GLOBAL ECONOMY

The Federal Reserve (Feds) kept the federal funds rate unchanged at 4.25%-4.50% during its March 2025 meeting, extending the pause in its rate-cut cycle that began in January. The Feds also noted, at the post-meeting brief that uncertainty concerning the economy had increased but they still plan to reduce interest rates by around 50bps before the end of the year. Initial jobless claims rose by 2,000 to 223,000 in the second week of March, below market expectations of 224,000. The results continued to indicate that the US holds a robust labor market despite the prolonged period of restrictive monetary policy and the pessimistic data released during the first quarter of the year.

The Bank of England (BoE) voted 8-1 to keep the Bank Rate at 4.50% this week, as policymakers adopted a cautious approach amid high inflation and global economic uncertainties. One member – Swati Dhingra – suggested a 25bps reduction to 4.25%. The bank highlighted that given the inflation outlook, a gradual and cautious approach to further withdrawal of monetary policies remains appropriate. The Unemployment rate also remained at 4.40% from November to January 2025.

The Euro Area’s Consumer Price Inflation (CPI) rate fell to 2.30% in February 2025, down from 2.50% in January, while it rose 0.40% month-on-month in February 2025, compared to a 0.30% fall in January 2025. Despite the decline, inflation remains above the European Central Bank’s 2.00% target.

The People’s Bank of China (PBoC) maintained its key lending rates unchanged for the fifth consecutive month in March. The one-year loan prime rate (LPR), a benchmark for most corporate and household loans, was held at 3.10%, while the five-year LPR, a reference for property mortgages, remained at 3.60%. On the fiscal front, Beijing rolled out more stimulus measures to boost domestic demand and consumption and mitigate the impact of rising tariffs imposed by the US Trump administration.

Next week in the US, Investors will closely monitor speeches by several Federal Reserve officials in the United States, along with key economic data releases (personal income and spending, PCE price indices, and the final reading of Q4 GDP growth).

GLOBAL MARKETS

US Stocks closed positive on Friday, as President Trump suggested some leniency on tariffs, while several Megacap stocks made recoveries. The Nasdaq, S&P 500 and Dow Jones indices increased by 0.25%, 0.51% and 1.20% to 19,753.97, 5,667.56 and 41,985.35, respectively.

European shares closed mixed this week as markets digested a batch of monetary policy decisions. The London’s Financial Times Stock Exchange (FTSE) 100 and France Cotation Assistée en Continu (CAC) 40 indices increased by 0.17% and 0.18% to 8,646.79 and 8,042.95, while Germany’s Deutscher Aktien (DAX) decreased by -0.41% to 22,891.68.

Chinese stocks closed lower as investors engaged in profit-taking, as Beijing announced a special action plan to boost consumer spending with few details, while the People’s Bank of China kept key lending rates unchanged. Sentiment was further dampened by the approaching April 2 deadline for US President Donald Trump’s reciprocal tariffs on countries that have imposed levies on US goods. The Hang Seng index decreased by -1.13% to 23,689.72, while the Topix index increased by 3.25% to 2,804.16.

We expect mixed sentiments to persist in the Global Equities Market amidst ongoing trade tensions among major economies.

DOMESTIC ECONOMY

Nigeria’s inflation rate declined to 23.18% in February 2025, a decrease from 24.48% recorded in January 2025 following the rebasing exercise, according to the Inflation data released by the National Bureau of Statistics (NBS) for February 2025. Year-on-year, the Headline inflation rate was 8.52% lower than the rate recorded in February 2024 at 31.70%. On a month-on-month basis, the Headline inflation rate in February 2025 was 2.04%, with food inflation rate in February 2025 at 23.51% compared to 37.92% recorded in February 2024.

The Nigeria Extractive Industries Transparency Initiative (NEITI) released information showing that the Federation Accounts Allocation Committee (FAAC) disbursed a total of ₦15.26trillion to the federal, state, and local governments in 2024. The total FAAC disbursements, including derivation revenue, reflecting a 40% increase from ₦10.90trillion in 2023. The report attributed the surge in revenue disbursements to the Federal Government’s fiscal reform policies, particularly the removal of fuel subsidies and the adjustment of foreign exchange rates which significantly boosted oil revenue remittances, a major driver of the increased allocations.

