GLOBAL ECONOMY

The Federal Reserve (Fed) held interest rates steady at 4.25%–4.50% for the fourth straight meeting, citing persistent inflation with Personal Consumption Expenditure (PCE) at 3.00% and a downgraded GDP forecasts (1.40% for 2025 and 1.60% for 2026) following President Trump’s era of trade and fiscal uncertainties. Meanwhile, in the trade sector, export prices fell 0.90%, while import prices were flat at 0.10%, with foreign firms refusing to lower their selling prices to counter the impact of aggressive tariffs that US consumers will face.

The British Pound hovered around £1/$1.34, weighed by the Bank of England’s (BoE’s) hold decision and safe haven flows into the U.S. dollar amid Middle East conflict. Headline inflation in the UK eased to 3.40%, slightly down from April’s 3.50%, core inflation also fell to 3.50%, mainly due to a slowdown in services inflation (4.70%). The Bank of England voted 6-3 to hold interest rates at 4.25%, citing ‘two-sided risks’ from rising energy prices and potential U.S. tariffs. Public borrowing also rose to £17.70billion, pushing the public sector debt to 96.40% of GDP.

The Euro slipped below €1/$1.15 as the European Central Bank (ECB) hinted at a pause in further easing after its June rate cut, citing improved inflation dynamics but cautioning against premature optimism. Wage growth slowed to 3.40%, with notable deceleration in Germany (2.80%) and Italy (3.90%), helping to ease labor cost pressures. Hourly labor costs also rose by 3.40%, with industry seeing the softest rise at 2.50%. Consumer confidence dipped to -15.30, and retail sentiment remained fragile. The current account surplus narrowed sharply to €19.30billion, down from €60.10billion in March, as trade activity faded. Unemployment held at 6.40%, near record lows, with modest wage growth supporting domestic demand. Meanwhile, in a symbolic step toward deeper integration, Bulgaria was recommended to adopt the euro in January 2026.

The Yuan strengthened to ¥7.18/$1 as the People’s Bank of China (PBoC) held key lending rates steady at 3.00% (1-year LPR) and 3.50% (5-year LPR) after a May rate cut, signaling a pause. Foreign Direct Investment (FDI) dropped to 13.20%, totaling ¥358.19billion from ¥320.80billion in April, following strong inflows from sectors like e-commerce (+146%) and aerospace (+74.90%).

Next week, Investors will keep a close eye on the approaching end of the 90-day U.S.-China tariff pause, adjusting positions in anticipation of potential trade disruptions as they monitor the tensions in the Middle East also.

GLOBAL MARKETS

Last week, U.S. stocks reversed this week as investors weighed the Fed report, holding rates but citing persistent inflation and escalating tension between Israel and Iran. Compared to last week, the Dow Jones, and Nasdaq indices increased by 0.02%, and 0.21% to close at 42,206.82 and 19,447.41 respectively, while the S&P 500 decreased by -0.15% to close at 5,967.84.

In the UK and across Europe, major stocks fell following rate cuts, concerns about weakening economy, the resumption of tariffs from July 8th and the tensions in the Middle East. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices decreased by -0.86%, -1.24% and -0.70% to 8,774.65, 7,589.66 and 23,350.55 respectively.

The Asian stock market closed mixed last week with rates at an historic low and global uncertainty driving investors sentiments. The Hang Seng index decreased by -1.52% to 23,530.48 while the Topix index increased by 0.54% to 2,771.26.

This week, markets will track the Israel-Iran conflict and potential U.S. military involvement, while also watching global trade talks alongside key economic indicators from Europe and Asia.

DOMESTIC ECONOMY

Nigeria’s Inflation Eases to 22.97% in May, Driven by Naira Stability and Fuel Price Cuts

Nigeria’s headline inflation rate declined for the second consecutive month to 22.97% in May 2025, down from 23.71% in April, according to the National Bureau of Statistics. The moderation was supported by a stronger naira, reduced fuel prices, and easing logistics costs. Food inflation also slowed to 21.14%, though regional disparities persist, with states like Borno and Bayelsa still facing elevated price pressures.

UK Grants Nigeria 99% Duty-Free Export Access

The UK has reaffirmed that 99% of Nigerian exports will continue to enjoy duty-free access under the Developing Countries Trading Scheme (DCTS). Launched in 2023, the scheme covers over 3,000 products, including cocoa, shrimp, sesame, and value-added goods like palm oil and cotton clothing, aiming to boost Nigeria’s non-oil exports, support job creation, and deepen trade ties.

