GLOBAL ECONOMY

US inflation accelerated for the second straight month, reaching 2.70% annually from 2.40% in May and 0.30% monthly driven by rising import costs from new tariffs and a rebound in gasoline prices. Core inflation rose to 2.90% from 2.80% in May, with notable increases in medical care, transportation services, and household furnishings. President Trump called on the Federal Reserve to slash interest rates to 1% from the current 5.25–5.50%, aiming to reduce federal debt servicing costs, despite economists warning this could reignite inflation. Trade tensions escalated as the U.S. imposed a 17% tariff on Mexican tomatoes, which supply 70% of the U.S. market.

The British pound hovered near an eight-week low at £1/$1.34 amid mixed economic signals and uncertainty over future Bank of England rate cuts. UK inflation rose to 3.60%, the highest since January 2024, driven by transport and food prices, while core inflation hit 3.70%. Retail sales jumped 2.70% year-on-year, fueled by warm weather and summer events. However, the labour market showed signs of strain with unemployment rising to 4.70%, the highest since 2021, and payrolled employment falling for the fifth straight month. Wage growth slowed to 5%, though real wages rose by 1%. Meanwhile, the UK secured a trade deal with Vietnam to ease pharmaceutical exports, expected to generate £250million over five years.

The Euro fell to a two-week low near €1/$1.17 after President Trump announced a 30% tariff on EU and Mexican imports starting August 1, prompting the EU to delay retaliatory measures while pursuing negotiations. Eurozone inflation held steady at 2% in June, matching the ECB’s target, with core inflation at 2.30%. Industrial production rebounded 1.70% month-on-month in May, while annual output surged 3.70%, led by energy and consumer goods. The Eurozone’s trade surplus widened to €16.20billion, driven by rising exports and falling energy imports. However, the current account surplus narrowed sharply to €1.00billion. Meanwhile, the EU advanced trade talks with Indonesia, aiming to boost cooperation in agriculture and automotive sectors.

The offshore Yuan strengthened past ¥7.18/$1, China’s GDP grew by 5.20% year-on-year and 1.10% quarter-on-quarter, slightly beating expectations. Industrial output rose by 6.80%, while exports grew 5.80% and imports rebounded 1.10%, narrowing the trade gap with key partners. The unemployment rate held steady at 5.00%, its lowest since November 2024, while youth unemployment dropped to 14.50%. Retail sales growth slowed to 4.80%. Credit activity surged, with banks issuing 2.24 trillion in new loans and total social financing reaching CNY ¥4.20trillion. Meanwhile, trade talks with the U.S. progressed, though uncertainty remains ahead of the August 12 tariff deadline.

Investors globally will focus on US trade negotiations, key economic data releases, and major central bank decisions from the Fed, ECB, Russia.

GLOBAL MARKETS

Last week, US stocks closed near the flatline on Friday as investors weighed President Trump’s push for higher tariffs on the European Union against strong economic data and corporate earnings. Compared to last week, the Dow Jones index decreased by -0.07%, to close at 44.342.19 while the Nasdaq and S&P indices Increased by 1.51% and 0.59% to close at 20,895.65 and 6,296.79 respectively.

In the UK and across Europe, major stocks slipped to trim initial gains during the week as Investors monitored the corporate developments and the signs of progress in trade Negotiations. The London’s Financial Times Stock Exchange (FTSE) 100 and Germany’s Deutscher Aktien (DAX) indices increased by 0.54% and 0.18% to 8,989.53 and 24,297.86, while the France Cotation Assistéeen Continu (CAC) 40 decreased by -0.08% to 7,822.67 respectively.

The Asian stock market closed high last week with mainland stocks extending gains with China’s top leaders making a commitment to curb aggressive price cutting to combat deflation. The Hang Seng and Topix indices increased by 2.84% and 0.40% to 24,825.66 and 2,834.48 respectively.

This week, Investors sentiments will be driven by a mix of corporate earnings key decision from Policy makers.

