GLOBAL ECONOMY

Global markets showed resilience despite inflationary pressures from tariffs. The United States maintained its ‘AA+’ rating from S&P as tariff revenues provided fiscal support. President Trump expanded 50.00% tariffs on steel and aluminium to 407 new product categories, including auto parts, chemicals, and furniture components, while announcing a planned peace summit between Russia and Ukraine. Federal Reserve Chair Powell signalled openness to a rate cut in September. Jobless claims rose to 235,000.00, while the Manufacturing Purchasing Managers Index rebounded to 53.30 and the Composite PMI hit a 2025 high of 55.40, driven by factory output and hiring.

UNITED STATES

The US dollar remained steady as tariffs were broadened across new categories—the Fed. Chair Powell signalled openness to a September cut as the Federal Open Market Committee FOMC minutes were released during the week. Manufacturing rebounded as the Purchasing Managers Index rose to 53.30 quarter-on-quarter, while the Composite PMI reached 55.40. Jobless claims rose to 235,000.00, with continuing claims at 1.97 million.

UNITED KINGDOM

The British Pound strengthened to £1.00/$1.35 as services posted their strongest rebound in a year. Inflation surged to 3.80% year-on-year in July 2025, the highest since January 2024, largely due to a 30.20% jump in airfares. Manufacturing weakened further with PMI slipping to 47.30 in August 2025 from 48.00 in July 2025, while the Composite PMI rose to 53.00 from 51.50 in the previous month, led by services at 53.60.

EUROZONE

The Euro traded around €1.00/$1.17, holding its 11.00% rally year-to-date. Inflation remained stable at 2.00% year-on-year, with core inflation at 2.30%. The trade surplus narrowed to €7.00 billion in June 2025 from €20.70 billion a year earlier, as imports rose 6.80% and exports increased 0.40%. The Composite PMI rose to 51.10, Manufacturing PMI to 50.50, while Services PMI softened slightly to 50.70. A new US-EU trade deal capped tariffs at 15.00%, averting threatened 30.00% levels.

CHINA

The offshore Yuan held steady at ¥7.18/$1. Foreign Direct Investment declined 13.40% year-on-year to ¥467.34 billion from ¥539.57 billion. Industrial output and retail sales weakened as youth unemployment spiked to 17.80%, lifting the overall jobless rate to 5.20%. The 1-year Loan Prime Rate remained at 3.00%, while the 5-year held at 3.50%. Fiscal revenue edged up 0.10% to ¥13.58 trillion, while expenditure rose 3.40%. Rare earth exports rebounded 75% in July, signalling easing restrictions after the US and Europe deal.

GLOBAL MARKETS

- US equities closed mixed. The S&P 500 rose 0.27% to 6,466.91, the Dow Jones climbed 1.53% to 45,631.74, while the Nasdaq declined -0.58% to 21,496.54.

- In Europe, the FTSE 100 gained 2.00% to 9,321.40, DAX edged 0.02% higher to 24,363.09, and CAC 40 rose 0.58% to 7,969.69.

- Asian markets were mixed, with the Hang Seng up 0.27% to 25,339.14 and Topix down -0.22% to 3,100.87.

NIGERIAN ECONOMY

- Foreign Exchange Reserves Increased to $41.08 billion, the highest since December 2021, driven by a 24% rise in July FX inflows and strong non-bank corporate participation.

- The Naira depreciated slightly by 0.16% to ₦1,535.04/$1 (NAFEM) from ₦1,532.51/$1. The parallel market closed at ₦1,545.00/$1.

- FAAC disbursement records ₦2.00 trillion shared in July 2025, up from ₦1.81 trillion in June, with ₦1.28 trillion statutory revenue and ₦640.61 billion VAT.

DOMESTIC MARKETS

Bonds: The bond market traded mixed throughout the week. The average yield for the mid-tenor and long tenor bonds increased by 39 bps and 16 bps to 17.11% and 15.86% while the short-tenor bonds decreased by 1bp to 16.64%.

Nigerian Treasury Bills: The average yield for Nigerian Treasury Bills (NTB) rose by 20 bps to 18.21% week-on-week. The recent auction saw strong demand for the long tenor bill, with total subscriptions at ₦396.42 billion, 1.72x the offer. The bid-to-cover ratio was 1.30x, and total allotment reached ₦303.79 billion, overselling by ₦73.79 billion. Stop rates for the 182-day bill remained steady, while the rates for the 91-day and 364-day bills increased by 35 bps and 94 bps to 15.35% and 17.44%, respectively.

Equities Market

- The NGX All-Share Index and Market Capitalisation depreciated by 2.51% to close the week at 141,004.14 and ₦89.21trillion compared to 144,628.20 and ₦91.50trillion last week.

- A total turnover of 4.77 billion shares worth ₦107.43billion in 152,965 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 8.56billion shares valued at ₦99.94billion that exchanged hands last week in 177,870 deals.

- On a sectoral basis, Industrial Goods, Banking, Insurance and Oil and Gas indices closed negative at 8.42%, -3.48%, -4.17%, and -0.84%, while the Consumer Goods Index was the sole gainer, closing positive at 0.83%.

CURRENCY

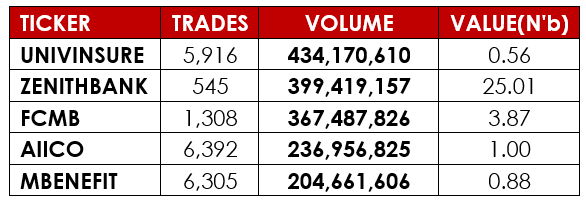

TOP TRADES BY VOLUME

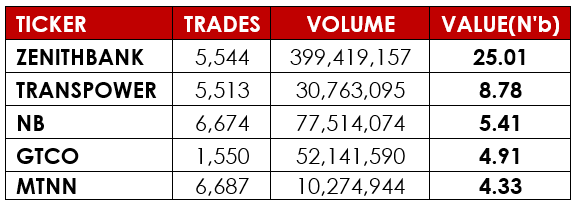

TOP TRADES BY VALUE

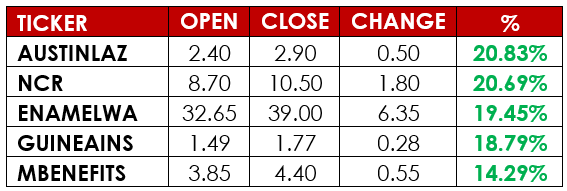

TOP GAINERS

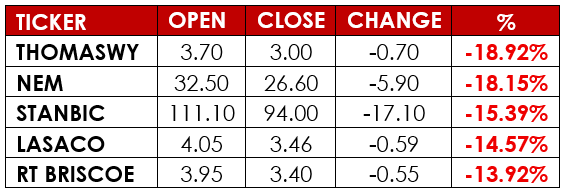

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst utmost care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication.

Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.