GLOBAL ECONOMY

The US Services PMI fell to 49.70 in February 2025 from 52.90 in the previous month, below expectations of 53.00 to indicate a contraction in the services sector. Firms cite the decline to political uncertainty, notably due to spending cuts and pro-inflationary policies by the new Presidential administration. The US Composite PMI also dropped to 50.40 in February 2025 from 52.70 in January, indicating near-stagnation in the private sector, driven by a contraction in services output as new orders growth weakened. Finally, business optimism fell to its lowest since December 2022, with concerns over Government policies related to domestic spending cuts and tariffs, as well as worries over higher prices, and broader geopolitical developments.

The United Kingdom’s unemployment was unchanged at 4.40% from October to December 2024, contrary to expectations of a rise to 4.50%. The UK inflation figures also came higher than expected as the annual inflation rate increased to 3.00% in January 2025, from 2.50% in the previous month, with the largest contributions coming from transport given the rise in prices of air fares and motor fuel. However, Bank of England Governor Andrew Bailey toned down the inflation spike, calling it a short-term issue rather than a sign of deeper economic problems. He attributed the rise mainly to regulated costs such as energy bills, suggesting it won’t be as harsh as previous inflation surges.

Across Europe, France’s annual inflation rate rose to 1.70% in January 2025, up from 1.30% in December. This marks the highest level since last August, driven by faster price growth in services and energy. In addition, manufactured goods costs increased, due to a sharp rise in clothing and footwear prices. Producer Price Index in Germany increased by 0.50% year-on-year in January 2025, from 0.80% in December.

The People’s Bank of China (PBoC) carried out a series of short-term cash injections on Friday to ease a liquidity squeeze that has unsettled the bond market. The Central Bank injected a net ¥84billion through daily Open Market Operations (OMO). On the monetary rates, the PBOC chose to keep its key lending rates unchanged for the fourth consecutive month in February 2025, with the one-year loan prime rate holding steady at 3.10%, while the five-year loan prime rate remained at 3.60%.

Next week in the US, investors will focus on key economic data releases, including Personal Income and Spending, PCE Price indices and the second estimate of Q4 GDP growth.

GLOBAL MARKETS

US stocks fell on Friday as released economic data raised concerns about a slowing US economy and persistent inflation, prompting investors to seek safer assets. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices decreased by -2.26%, -1.66% and -2.51% to 21,614.08, 6,013.13 and 43,428.02, respectively.

In the UK and across Europe, concerns about rising unemployment and inflation weighed on Investors sentiment, leading to losses from record highs earlier in the week as markets assessed the latest inflation data and corporate returns. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices decreased by -0.84%, -0.29% and -1.00% to 8,659.37, 8,154.51 and 22,287.56, respectively.

Chinese stocks closed high as Chinese technology and artificial intelligence-related stocks continued to attract strong market interest. In Japan, Core inflation increased to 3.20% in January, up from 3.00% in December, leading to negative Investor sentiment. The Hang Seng index increased by 3.79% to 23,477.92 while the Japanese Topix index fell by -0.82% to 2,736.53.

We expect cautious trading in the Global Equities market as Investors reassess the impact of released economic data in the US and UK.

DOMESTIC ECONOMY

Nigeria’s headline Inflation rate dropped to 24.48% year-on-year in January 2025, following the rebasing of the Consumer Price Index (CPI) compared to 34.80% in December 2024 which was calculated using the previous methodology. The report from the National Bureau of Statistics (NBS) highlights that urban inflation stood at 26.09%, while rural inflation was recorded at 22.15%. The rebased food inflation index stood at 26.08% year-on-year, down from 39.84% in December 2024. Similarly, the core inflation rate, which excludes volatile agricultural produce and energy prices, stood at 22.59% year-on-year in January 2025.

The Central Bank of Nigeria’s (CBN) Monetary Policy Committee (MPC) voted to hold all key rates steady, keeping the Monetary Policy Rate (MPR) at 27.50%. This was announced by the CBN Governor, Yemi Cardoso, at the post-MPC press briefing on Thursday. The decision reflects the committee’s cautious approach to monetary policy, as it continues to evaluate macroeconomic conditions before making any adjustments. The Asymmetric Corridor was retained at +500/-100 basis points around the MPR, while the Cash Reserve Ratio (CRR) was maintained at 50.00% for Deposit Money Banks and 16% for Merchant Banks with Liquidity Ratio unchanged at 30.00%.