Nigeria’s total debt service payments dropped significantly from $540million in January 2025 to $276million in February 2025, according to the Central Bank of Nigeria (CBN)’s latest data on external sector payments. This decline comes amid ongoing efforts by the Federal Government to restructure its debt portfolio, improve dollar liquidity, and ease pressure on the foreign exchange market. These repayment figures highlight the increasing strain of debt obligations on Nigeria’s external reserves and overall fiscal sustainability, amid speculations that recent debt repayment deferrals and negotiations with multilateral lenders may have contributed to the lower outflows for the month of February.

We anticipate continued intervention by the CBN to support the Naira, given the prevailing exchange rate pressures.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity remained negative throughout the week, despite inflows from FGN Bond coupons, closing at a deficit of -₦1.96trillion compared to -₦956.03billion last week. The Open Repo Rate (ORR) remained unchanged at 32.40% while the Overnight Rate (O/N) increased by 10bps to 32.90%, week-on-week.

The Nigerian Treasury Bills (NTB) market average yield increased by 9bps to 18.97% against 18.88% last week. In the Bonds market, the average yield for the Short-tenor Bonds decreased by -1bp to 19.23%, while the average yield for the Medium-tenor and Long-tenor Bonds increased by 16bps and 3bps to 18.83% and 17.60%, respectively.

The Nigerian Treasury Bills Auction held this week, with an offer of ₦800billion across tenors. The total subscription was ₦902.04trillion and total allotment was ₦503.92billion, thus, the auction was undersold by ₦296.08billion. Stop rates increased by 100bps, 71bps and 155bps to 18.00%, 18.50% and 19.94% for the 91-day, 182-day and 364-day bills, respectively.

We anticipate a subdued start to the week as investors turn their attention to Monday’s FGN bond auction, where the DMO will offer ₦300 billion across the APR 2029 (₦200billion) and MAY 2033 (₦100billion) papers, and the subsequent Treasury Bills Auction.

THE EQUITIES MARKET

Market Capitalization and All-Share Index decreased by -0.80% and -0.94% to close the week at ₦65.82trillion from ₦66.35trillion and 104.962.96 from 105,955.13 the previous week.

A total turnover of 2.90 billion shares worth ₦48.06billion in 57,044 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 3.28 billion shares valued at ₦63.52billion that exchanged hands last week in 60,782 deals. On a sectoral basis, the Banking, Oil and Gas, Insurance and Industrial Goods indices closed negative, at -2.55%, -1.08%, -2.87% and -3.39%, while the Consumer Goods Index closed positive at 0.06%.

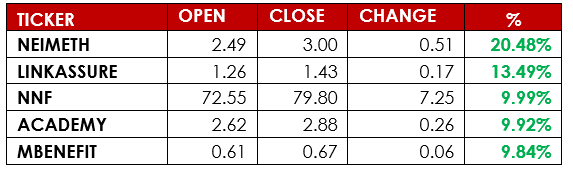

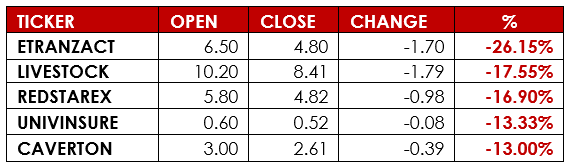

Notable gainers this week were Neimeth International Pharmaceuticals Plc and Linkage Assurance Plc, while notable losers were E-Tranzact International Plc and Livestock Feeds Plc.

We anticipate cautious trading in the Equities Market, as investors await corporate actions announcements from Banking Companies.

CURRENCY

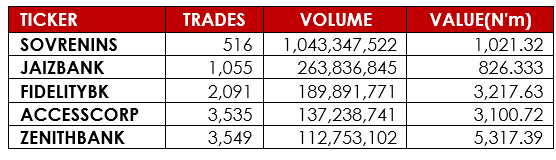

TOP TRADES BY VOLUME

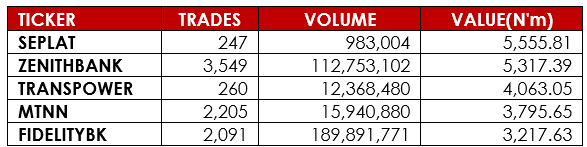

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research