GLOBAL ECONOMY

US inflation data for late 2025 indicate easing underlying pressures, with core Consumer Price Index (CPI) rising a softer‑than‑expected 0.20% in December as declines in used car prices offset modest increases in apparel and medical goods. Annual core inflation held at 2.60 unchanged from the previous month, its lowest since 2021, supported by slower increases in used vehicles and household furnishings despite a pickup in shelter and medical care. Headline CPI rose 0.30% month‑on‑month and 2.70% year‑on‑year, driven mainly by food and shelter, while energy inflation moderated sharply due to falling gasoline prices. Producer inflation was firmer, with headline PPI up 0.20% in November from 0.10% the previous month, and annual producer inflation rising to 3% from 2.80% on higher energy costs, although core PPI was unchanged, signaling subdued pipeline pressures.

The UK economy grew by 0.30% in November 2025, rebounding from October’s contraction and outperforming expectations, driven mainly by a 0.30% rise in services, especially strong gains in professional, scientific and technical activities, information and communication, and retail trade. Industrial output also strengthened, rising 1.10% as manufacturing expanded by 2.10%, boosted by a sharp rebound in transport equipment production following earlier cyber‑related disruptions. However, construction activity continued to weaken, falling 1.30% in the month. On an annual basis, GDP grew 1.40%, while industrial and manufacturing production both rose 2.30% and 2.10% respectively, marking their strongest performances since 2021.

The Eurozone’s trade surplus narrowed to €9.90billion from €17.91billion in November 2025 as exports declined more sharply than imports, driven by weaker sales of machinery, chemicals and food, alongside reduced shipments to major partners. Imports fell mainly on lower energy purchases. Meanwhile, industrial production rose 0.70% month‑on‑month and 2.50% year‑on‑year, supported by strong capital goods output despite declines in energy and consumer goods.

China recorded a record $1.19trillion trade surplus in 2025 as exports rose 5.50% while imports were broadly flat, reflecting a strong shift toward non‑US markets amid higher US tariffs. In December, the surplus reached $114.10billion, with exports up 6.60% year‑on‑year – driven by strong growth to ASEAN, the EU, and emerging markets while shipments to the US plunged 30%. Imports rose 5.70% in December, supported by resilient domestic demand and pre‑holiday restocking, although full‑year growth was flat. By product, China increased purchases of high‑tech and data‑processing equipment but cut imports of energy and industrial commodities. Meanwhile, money supply (M2) grew 8.50% year‑on‑year in December, reaching a record level and reflecting continued policy support.

Next week, we await several economic data releases – PCE price indices, and another estimate of the third quarter GDP from the US, PMIs for the Eurozone, UK, Japan, Australia, and India. Others are the UK inflation rate and unemployment, and in Asia, China’s final GDP print for the year and the Bank of Japan monetary policy decision.

GLOBAL MARKETS

Stocks in the US closed lower on Friday as Investors digested a mix of geopolitical developments, Federal Reserve uncertainty, and the start of the fourth-quarter earnings season. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices decreased by -0.91%, -0.38% and -0.29% to 25,529.26, 6,940.01 and 49,359.33, respectively.

Major stocks in the UK closed higher, driven by renewed risk appetite and strong gains in financial stocks, as Banks led the advance after better-than-expected UK economic data boosted confidence in growth and credit conditions. European stocks closed mixed as markets continued to assess earnings profits and monitor geopolitical risks. Compared to last week, the FTSE 100 and German DAX increased by 1.09% and 0.14% to 10,235.29 and 25,297.13, while the CAC 40 index decreased by -1.23% to close at 8,258.94.

Asian markets closed higher as China’s Central Bank announced on Thursday cuts to sector-specific interest rates to provide an early boost to the economy. Compared to last week, the Hang Seng and the Topix indices increased by 2.34% and 4.11% to close at 26,844.96 and 3,658.68, respectively.

Next week, we expect current sentiments to persist as more economic data is released.