Nigeria’s broad money supply (M3) rose to ₦110.98trillion in January 2025, marking a 17.30% year-on-year increase from ₦94.61trillion recorded in January 2024. This expansion highlights the growing liquidity in the economy, fueled by both net foreign assets and net domestic assets. Net foreign assets stood at ₦35.39trillion in January 2025, from ₦29.73trillion in January 2024, reflecting a 19.04% increase. Similarly, net domestic assets grew by 16.53% to ₦75.59trillion, compared to ₦64.87trillion in January 2024.

Nigeria’s non-oil revenue rose to ₦1.90trillion in November 2024, marking a 16.40% increase compared to ₦1.63trillion in October. The rise was due to higher receipts from corporate tax and customs & excise duties. Increased business activity, improved tax compliance, and stricter enforcement of customs regulations contributed to the substantial revenue boost. Oil revenue also experienced an increase, rising by 42.63% to ₦0.52trillion in November, driven by improved collections from Petroleum Profit Tax (PPT), royalties, and Company Income Tax (CIT) from upstream operations.

We await the release of the Gross Domestic Product (GDP) growth rate for Q4, 2024 to provide insights into the Nigerian economy performance at the end of 2024.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity remained negative for the second consecutive week, despite inflows of FGN bond coupon payments, although at better levels as it opened at -₦722.58trillion on Friday, compared to -₦3.10trillion last week. The Open Repo Rate (ORR) decreased by 12bps to 32.33% while the Overnight Rate (O/N) increased by 3bps to 32.83%.

The Nigerian Treasury Bills (NTB) market average yield decreased by 184bps to 20.23% against 22.07% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor and Long-tenor Bonds decreased by 76bps, 84bps and 44bps to 19.78% and 19.45% and 18.27%.

The Nigerian Treasury Bills Auction held this week, with an offer of ₦700billion. The total subscription was ₦2.41trillion and total allotment was ₦774.13billion, thus, the auction was oversold by ₦74.13billion. Stop rates decreased by 100bps, 150bps and 189bps to 17.00%, 18.00% and 18.43% for the 91-day, 182-day and 364-day bills, respectively.

We expect a muted session on Monday, as investors shift their attention to the FGN Bond Auction, where the DMO plans to offer ₦200billion for the April 2029 Bond and ₦150billion for the February 2031 Bond.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 0.29% and 0.41% to close at ₦67.61trillion from ₦67.42trillion and 108,497.40 from 108,053.95 the previous week.

A total turnover of 2.00 billion shares worth ₦9.49billion in 70,853 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 2.41 billion shares valued at ₦55.51billion that exchanged hands last week in 80,988 deals. On a sectoral basis, the Insurance, Consumer Goods and Industrial Goods indices closed positive this week, at 1.47%, 6.55% and 0.05%, while the Banking and Oil and Gas indices closed negative for the second week at -3.22% and -2.87%.

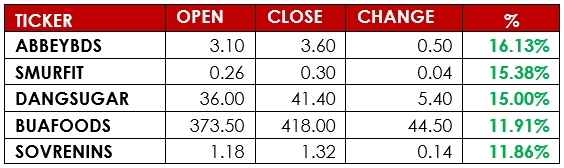

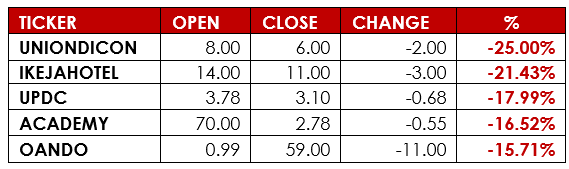

Notable gainers this week were Abbey Mortgage Bank Plc and Smart Products Nigeria Plc, while notable losers were Union Dicon Salt Plc and Ikeja Hotel Plc.

We expect mixed sentiments next week, as Investors reassess macroeconomic data and adjust positions ahead of earnings and corporate actions

CURRENCY

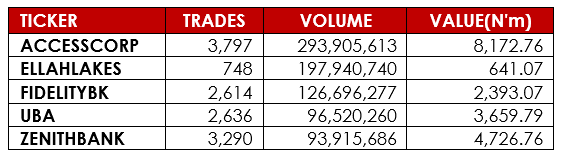

TOP TRADES BY VOLUME

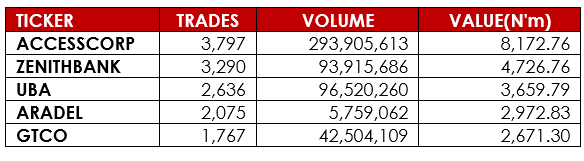

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, BusinessDay, Alpha10 Research