to ₦15.42trillion in 2024, up from ₦7.51trillion in 2023. Nigeria had anticipated a reduced reliance on imported fuel with the commencement of operations at the 650,000 barrels-per-day Dangote Refinery and the ongoing rehabilitation of state-owned refineries. However, domestic refining remains insufficient to meet national demand, due to delays in refinery ramp-up, supply chain inefficiencies, and persistent demand-supply imbalances, among other factors. The country’s vulnerability to foreign exchange fluctuations further complicates its ability to achieve self-sufficiency, as the rising cost of petrol imports continues to strain government finances and consumer purchasing power.

The Nigerian Insurance Industry Reform Act Bill, 2024, recently passed by the House of Representatives, entails a significant overhaul of the country’s insurance sector, aimed at establishing a comprehensive legal and regulatory framework to protect policyholders and foster a competitive and innovative insurance industry. It set the minimum capital requirements at ₦25billion, ₦15billion and ₦45billion for Non-life insurance, Life insurance and Reinsurance businesses, respectively.The bill also repealed several outdated laws, including the Insurance Act, Cap 117, Marine Insurance Act, Cap M3, Motor Vehicle (Third Party) Insurance Act, Cap M22 and the National Insurance Corporation of Nigeria Act. Individuals found operating unlicensed insurance businesses face penalties of up to ₦25million according to the new bill.

We await the release of inflation figures for February 2025.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity remained negative throughout the week, driven by Cash Reserve Ratio (CRR) debits, despite inflows for oil-producing states. The market saw further strain following the Treasury Bill auction settlement. Consequently, the Open Repo Rate (ORR) and the Overnight Rate (O/N) increased by 532bps and 513bps to 32.40% and 32.80%, respectively.

The Nigerian Treasury Bills (NTB) market average yield increased by 3bps to 18.88% against 18.85% last week. In the Bonds market, the average yield for the Short-tenor and Medium-tenor Bonds increased by 1bp and 11bps to 19.24% and 18.67%, while the average yield for the Long-tenor Bonds remained unchanged at 17.60%.

The Nigerian Treasury Bills Auction held this week, with an offer of ₦550billion across tenors. The total subscription was ₦1.27trillion and total allotment was ₦680.27billion, thus, the auction was oversold by ₦130.27billion. Stop rates increased by 4bps and 57bps to 17.79% and 18.39% for the 182-day and 364-day bills, while the stop rate for the 91-day bill remained unchanged at 17.00%.

We anticipate the Nigerian Treasury Bills auction scheduled to hold next week, as seen in the revised auction calendar, where ₦800billion will be offered across the 91-day, 182-day and 364-day tenors.

THE EQUITIES MARKET

Market Capitalization and All-Share Index decreased by -0.55% to close the week at ₦66.35trillion from ₦66.72trillion and 105,955.13 from 106,538.60 the previous week.

A total turnover of 3.28 billion shares worth ₦63.52billion in 60,782 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 1.82 billion shares valued at ₦47.23billion that exchanged hands last week in 64,222 deals. On a sectoral basis, the Banking, Oil and Gas and Industrial Goods indices closed negative for the second consecutive week, at -0.45%, -1.15% and -0.21%, while the Insurance and Consumer Goods Indices closed positive at 0.89% and 0.03%, respectively.

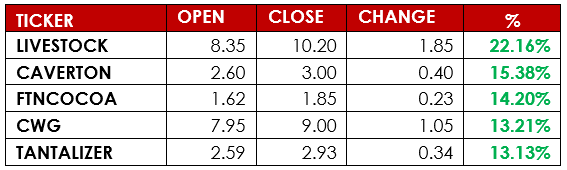

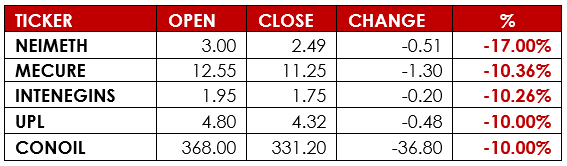

Notable gainers this week were Livestock Feeds Plc and Caverton Offshore Support Grp Plc, while notable losers were Neimeth International Pharmaceuticals Plc and Mecure Industries Plc.

We anticipate mixed sentiments in the equities market, amid recent selloffs and potential re-entry opportunities.

CURRENCY

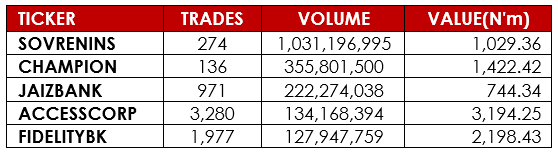

TOP TRADES BY VOLUME

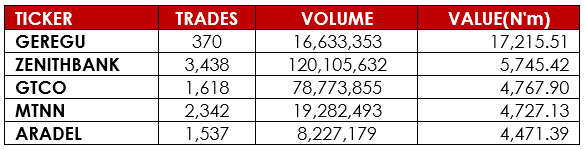

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research