DOMESTIC ECONOMY

Nigeria’s Inflation Eases to 22.22% in June 2025

Nigeria’s headline inflation rate dropped to 22.22% in June 2025, down from 22.97% in May, marking a 0.75%-point decline and a sharp 11.97%-point drop from June 2024’s 34.19%. While year-on-year inflation eased, month-on-month inflation rose to 1.68%, indicating faster price increases in June. Food inflation fell to 21.97% year-on-year but rose 3.25% month-on-month, driven by rising prices of key staples. Urban inflation stood at 22.72%, while rural inflation was 20.85%. Experts attribute the easing to FX stability and contained energy prices, though food inflation remains a concern due to insecurity in key agricultural regions.

Summary of Key Developments in Nigeria’s Oil Sector and Global Market – July 2025

Nigerian crude prices rose to $72.5 per barrel, nearing the Federal Government’s benchmark, amid Middle East tensions following drone attacks on Iraqi Kurdistan oilfields that cut regional output by over 50%. Nigeria’s oil production exceeded its OPEC+ quota of 1.5 million bpd, reaching 1.505 million bpd, with total output (including condensates) at 1.7 million bpd. The Dangote Refinery’s full operations and rising West African fuel demand are reshaping regional supply dynamics. Globally, Brent crude hovered near $70, supported by seasonal demand averaging 105.2 million bpd, despite volatility from U.S. tariff uncertainty and speculative trading. Nigeria is pushing to raise its OPEC+ quota to 2 million bpd, while ExxonMobil, Shell, and TotalEnergies plan major investments in deepwater projects, signaling long-term growth potential.

FGN Savings Bond Allotment – July 2025

The Debt Management Office (DMO) successfully allotted ₦4.27billion in FGN Savings Bonds for July 2025, up from ₦4.01billion in June. The 2-year bond (maturing July 2027) was issued at a 15.76% coupon, while the 3-year bond (maturing July 2028) offered 16.76%, both lower than June’s rates. The 3-year bond attracted the bulk of subscriptions (₦3.40billion from 1,591 investors). These bonds, priced at ₦1,000 per unit with a minimum ₦5,000 investment, offer quarterly interest payments and are listed on the NGX, making them tradable and tax-exempt for qualified investors. The lower rates reflect the CBN’s steady 27.50% policy rate and growing investor appetite for secure, government-backed instruments.

Naira Weakens Ahead of MPC Meeting as Market Awaits Inflation Data

The naira depreciated to ₦1,555/$1 on the parallel market midweek, down from ₦1,550/$1 earlier in the week, while the official rate slightly appreciated to ₦1,528.65/$1. This comes ahead of the CBN’s 301st Monetary Policy Committee (MPC) meeting scheduled for July 21–22, 2025, where we expect a cautious stance amid inflation concerns. Meanwhile, with the June 2025 inflation report, at 22.22%, driven by FX stability and seasonal food supply. The CBN previously held the MPR at 27.50%, maintaining tight monetary conditions to curb inflation and stabilize the naira.

Nigeria Hits 1.51 million barrels per day Oil Output in June, Retains Top Spot in Africa — OPEC

Nigeria’s crude oil production rose to 1.51 million barrels per day (bpd) in June 2025, a 3.58% increase from May’s 1.45 million bpd, marking the highest level since January and meeting OPEC’s 2025 quota for the second time. Secondary sources estimated output to be even higher at 1.55 million bpd. Nigeria maintained its lead as Africa’s top oil producer, ahead of Algeria’s 927,000 bpd. OPEC plans to boost output by 548,000 bpd in August, while OECD oil inventories rose to 2,771 million barrels in May. OPEC warns of a potential 23 million bpd global supply shortfall by 2030 without $17.40trillion in upstream investment.

CBN to Hold Crucial MPC Meeting July 21–22 Amid Inflation, FX Concerns.

