GLOBAL ECONOMY

The US Dollar faced pressure amid concerns about the economic fallout from tariffs and increasing policy uncertainty under Trump. President Trump also indicated a possible de-escalation of trade tensions with China, stating he does not want tariffs to rise further and may even consider reducing them. Meanwhile, Trump criticized Fed Chair Powell of being too slow to cut rates, as Powell said the Fed is cautiously monitoring the impact of tariffs before taking decisions. Initial jobless claims in the United States fell by 9,000 from the previous week to 215,000 on the second week of April, contrasting with market expectations of a 1,000 increase.

The annual inflation rate in the UK slowed to 2.60% in March 2025 from 2.80% in February and below the market and the BoE’s forecasts of 2.70%. The largest downward contributions came from recreation and culture. Transport also contributed to the slowdown, largely due to a 5.30% fall in motor fuel prices. Month-on-month, the Consumer Price Index edged up 0.30%, slightly below both the previous month’s increase and expectations of 0.40%. Annual core inflation slowed to 3.40% from 3.50%. The UK trade balance posted a £1.96billion deficit in February 2025, shifting from a revised £0.30billion surplus in the previous month. Exports grew 0.20% month-on-month to £76.24billion, while imports grew by 3.20% to £78.19billion.

The European Central Bank (ECB) cut all three of its key interest rates by 25bps, lowering the main refinancing rate to 2.40%, the deposit rate to 2.25% and the marginal lending facility to 2.65%, as expected. The decision reflects growing confidence that inflation is on track to return sustainably to the 2.00% target. The Euro weakened to approach €1/$1.13, after the ECB lowered borrowing costs. The annual inflation rate in the Eurozone slowed to 2.20% in March 2025 from 2.30% in February. Among the bloc’s largest economies, inflation eased in Germany (2.30% vs 2.60%), Spain (2.20% vs 2.90%), the Netherlands (3.40% vs 3.50%), and Belgium (3.60% vs 4.40%), but steadied in France (at 0.90%) and accelerated in Italy (2.10% vs 1.70%).

Foreign Direct Investment (FDI) into China sank by 10.80% from the previous year to about $36.90billion in Q1, 2025, following the 27.10% slump in 2024. The decline continued to reflect weaker foreign confidence into largest projects in the Chinese economy, pressured by risks of a deflationary spiral and the view that the government delayed in its stimulus response, recently magnified by the threat of tariffs from the United States government. The offshore yuan fell to around ¥7.30/$1 on Thursday, reversing gains from the previous session as investor caution resurfaced amid renewed concerns over US-China trade relations.

Next week, we expect uncertainty in the global economy as Investors watch out for reactions to China’s potential monetary easing and outcomes from the IMF and World Bank meetings.

GLOBAL MARKETS

US stocks closed negative ahead of the Good Friday holiday, as Investors weighed trade talks and interest rate uncertainty. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices decreased by -2.62%, -1.50% and -2.66% to 16,286.45, 5,282.7 and 39,142.23, respectively.

In the UK and across Europe, sentiment improved slightly as the US negotiated trade deals was made in talks with Japan, raising hopes for broader deals. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices decreased by 3.91%, 2.55% and 4.08% to 8,275.66, 7,285.86 and 21,205.86 respectively.

Chinese stocks closed high as Beijing set conditions for entering new talks with the US, calling for policy consistency following Trump’s indication of a possible de-escalation of trade tensions with China. The Hang Seng and Topix indices increased by 2.30% and 3.74% to 21,395.14 and 2,559.15 respectively.

Global markets may see cautious trading, Investors will also closely watch global earnings reports amidst uncertainty on the path of tariffs by the US.

DOMESTIC ECONOMY

Nigeria’s Inflation rises to 24.23% in March 2025

Nigeria’s annual inflation rate rose slightly to 24.23% in March 2025, from 23.18% in the prior month. Food inflation, the largest component of the inflation basket, remained elevated but eased to 21.79% from 23.51% in the prior month. The core inflation, which excludes the prices of volatile agricultural products and energy, quickened to 24.43%, from 23.01% in the previous month. On a monthly basis, consumer prices rose by 3.90% in March, accelerating from 2.04% in February.