FAAC Shares ₦1.66Trillion in May Despite Dip, VAT and CIT Lead Revenue Surge

In May 2025, the Federation Account Allocation Committee (FAAC) distributed about ₦1.66trillion among the Federal Government (₦538.00billion), 36 states (₦577.84billion), and 774 local councils (₦419.97billion). This marked a 1.31% drop from April’s ₦1.68trillion, despite a rise in gross revenue to ₦2.94trillion. The allocation included ₦863.90billion in statutory revenue, ₦691.71billion from Value Added Tax (VAT), ₦27.67billion from Electronic Money Transfer Levy (EMTL), and ₦76.61billion from exchange differences. Notably, VAT revenue jumped by ₦100.60billion, and Companies Income Tax (CIT) and Import Duty also saw strong gains. However, Petroleum Profits Tax (PPT), oil royalties, Common External Tariff (CET) levies, and EMTL declined. The disbursement also included ₦124.08billion in derivation revenue for oil-producing states

Nigeria Unveils REV-OP to Digitally Reinvent Public Finance and Plug Revenue Leaks

Nigeria has launched the Revenue Optimization and Assurance Project (REV-OP) a bold, tech driven initiative aimed at blocking revenue leakages, boosting transparency, and modernizing public financial management. Described by Finance Minister Wale Edun as a clean break from past practices, REV-OP is built on three pillars: transparency, efficiency, and digital transformation. It introduces real-time monitoring and data-driven oversight across revenue generating agencies, supported by a two-tier governance structure for effective execution, bringing together key institutions like the FIRS, CBN, and Private Tech Partners, signaling a multi-stakeholder approach to reform. Alongside REV-OP, the government also launched the Africa Sovereign Investors Forum (ASIF) Investment Platform to unlock cross-border investments in infrastructure, renewables, and healthcare further reinforcing Nigeria’s push for sustainable, inclusive growth.

Banks Gear Up to Exit CBN Forbearance by June 30, Eye Dividend Comeback

Top Nigerian banks have announced plans to exit the Central Bank of Nigeria’s (CBN) regulatory forbearance by June 30, 2025, signaling renewed financial strength and a return to dividend payouts. The CBN had earlier imposed restrictions—such as suspending dividends and foreign investments—to help banks build capital buffers and strengthen balance sheets amid economic headwinds. This was a temporary relief framework introduced to help banks manage exposure risks and capital shortfalls during periods of economic stress. Under this arrangement, banks were allowed to exceed regulatory limits, such as the Single Obligor Limit (SOL) which caps how much a bank can lend to a single borrower and delay full provisioning for certain non-performing loans.

Now, with economic conditions stabilizing, the CBN has set a June 30, 2025 deadline for banks to exit the forbearance regime. Institutions like Fidelity Bank and Zenith Bank have announced their readiness to comply, signaling a return to regulatory normalcy and paving the way for dividend payouts and renewed investor confidence.

We anticipate the release of the Purchasing Managers Index to guide Investors decisions.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System Liquidity stayed robust during the week reaching ₦1.04trillion midweek and closing at ₦181billion due to the Treasury Bills Auction settlement. Consequently, short-term rates closed high, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) increased by 167bps and 193bps to 28.17% and 28.92% respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 265bps to 18.46% last week. In the Bonds market, the average yield for the short-tenor, mid-tenor and long-tenor bonds decreased by 25bps, 35bps and 26bps to 18.99%, 18.63% and 17.44% respectively.

We expect calm trading this week as Investors participate in the FGN Bond Auction on Monday 23rd June 2025, where the DMO is offering ₦50billion each on the FGN 2029 (Re-opening) and FGN 2032 (New) Bonds.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 2.40%to close the week at 118,138.22 and ₦74.53trillion, compared to 115,429.54 and ₦72.79trillion last week.

A total turnover of 3.57 billion shares worth ₦115.40billion in 99,960 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 2.06 billion shares valued at ₦51.02billion that exchanged hands last week in 65,016 deals.

On a sectoral basis, the Banking, Insurance and Oil and Gas, Consumer Goods indices closed positive at 3.58%, 2.37%, 5.27% and 2.16%, while Industrial Goods index closed negative at -0.36%.

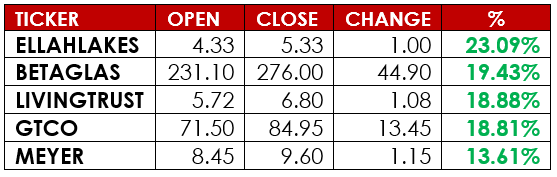

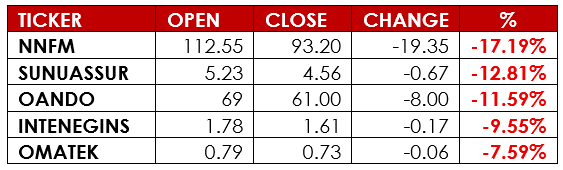

Notable gainers this week were Ellah Lakes and Beta Glass PLC, while notable losers were Northern Nigerian Flour Mill and Sunu Assurance PLC.

With the CBN Forbearance deadline approaching, Investors are watching how this impacts dividend policies, recapitalization plans, and market sentiment.

CURRENCY

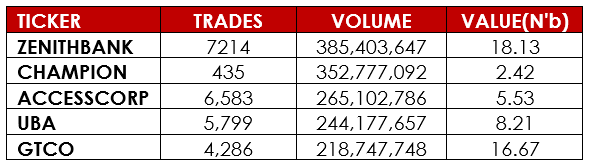

TOP TRADES BY VOLUME

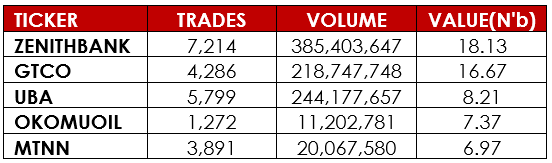

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.