DOMESTIC ECONOMY

Nigeria’s Inflation Falls to 15.15% After CPI Rebasing, Showing Sharp Slowdown but From a Higher Revised Base

Nigeria’s headline inflation eased to 15.15% in December 2025 from 17.33% in November, reflecting a major deceleration in price pressures following the National Bureau of Statistics’ CPI rebasing, which shifted the base year to a 12‑month 2024 average. The CPI rose slightly to 131.20 from 130.50, while month‑on‑month inflation slowed to 0.54% from 1.22%, showing cooling short‑term pressures. Despite the moderation, inflation across January–November 2025 was revised upward by 3.00–2.88 percentage points, confirming prices were higher for longer than earlier reported. Food inflation plunged to 10.84% from 39.84% a year earlier, aided by lower prices of tomatoes, garri, grains and vegetables; core inflation dropped to 18.63% from 29.28%; urban and rural inflation fell to 14.85% and 14.56%, respectively, while Abia recorded the highest state rate at 19.03%. The IMF endorsed the new methodology, noting it aligns with global CPI standards.

EU Delists Nigeria from High‑Risk Finance List, Boosting Trade, Investment Confidence

The EU has officially removed Nigeria from its high‑risk money‑laundering list effective 29 January 2026 following Nigeria’s exit from the FATF grey list in 2025, a move expected to cut compliance costs, ease cross‑border transactions, improve bank relationships, and strengthen Investor confidence. The EU delisted Nigeria, South Africa, Burkina Faso, Mali, Mozambique and Tanzania, lifting enhanced due‑diligence rules once applied to Nigerian-linked transactions, while adding Bolivia and the British Virgin Islands to the list. Nigeria’s Minister of State for Finance hailed the decision as a “big win,” noting benefits for Exporters, Fintech’s, Banks and Investors. With reduced scrutiny, Nigeria is set for smoother trade flows, faster remittances and stronger capital inflows supporting broader reforms in its AML/CFT regime and enhancing the country’s global financial credibility.

NRS Debunks Claims of New VAT on Bank Transfers, Says No Fresh Tax Burden Introduced

The Nigeria Revenue Service (NRS) has dismissed media reports suggesting that the Nigeria Tax Act introduced new VAT charges on banking services, clarifying that VAT has always applied to fees and commissions such as transfer charges, USSD fees, cards, and account maintenance not on the money transferred. In a statement issued on 14 January 2026, the NRS stressed that no new tax obligation was created and urged the public to ignore misinformation. The agency also released VAT FAQs confirming that savings interest, basic food items, medical products, and educational services remain VAT‑exempt, noting that recent changes relate only to improved compliance and enforcement. The clarification follows the rollout of tax reforms signed in June 2025, aimed at strengthening Nigeria’s fiscal framework without adding extra VAT burdens on ordinary Nigerians.

FG Clarifies That Nigeria’s ₦152.40trillion Debt Surge Stems From Transparency and FX Revaluation, Not Fresh Borrowing

Nigeria’s ₦152.40trillion public debt is largely the outcome of improved fiscal transparency and foreign‑exchange revaluation – not new borrowing – according to Finance Minister Wale Edun at the Nigerian Economic Summit Group (NESG) 2026 Outlook launch. The ministry explained that roughly ₦30trillon came from formally recognizing previously unrecorded Ways and Means obligations, while about ₦49trillion resulted from FX reforms that revalued foreign‑denominated debt. Edun emphasized that the updated figure reflects corrected reporting gaps rather than fiscal irresponsibility and noted an 84% execution rate for the 2024 capital budget, with implementation extended to March 2026 to complete priority infrastructure projects. The government reaffirmed its commitment to responsible debt management, stronger public‑finance governance, and reforms aimed at restoring investor confidence and ensuring long‑term economic stability.

Nigeria Misses OPEC Quota Again as Crude Output Slips to 1.42mbpd, Despite Stronger Condensate Boost

Nigeria’s crude oil output dipped to 1.42mbpd (million barrels per day) in December 2025 from 1.44mbpd in November, marking the fifth consecutive miss of its OPEC quota, according to OPEC’s latest Monthly Oil Market Report (MOMR) data. Quarterly averages show a steady decline from 1.47mbpd (Q1) to 1.42mbpd (Q4), underscoring structural constraints in the upstream sector. However, secondary sources were more upbeat, estimating 1.50mbpd, up 1.35% month‑on‑month. Despite the slump, Nigeria remained Africa’s top producer, ahead of Libya’s 1.37mbpd. Broader OPEC+’s output fell to 42.83mbpd, down 238,000bpd. Domestic Nigerian Upstream Petroleum Regulatory Commission (NUPRC) figures paint a stronger picture when condensates are included, with combined crude‑and‑condensate production averaging 1.64mbpd over Jan–Nov 2025, fluctuating between 1.58mbpd and 1.73mbpd. The persistent gap between OPEC quotas and actual crude output continues to limit Nigeria’s FX inflows and fiscal buffers, even as reforms aim to stabilise production amid security, infrastructure and operational bottlenecks.

