GLOBAL ECONOMY

In US President Trump enacted sweeping tariffs and secured major trade deals with the EU, Japan, and Southeast Asia, while extending a tariff truce with China and pushing for increased agricultural exports. Treasury Secretary Scott Bessent is calling for interest rate cuts of up to 175 basis points from the current 4.33%, citing economic strain from tariffs and inflation. Inflation remains persistent in the US with headline CPI rising 0.20% monthly and 2.70% annually, while core CPI climbed to 3.10%. Producer prices surged 0.90% monthly, with core PPI hitting 3.70% annually; its highest in over a year, driven by spikes in services and food costs. Industrial production fell 0.10%, and capacity utilization dropped to 77.50%, below long-term averages.

The British Pound strengthened to £1/$1.36 after higher-than-expected Gross Domestic Product (GDP) figures signaling a stronger economy and thus reduced the likelihood of further Bank of England rate cuts. The UK GDP rose by 0.30% quarter-on-quarter and 1.20% year-on-year in Q2 2025, beating forecasts, while June GDP grew 0.40%, driven by services and construction. Unemployment held steady at 4.70% with manufacturing output rebounded 0.50% month-on-month, led by an 8.80% surge in electronics, though annual growth stalled. Construction rose 1.50% year-on-year, marking 11 consecutive monthly gains. The trade deficit widened to £5.01billion, as exports fell 2.60% and imports dropped 1.90%, with notable declines in shipments to the EU and US.

The Euro strengthened to €1/$1.17, supported by expectations of a US rate cut and steady Eurozone inflation at 2.00%. Eurozone GDP grew 0.10% quarter-on-quarter in Q2 2025, its weakest pace since late 2023, while annual growth eased to 1.40%, down from 1.50% in Q1 2025. Employment rose 0.10% quarterly to 171.70 million, marking the 17th straight period of growth, led by Spain (0.70%) and France (0.30%), while Germany and Italy saw -0.10% declines. Business confidence further dampened by the lingering US trade tensions and the EU’s exposure to new 15.00% tariffs.

The offshore Yuan weakened past ¥7.18/$1, reflecting Investors concerns over economic softness and geopolitical tensions. China’s Industrial production grew 5.70% year-on-year in July, down from 6.80%, with manufacturing up 6.20% and monthly output rising 0.38%. Retail sales increased 3.70%, the weakest since December 2024, while monthly activity fell 0.14%. Beijing eased suburban housing purchase limits and introduced interest subsidies for service sectors and consumer loans to boost spending. However, new Yuan loans fell by ¥50billion, and total social financing which refers to the broad measure of credit and liquidity in China’s economy dropped to ¥1.16trillion, far below expectations. Loan growth slowed to 6.90%, the weakest since 1998, while M2 money supply rose 8.80%, beating forecasts. In trade, China extended its tariff truce with the US and also demanded easing of High-Bandwidth Memory (HBM) chip export controls which are critical for artificial intelligence (AI) development, and imposed steep antidumping duties on Canadian goods.

Next week, Investors will focus on the FOMC minutes, inflation reports from UK and other Economic data to guide sentiments and provide insights into Global Economic performance.

GLOBAL MARKETS

This week, US stocks closed high with some major stocks losing some initial gains as Investors digested economic data, corporate news, and geopolitical developments. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices closed higher, increasing by 0.81%, 0.94% and 1.74% to close the week at 21,622.98, 6,449.80 and 44,946.12 respectively.

In the UK and across Europe, major stocks closed positive, however losing some initial gains towards the close of the week. London’s Financial Times Stock Exchange (FTSE) 100, Germany’s Deutscher Aktien (DAX) and France Cotation Assistéeen Continu (CAC) 40 indices increased by 0.47%, 0.18% and 2.33% to 9,138.90, 24,359.30 and 7,923.45 respectively.

The Asian stock market closed higher this week with major stocks closing positive as market rallied with hopes of a fresh Beijing stimulus to support economic growth and counter US tariff pressure. The Hang Seng and Topix indices increased by 1.65% and 2.76% to 25,270.07 and 3,107.68 respectively.

Next week, Investors will monitor key Interest rate decisions and the minutes of the FOMC meeting to shape investment decisions.

