GLOBAL ECONOMY

The US GDP grew by 3.00% in Q2 2025, rebounding strongly from a 0.50% contraction in Q1 2025. The growth was driven by a 30.30% plunge in imports, reversing the Q1 surge as businesses had previously stockpiled goods ahead of tariff hikes. Consumer spending also picked up (1.40% vs. 0.50% in Q1), while government spending rebounded modestly. Despite the strong Q2 rebound, the Federal Reserve (Fed) has revised its full-year 2025 growth forecast down to 1.40%, citing ongoing trade tensions and investment weakness. The US economy is now facing growing uncertainty as President Trump announced sweeping global tariffs, including a 10% baseline and up to 41% on countries without trade deals.

The British Pound rebounded slightly to £1/$1.33 but still dropped by 3.80% month-on-month amid growing expectations of a Bank of England rate cut in August due to weak growth prospects. Manufacturing Purchasing Managers Index (PMI) edged up to 48 in July 2025 from 47.70 in June 2025, the mildest contraction since January, supported by gains in consumer and intermediate goods, though export challenges and labor cost pressures persisted.

The Euro weakened to €1/$1.15 amid rising expectations of a US Fed rate cut. The Eurozone economy grew by 0.10% quarter-on-quarter, down from 0.60% in Q1 2025, with Germany and Italy contracting by 0.10% each, while Spain and France posted modest growth. The Eurozone GDP rose by 1.40% year-on-year, led by Ireland (16.20%) and Lithuania (3.00%). Despite trade tensions with the US and a new 15% tariff on EU exports, Consumer Inflation held steady at 2.00%, matching the European Central Bank’s target, while unemployment remained at a record low of 6.20%, with youth unemployment falling to 14.10%.

The offshore Yuan weakened past ¥7.21/$1 after President Trump imposed sweeping tariffs, including 41% on non-trade-deal countries. Meanwhile, Manufacturing PMI also contracted sharply to 49.50 points in July 2025 from 50.40 points in June 2025, signaling a broader economic slowdown entering Q3. The official Non-Manufacturing PMI also dropped to 50.10 points from 50.50 points amidst weak domestic and foreign demand, adverse weather, and escalating U.S. trade tensions.

Investors globally will monitor developments on President Trump’s trade war.

GLOBAL MARKETS

This week, US stocks closed mixed as Investors reacted to a weak July jobs report and a fresh round of tariffs announced by President Trump. Compared to last week, the S&P 500 and Dow Jones indices closed lower, decreasing by -2.38% and -2.92% to close at 6,238.01 and 43,588.58. The Nasdaq index, however, increased by 7.84% to close the week at 22,763.31.

In the UK and across Europe, major stocks closed lower following decline in global Equities as tariff imposition intensifies. London’s Financial Times Stock Exchange (FTSE) 100, Germany’s Deutscher Aktien (DAX) and France Cotation Assistéeen Continu (CAC) 40 indices decreased by -0.56%, -3.17% and -3.68% to 9,069.25, 23,450.39 and 7,546.16 respectively.

The Asian stock market closed lower this week with major stocks closing negative as Investors sentiments were influenced by weak economic data. The Hang Seng and Topix indices decreased by -3.47% and 0.11% to 24,507.81 and 2,948.65 respectively.

This week, Investors will closely monitor developments in the Tariff front while on the lookout for more data from earnings reports.

DOMESTIC ECONOMY

Nigeria’s Private Sector Employment Hits 21-Month High as PMI Climbs to 54.00 in July

Nigeria’s non-oil private sector recorded its strongest employment growth since October 2023, with the PMI rising to 54.00 in July 2025, up from 51.60 in June marking the eighth consecutive month of expansion. The surge was driven by accelerated increases in new orders and output, supported by improved customer demand and easing inflationary pressures. All five key PMI components (output, new orders, employment, stocks of purchases, and suppliers’ delivery times) showed improvement, signaling a robust start to Q3 for the economy.

Diaspora Remittances Surge to $20.93billion in 2024, Quadruple Nigeria’s FDI

President Bola Ahmed Tinubu has praised the Nigerian diaspora for their growing economic impact, revealing that remittances from abroad reached $20.93billion in 2024, an 8.90% increase from the previous year and nearly four times Nigeria’s Foreign Direct Investment (FDI). Speaking at the National Diaspora Day 2025, he highlighted diaspora contributions across key sectors like Healthcare, ICT, and Real Estate. The World Bank noted Nigeria accounted for 37% of Sub-Saharan Africa’s total remittances, underscoring the diaspora’s role as vital economic drivers and global ambassadors.