Edun Hints Interest Rate Cuts Could Be Near as Inflation Eases, Offering Fiscal Relief for Nigeria

Finance Minister Wale Edun signaled that interest rate cuts may come soon if Nigeria’s inflation continues to ease, a shift that would lower borrowing costs and ease pressure on public finances heavily strained by debt servicing. Speaking to Bloomberg at Abu Dhabi Sustainability Week, Edun praised the CBN’s aggressive tightening which more than doubled rates since 2022 before a cut to 27.00% in September for driving down inflation from its late‑2024 peak. With the proposed ₦58trillion 2026 budget allocating over a quarter to interest payments and projected revenues at ₦34trillion, easing rates could reduce the ₦24trillion (4.30% of GDP) deficit and free up fiscal space.

Next week, we anticipate cautious sentiments as Investors await Q4 GDP release.

EUROBOND MARKET

African Eurobonds traded mildly bullish this week, supported by steady demand from oil-producing credits amid stable commodity prices. Nigerian sovereign yields compressed across key maturities, driving an 8bps w/w decline in the average benchmark yield to 7.00%, with notable interest in mid-curve bonds. Market sentiment was underpinned by resilient global risk appetite and positioning ahead of the new year, while liquidity remained balanced across major African credits.

We expect sustained buying interest in high-yield African Eurobonds next week, aided by firm oil prices and supportive technicals, though activity may remain moderate as Investors await fresh macro signals.

ALTERNATIVE ASSETS

GOLD

Gold prices were slightly softer over the week, with spot gold closing at approximately $4,596/oz on 16 January 2026, slipping 0.42% from the previous day but still near record highs. Price action was largely range‑bound as a firmer dollar and subdued safe‑haven demand kept upside limited.

OIL

Oil ended the week modestly higher. Brent crude settled at $64.13/bbl (+0.63%) and WTI at $59.44/bbl (+0.40%) on 16 January 2026, supported by lingering geopolitical tensions involving Iran. Despite this, prices remained volatile, reversing mid‑week gains as the US signaled a softer stance toward Ira.

ETFs

US‑listed ETFs continued to attract inflows in early January. For the week of January 12–16, flows were led by equity ETFs, with strong demand for large‑cap index products, while commodity ETFs – particularly gold‑backed funds – also saw notable Investor interest. Fixed‑income ETFs sustained healthy inflows as markets-maintained expectations of Fed easing later in the year.

Gold is expected to remain well‑supported by medium‑term Fed rate‑cut expectations and ongoing geopolitical uncertainty, while Oil is likely to trade within a tight range, with geopolitical risks providing intermittent support and ETF flows are expected to stay positive, driven mainly by fixed‑income demand and continued allocations to commodity funds, especially gold ETFs.

DOMESTIC MARKETS

SEC’s higher capital rules win broad operator support, set to reshape Nigeria’s capital market

SEC has introduced sharply increased capital requirements, a move widely welcomed by Capital Market Operators (CMOs), as long‑anticipated and essential for deepening market stability. Operators praised the regulator for sticking to its timeline and extensive consultations, though some flagged inconsistencies in broker‑dealer classifications. With an 18‑month window ending June 30, 2027, analysts expect orderly restructuring through mergers, license downgrades, and capital injections rather than mass exits, especially as demutualization proceeds have strengthened many firms. Digital asset operators were also fully integrated into the framework, with new categories such as Digital Assets Offering Platform (DAOP) (₦1billion), Ancillary Virtual Assets Service Providers (AVASPs) (₦300million), Digital Assets Intermediary (DAI) (₦500million), and Real‑World Assets Tokenization and Offering Platform (RATOP) (₦1billion) formalized. While fees are not expected to rise immediately, the recapitalization push is anticipated to boost liquidity, enhance governance, and align Nigeria with global standards – ultimately leaving fewer but stronger players and a more resilient market.

