GLOBAL ECONOMY

The annual inflation rate in the US accelerated for a third consecutive month, reaching 2.90% in December 2024, compared to 2.70% in November. On a month-on-month basis, in December 2024, the inflation rate increased by 0.40% compared to 0.30% in November and forecasts of 0.30%. Meanwhile, annual core inflation, which excludes volatile components such as food and energy fell by 0.10% to 3.20%, from 3.30% in November.

In the UK, the annual inflation rate fell to 2.50% in December, in line with the Bank of England’s forecast but below market expectations of 2.60%. The annual core inflation decreased to 3.20% in December 2024 from 3.50% in the previous month, marking the lowest reading since September 2024 and increased by 0.30% on a month-on-month basis, from a flat reading in November.

The Euro rebounded slightly to €1/$1.03, following reports that President-elect Donald Trump’s economic team is considering a phased approach to trade tariffs that could avoid inflation spikes. The proposed strategy includes gradual monthly tariff hikes of 2.00% to 5.00% instead of a one-time increase. Attention now shifts to the European Central Bank’s (ECB) December meeting minutes and upcoming Eurozone inflation data for clues on future monetary policy.

The Chinese economy grew by 5.00% in 2024, aligning with the government’s target, but slightly down from the 5.20% growth recorded in 2023. This performance was driven by a series of stimulus measures introduced in September to support recovery and restore confidence. Additionally, companies accelerated exports in anticipation of higher US tariffs.

All eyes will be on Inauguration Day on Monday as Donald Trump is sworn in as President.

GLOBAL MARKETS

US stocks surged last week, driven by a tech revival and strong gains across major indices. The Nasdaq index, S&P 500 and Dow Jones indices increased by 2.85%, 2.91% and 2.69% to 21,441.16, 5,996.66 and 43,487.83, respectively.

European stocks closed higher this week, fueled by optimism over potential interest-rate cuts from the BoE, as recent data from the UK strengthened the case for monetary easing to support the UK economy. London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices closed positive this week, increasing by 3.11%, 3.41% and 3.75% to 8,505.22, 7,709.75 and 20,903.39, respectively.

Chinese stocks finished the week higher in response to positive economic data. In Japan, investors remained cautious about Japanese equities after Bank of Japan Governor Kazuo Ueda indicated on Wednesday that the Central Bank would discuss the possibility of raising interest rates at its upcoming policy meeting next week. The Hang Seng index increased by 2.73% to 19,584.06 while the Topix index decreased by -1.32% to close at 2,678.42.

We anticipate cautious trading as traders monitor President-Elect Donald Trump speech for hints about policy changes and potential executive orders.

DOMESTIC ECONOMY

In December 2024, Nigeria’s inflation rate surged to 34.80%, marking a slight increase from the 34.60% recorded in November 2024. This rise was primarily driven by heightened demand for goods and services during the festive season. On a year-on-year basis, the inflation rate increased by 5.87% points compared to December 2023 at 28.92%. The National Bureau of Statistics (NBS) attributed this persistent inflationary pressure to factors such as currency depreciation, high energy costs, and ongoing supply chain disruption.

The Federal Government, States, and Local Government Councils shared a total sum of ₦1.42trillion as revenue for December 2024, a decline of 17.54% compared to ₦1.73trillion shared in November 2024. This allocation was done during the Federation Account Allocation Committee (FAAC) meeting held in Abuja on Friday. The total distributable revenue comprised ₦386.12billion from statutory revenue, ₦604.87billion from Value Added Tax (VAT), ₦31.21billion from the Electronic Money Transfer Levy (EMTL), and ₦402.71billion from Exchange Difference revenue.

The Nigeria Upstream Petroleum Regulatory Commission (NUPRC) recently released data showed that Nigeria produced a total of 566.79 million barrels of crude oil and Condensate in 2024. According to the report, Nigeria highest production was in December 2024, a total of 51,694,357 in crude oil and condensate. The country’s lowest production was recorded in April with a total of 43,423,051 barrels produced in crude oil and condensate. On daily average production, Nigeria recorded its highest daily average in November with an average of 1.69 million barrels produced per day.

We await the release of statistical reports from the CBN for the year ended 2024.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity remained tight this week, primarily due to net Cash Reserve Ratio (CRR) debit activities, and foreign exchange settlements. Despite some improvements from OMO maturities and Remita inflows, liquidity stayed negative, closing at -₦397.79billion. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) rose by 504bps and 489bps to 32.33% and 32.75%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 4bps to 25.23% against 25.27% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor and Long-tenor Bonds increased by 31bps, 43bps and 4bps to 20.30%, 20.70% and 18.08% respectively.

The Federal Government Treasury Bill Auction is scheduled to hold next week on Wednesday 22nd January 2025, with an offer size of ₦530billion across tenors.

We expect cautious trading activity as participants prepare for the NTB auction next week.

THE EQUITIES MARKET

Market Capitalization and All-Share Index decreased by 2.26% and 2.94% to close at ₦62.85trillion from ₦64.30trillion and 102,353.68 from 105,451.06 the previous week.

A total turnover of 2.25 billion shares worth ₦58.83billion in 63,657 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 4.70 billion shares valued at ₦85.04billion that exchanged hands last week in 72,562 deals. On a sectoral basis, the Banking, Insurance, Oil and Gas and Industrial Goods indices all closed negative at -0.46%, -6.23%, -0.78% and -8.20%, respectively. The Consumer Goods index was the sole gainer, closing at 1.33%.

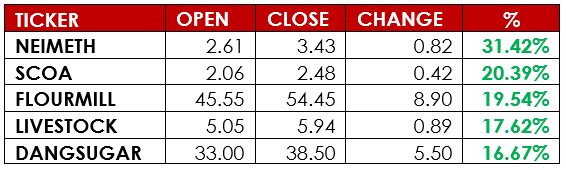

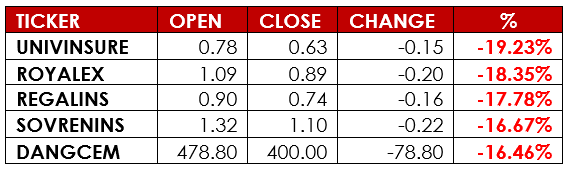

Notable gainers this week were Neimeth International Pharmaceuticals Plc and SCOA Nig. Plc, while notable losers were Universal Insurance Plc and Royal Exchange Plc.

We expect reduced activities in the equities market as Investors shift their attention to upcoming the Treasury Bills Auction.

CURRENCY

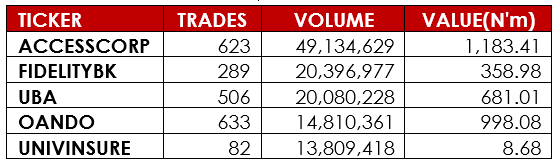

TOP TRADES BY VOLUME

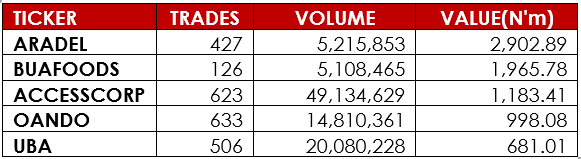

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research