The Central Bank of Nigeria (CBN) will convene its 301st Monetary Policy Committee (MPC) meeting on July 21–22, 2025, at its Abuja headquarters, with Governor Olayemi Cardoso set to announce key policy decisions. The meeting follows May’s decision to hold the Monetary Policy Rate at 27.50%, alongside a 50% CRR for banks and a 30% liquidity ratio. Analysts anticipate a possible policy shift as the committee weighs inflation, forex stability, and economic growth. The outcome will be closely watched by investors and markets for signals on Nigeria’s monetary direction.

This week, Investors will closely monitor macroeconomic data releases and the outcome of the 301st Monetary Policy Committee meeting.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity closed Negative last week due to the absence of OMO auction and Treasury Bills Auction. The Short-term rates closed higher, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) increased by 83bps and 50bps to 32.33% and 32.67% respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased further by 70bps to 16.23% last week. In the Bonds market, the average yield for the short-tenor, mid-tenor and long-tenor bonds decreased by 89bps, 21bps and 30bps to 16.78%, 16.61% and 15.90% respectively.

We anticipate bullishness in the Market driven by the easing of Inflation in June.

EUROBONDS MARKET

This week, the Nigeria Sovereign Eurobond market extended its bearish trajectory, reversing early mixed sentiment amid renewed global risk aversion. The downturn was primarily driven by a decline in global oil prices, following a buildup in US crude inventories; an event that dampened investor confidence in oil-dependent issuers like Nigeria. As a result, the average yield on Nigeria’s Eurobonds climbed by 11bps to 8.61%, reflecting offshore investor sell-offs and a cautious stance toward Emerging Market debt, despite signs of macroeconomic improvement on the domestic front.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 4.31% to close the week at 131,585.66 and ₦83.24trillion respectively, compared to 126,149.59 and ₦79.80trillion last week.

A total turnover of 17.498 billion shares worth ₦500.76billion in 142,082 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 5.39 billion shares valued at ₦107.81billion that exchanged hands last week in 134,390 deals.

On a sectoral basis, the Banking, Insurance, and Consumer Goods indices closed positive at 5.36%, 19.17%, and 1.34%, while Industrial Goods and Oil and Gas indices closed negative at -3.65%, and -0.76%.

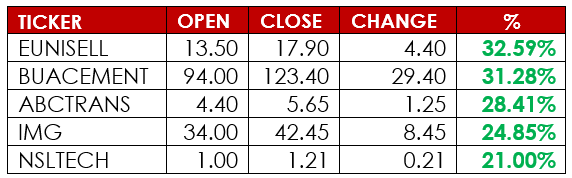

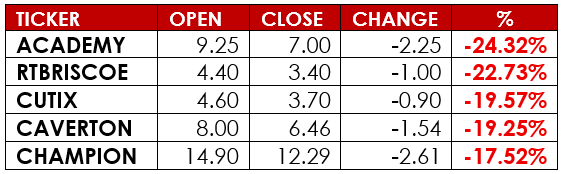

Notable gainers this week were Eunisell Interlinked PLC and Bua Cement PLC, while notable losers were RT Briscoe PLC and Academy Press PLC.

This week, Investors will watch out for corporate earnings update and the MPR outcome.

CURRENCY

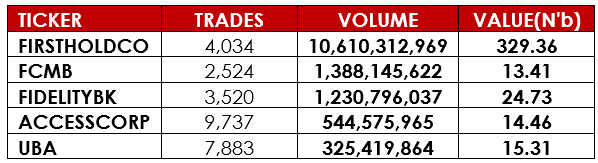

TOP TRADES BY VOLUME

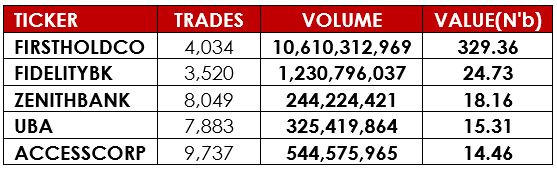

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst utmost care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.