MONEY MARKET AND FIXED INCOME

System liquidity opened the week at a credit of ₦1.47trillion, an increase of ₦48.77billion from the previous week’s close, declining further on Tuesday to ₦1.40trillion and later improving mid-week on Wednesday by ₦670.28billion to ₦2.07trillion, with a further increase on Friday to close the week at a credit of ₦2.13trillion. Consequently, the Open Repo Rate (OPR) remained unchanged at 22.50% while the Overnight Rate (O/N) increased this week by 7bps to 22.78%.

EQUITIES MARKET

The Nigerian equities market remained bullish as the NGX All-Share Index and Market Capitalization appreciated by 2.36% and 2.48% to close the week at 166,129.50 and ₦106.35 compared to 162,298.08 and ₦103.78trillion last week.

A total turnover of 4.61 billion shares worth ₦130.64billion in 263,439 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 4.16 billion shares valued at ₦94.03billion that exchanged hands last week in 248,254 deals.

On a sectoral basis, all sectors closed positive, with the Banking, Consumer Goods, Industrial Goods, Insurance and Oil and Gas indices increasing by 3.45%, 1.59%, 0.67%, 1.78% and 5.71% compared to previous week.

Notable gainers this week were NCR (Nigeria) PLC and SCOA Nigeria PLC while Austin Laz & Company PLC and Ikeja Hotel PLC topped the losers list.

We anticipate the Equities market to remain bullish this week driven by strengthened Investor sentiments and growing public interest in the Market.

CURRENCY

| (₦/$) | 16/01/2026 | 09/01/2026 | W-O-W% |

| NAFEM | 1,417.95 | 1,423.17 | -0.37% |

| Parallel | 1,485.00 | 1,485.00 | 0.00% |

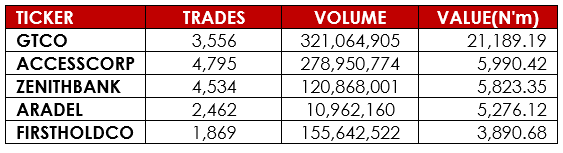

TOP TRADES BY VOLUME

| TICKER | TOP TRADES BY VOLUME TRADES | VOLUME | VALUE (₦’b) |

| SOVRENINS | 846 | 905,919,498 | 2.95 |

| ACCESSCORP | 10,032 | 277,440,534 | 6.38 |

| LINKASSURE | 854 | 222,704,976 | 0.40 |

| ZENITHBANK | 9,972 | 185,819,101 | 12.82 |

| FIDELITYBK | 3,535 | 182,338,822 | 3.61 |

TOP TRADES BY VALUE

| TICKER | TOP TRADES BY VALUE TRADES | VOLUME | VALUE(₦’b) |

| MTNN | 20,461 | 25,771,749 | 15.47 |

| ARADEL | 4,869 | 18,787,604 | 14.67 |

| ZENITHBANK | 9,972 | 185,819,101 | 12.82 |

| SEPLAT | 2,362 | 1,057,537 | 6.92 |

| GTCO | 10,354 | 68,970,021 | 6.84 |

TOP GAINERS

| TOP GAINERS TICKER | OPEN | CLOSE | CHANGE | % |

| NCR | 79.95 | 128.55 | 48.60 | 60.79% |

| SCOA | 9.35 | 14.90 | 5.55 | 59.36% |

| DEAPCAP | 3.00 | 4.46 | 1.46 | 48.67% |

| JAIZBANK | 5.62 | 8.19 | 2.57 | 45.73% |

| OMATEK | 1.28 | 1.77 | 0.49 | 38.28% |

TOP LOSERS

| TICKER | OPEN | CLOSE | CHANGE | % |

| IKEJAHOTEL | 40.00 | 35.05 | -4.95 | -12.38% |

| AUSTINLAZ | 4.13 | 3.75 | -0.38 | -9.20% |

| ETERNA | 35.00 | 32.30 | -2.70 | -7.71% |

| UNIVINSURE | 1.30 | 1.20 | -0.10 | -7.69% |

| EUNISELL | 169.80 | 156.95 | -12.85 | -7.57% |

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst utmost care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication.

Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.