AfDB Commits $1.20million for Nigeria’s Battery Storage Study to Boost Clean Energy Transition

The African Development Bank (AfDB) has granted $1.20million under its Energy Transition Catalyst Programme to fund a feasibility study on Nigeria’s Battery Energy Storage System (BESS), aimed at stabilizing the national grid and integrating renewable energy. Announced at a workshop in Abuja, the study jointly led by the Transmission Company of Nigeria (TCN) and AfDB will assess grid integration, investment models, and technical capacity needs. AfDB’s Dr. Abdul Kamra emphasized the role of battery storage in frequency stabilization and peak load management, aligning with Nigeria’s Energy Transition Plan and the broader Mission 300 goal to connect 300 million Africans to electricity by 2030.

Manufacturers Push for Rate Cuts Amid High Borrowing Costs and Weak Capacity

The Manufacturers Association of Nigeria (MAN) this week called for a rate cut, citing worsening business conditions like lending rates remaining above 30% and capacity utilization dropping below 60%. With inflation trending lower and the Naira stabilizing, Manufacturers argue that easing policy could stimulate investment and employment. However, the CBN has signaled it will prioritize price stability until inflation falls further.

Next week, Investors in Nigeria will be closely watching for key economic signals and data releases.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity closed positive this week at ₦1.61trillion despite outflows from the FGN Bond and OMO auction by the CBN. Consequently, the Short-term rates closed low, as the Open Repo Rate (ORR) remained unchanged at 26.50% while the Overnight Rate (O/N) decreased by 2bps to 26.90% respectively.

The Nigerian Treasury Bills (NTB) market average yield increased week-on-week by 7bps to 16.27%. In the Bonds market, the average yield for the mid-tenor bond increased by 37bps to 16.55%, while the short-tenor and long-tenor bonds average yields decreased by 22bps and 9bps to 16.56% and 15.74% respectively.

FGN Offers ₦80Billion in Bonds at July 2025 Auction Amid Strong Investor Demand

The auction witnessed high demand, with a bid-to-cover ratio of 1.62x. Total subscription was 3.76x the offer, at ₦300.67billion. The Debt Management Office (DMO) sold a total of ₦185.93billion, thus the auction was oversold by ₦105.93billion. The stop rate for FGN 2029 and FGN 2032 Bonds decreased by 206bps and 205bps to 15.69% and 15.90% respectively.

This week, Investors focus will shift to the Treasury Bills Auction holding on 6th August 2025, where the DMO is offering ₦220billion across tenors, against ₦258.63billion maturing.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 5.07% and 5.08% to close the week at 141,263.05 and ₦89.37trillion compared to 134,452.93 and ₦85.06trillion last week.

A total turnover of 4.85 billion shares worth ₦149.76billion in 174,267 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 3.69 billion shares valued at ₦112.26billion that exchanged hands last week in 138,250 deals.

On a sectoral basis, the Banking, Consumer Goods and Industrial Goods indices closed positive at 3.49%, 2.72% and 10.12% while Insurance and Oil and Gas indices closed negative at -1.22% and -0.48% respectively

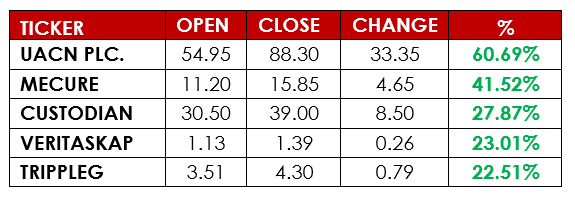

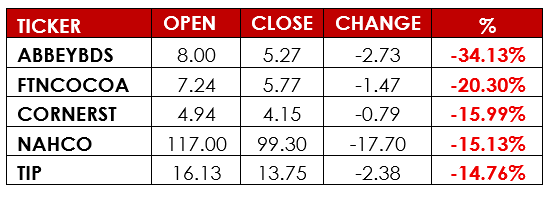

Notable gainers this week were United Africa Company of Nigeria (UACN) PLC and Mecure Industries PLC, while Notable losers were Abbey Mortgage Bank PLC and FTN Cocoa Processors PLC.

Next week, Investors will be focused on several earnings reports, and the expectation of interim dividend declarations by Tier-1 Banks. With major Banks yet to release their H1 results, Investor positioning is likely to intensify in the coming sessions.

Currency

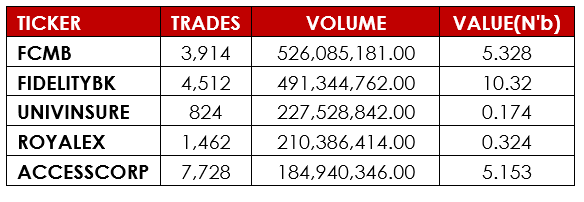

TOP TRADES BY VOLUME

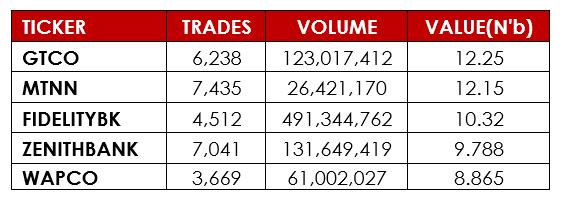

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst utmost care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication.

Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.