DOMESTIC ECONOMY

Nigeria’s Inflation Eases to 21.88% in July 2025 Amid Improved Food Supply and Stable Exchange Rates

Nigeria’s headline inflation slowed to 21.88% in July 2025, down from 22.22% in June, and significantly lower than 33.40% in July 2024, reflecting improved domestic food supply and relative exchange rate stability. Urban inflation dropped to 22.01%, while rural inflation stood at 21.08% year-on-year. Food inflation eased to 22.74%, with monthly declines in staple prices like rice, maize, and vegetable oil. Core inflation also fell to 21.33%, down from 27.47% a year earlier, as analysts cite ongoing harvests and moderating energy costs as key drivers of the downward trend.

FG Settles ₦2trillion Capital Budget Arrears, Targets 7% GDP Growth with Stronger State Surpluses

The Federal Government has cleared over ₦2trillion in outstanding capital budget obligations from 2024, with no pending commitments left unprocessed, according to Finance Minister Wale Edun, who also revealed that states’ combined fiscal surplus rose from ₦2.80trillion to ₦7.10trillion since H1 2023. The administration’s medium-term goal remains 7% annual GDP growth, driven by private investment, Public-Private Partnerships’ (PPPs), and strategic spending in agriculture, education, health, and infrastructure. Nigeria’s Q1 2025 GDP grew 3.13% year-on-year, reaching ₦94.05trillion nominally, with key growth sectors including trade, communications, rail transport, and crop production.

Nigeria’s Crude Oil Output Hits 1.51 Million barrels per day in July, Retains Top Spot in Africa

Nigeria’s average daily crude oil production rose to 1.51 million barrels per day (bpd) in July 2025, slightly up from 1.50 million bpd in June, surpassing OPEC’s quota for the second consecutive month and maintaining its lead as Africa’s top oil producer ahead of Algeria’s 937,000 bpd. According to OPEC’s Monthly Oil Market Report, global OPEC+ output increased by 335,000 bpd, with Saudi Arabia contributing nearly half. Meanwhile, Nigeria’s Upstream Petroleum Regulatory Commission reported a peak output of 1.78 million bpd, driven by enhanced security operations, while gas production rose to 7.58 billion standard cubic feet/day in June. However, crude oil and condensate sales fell to 21.68 million barrels, down from 24.77 million barrels in May.

Nigeria’s Non-Oil Exports Surge to $3.23billion in H1 2025, Driven by AfCFTA and Value-Added Products

Nigeria’s non-oil exports rose by 19.59% to $3.23billion in H1 2025, with volumes reaching 4.04 million metric tonnes, up from 3.83 million tonnes in H1 2024, according to the Nigerian Export Promotion Council (NEPC). Exports to 11 ECOWAS countries totaled 663 million metric tonnes, while 21 non-ECOWAS African nations received 488 million tonnes worth $83.54million, reflecting Nigeria’s expanding regional trade under African Continental Free Trade Area (AfCFTA). Top products included cocoa beans (34.88%) and urea/fertiliser (17.65%), with Indorama and Starlink Global leading exporters. Seaports handled 94.15% of traffic, and 29 banks processed 10,214 Nigerian Export Proceeds Forms (NXPs), led by Zenith Bank (31.98%). NEPC conducted 252 training programmes for 27,352 participants, boosting export readiness and compliance.

Next week Investors will watch out for Q2 GDP growth figures and PMI data to influence economic sentiment.

EUROBOND MARKET

The SSA Eurobonds posted a mixed performance during the week as Investors responded to multiple global developments—initial optimism driven by the Bank of England’s 25bps rate cut and hopes for a Fed rate cut in September gave way mid-week to weaker sentiments after US July CPI held steady at 2.70% and higher-than-expected PPI data pressured US Treasuries, triggering broad government bond sell-offs. Despite this, major SSA Eurobonds ended the week higher, with Nigerian Eurobonds seeing a 20bps drop in average mid-yield, closing at 7.84%.

Nigeria’s Eurobond market is expected to trade cautiously next week with mixed sentiment, as Investors weigh the geopolitical implications of the Trump-Putin meeting alongside ongoing global uncertainties that could influence risk appetite and capital flows.

DOMESTIC MARKETS

SEC DG Projects $10trillion Digital Asset Boom in Africa-Middle East by 2030, Elected IOSCO Vice Chair.