Nigeria’s PMI Expands for Third Month Amid Naira Stability and Lower Energy Costs

Nigeria’s Purchasing Managers Index (PMI) increased to 52.30 points in March 2025, up from 51.40 points in February, marking the third consecutive month of expansion. This growth is attributed to the relative stability of the Naira and reductions in energy prices. The Industry and Services sectors both recorded expansions to 51.50 points, while the Agriculture sector continued its strong growth at 54.70 points, achieving its eighth straight month of expansion. Among 36 subsectors analyzed, 24 subsectors reported growth, with Forestry showing the highest gains, while 12 subsectors faced declines, led by Non-metallic Mineral products.

FAAC Distributes ₦1.58trillion in March 2025 Amid Declining Monthly Allocations

The Federation Account Allocation Committee (FAAC) has distributed a total of ₦1.58trillion among Nigeria’s three tiers of government for revenue generated in March 2025. This marks the third consecutive decline in monthly allocations, following ₦1.68trillion in February and ₦1.70trillion in January, according to Bawa Mokwa, Director of Press and Public Relations at the Office of the Accountant General of the Federation, after the April 2025 FAAC meeting in Abuja. The distributable revenue, derived from Statutory Revenue, Value Added Tax (VAT), Electronic Money Transfer Levy (EMTL), and Exchange Difference Earnings, faced downward pressure despite a rise in gross statutory inflows for the month. FAAC attributed the decline to reduced Oil and Gas Royalties, VAT, EMTL, excise duties, import duties, and Common External Tariff (CET) levies, although Petroleum Profit Tax (PPT) and Companies Income Tax (CIT) saw significant growth during the month.

We expect CBN to sustain its market stabilization interventions to prevent further depreciation of the Naira in the coming weeks.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity opened the week positive with a surplus of ₦262.61billion. However, it declined mid-week due to CBN FX settlements. Although inflows from Remita, and ₦73.75billion in FGN Bond coupons provided relief, it closed at a debit of ₦365.62billion. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) increased by 502bps and 509bps to 31.60% and 32.05%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 133bps to 19.71% against 21.04% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor and Long-tenor Bonds increased by 6bps, 2bps, and 16bps to 19.05%, 19.24% and 17.81%, respectively.

We anticipate cautious trading as Investors await next week’s NTB primary market auction and the Bonds Auction Calendar for Q2, 2025.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization depreciated by 0.32%to close the week at 104,233.81and ₦65.50trillion, from the previous week figure of 104,563.34 points and ₦65.71trillion, respectively.

A total turnover of 1.53 billion shares worth ₦43.01billion in 51,156 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 2.09 billion shares valued at ₦52.97billion that exchanged hands last week in 64,612 deals. On a sectoral basis, the Banking and Insurance Indices closed negative, at -5.43% and -2.34%. The Consumer Goods and Oil and Gas indices both closed positive at 2.23% and 0.20%, while the Industrial Goods index remained unchanged.

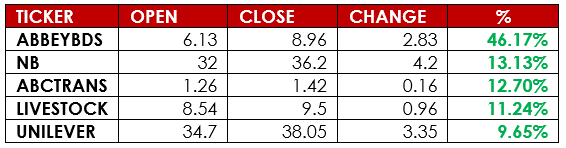

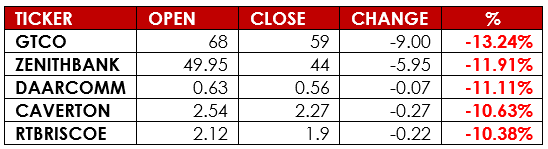

Notable gainers this week were Abbey Mortgage Bank Plc and Nigerian Brew. Plc., while notable losers were Guaranty Trust Holding Company and Zenith Bank Plc.

We expect cautious trading in the equities market as Investors await Q1 2025 earnings report of companies.

CURRENCY

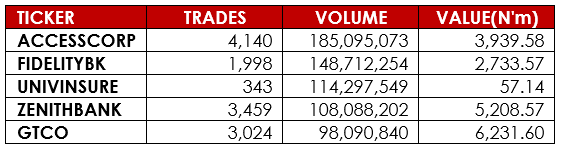

TOP TRADES BY VOLUME

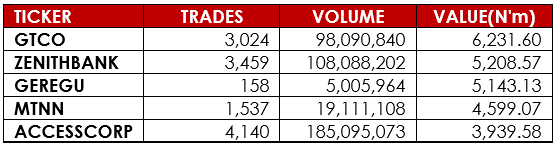

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, BusinessDay, Alpha10 Research