Dr. Emomotimi Agama, Director-General of Nigeria’s SEC, has projected that digital asset opportunities in Africa and the Middle East could reach $10trillion by 2030, driven by the region’s youthful, tech-savvy population. Speaking after his election as Vice Chairman of the International Organization of Securities Commissions (IOSCO) Africa/Middle East Regional Committee (AMERC) and board member of IOSCO, Agama outlined plans to expand listings, harmonize standards, and boost SME access through fintech innovation and regional market integration. He emphasized leveraging AfCFTA, pension reforms, and infrastructure de-risking to deepen capital markets and democratize wealth creation across the continent.

MONEY MARKET AND FIXED INCOME

System liquidity opened the week at a credit of ₦750.33billion but slipped to a deficit of ₦94.57billion due to persistent liquidity tightness and increased reliance on CBN’s Standing Lending Facility (SLF). Consequently, the Short-term rates closed high, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) increased by 560bps and 540bps to 32.10% and 32.40% respectively.

The Nigerian Treasury Bills (NTB) market average yield increased week-on-week by 159bps to 18.01%. The bonds market traded mixed throughout the week, with buying interest concentrated in short and mid-tenor instruments, while longer-dated bonds particularly the FGN 2037 and FGN 2038 faced notable selling pressure. The average yield for the short-tenor, mid-tenor and long tenor bonds increased by 9bps, 27bps and 11bps to 16.65%, 16.72%, and 15.70%.

We expect cautious trading as Investors turn their attention to the Nigeria Treasury Bills auction next week, where the DMO is offering ₦230billion across tenors against ₦303.79billion

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization depreciated by 0.77% to close the week at 144,628.20 and ₦91.50trillion compared to 145,754.91 and ₦92.22trillion last week.

A total turnover of 8.56 billion shares worth ₦99.94billion in 177,870 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 8.74 billion shares valued at ₦134.58billion that exchanged hands last week in 180,290 deals.

On a sectoral basis, Consumer Goods, Industrial Goods, Banking and Oil and Gas indices closed negative at -0.94%, -0.83%, -0.23% and -1.42%, while the Insurance index was the sole gainer, closing positive at 8.21% respectively.

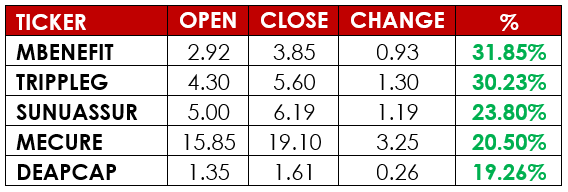

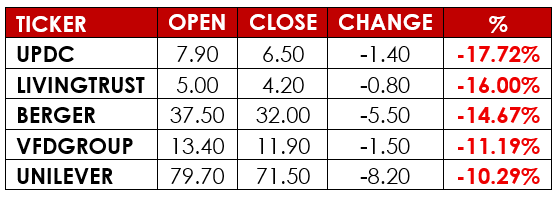

Notable gainers this week were Mutual Benefits Assurance PLC and Tripple Gee and Company PLC, while Notable losers were Livingtrust Mortgage Bank PLC and UPDC PLC.

We anticipate profit-taking to continue but we also expect portfolio rebalancing as Investors seek to take positions on viable stocks.

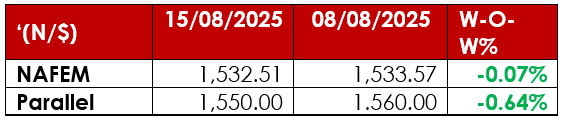

CURRENCY

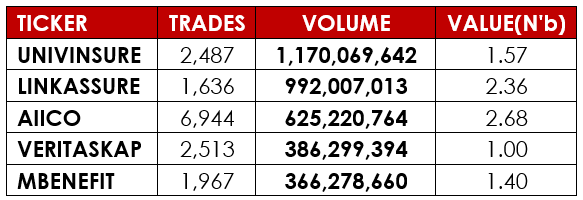

TOP TRADES BY VOLUME

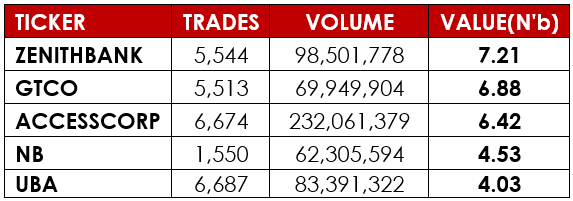

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst utmost care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication.

Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.