GLOBAL ECONOMY

The number of individuals filing for unemployment benefits in the US fell by 6,000 from the previous week to 213,000, the lowest since April, and well below market expectations of an increase to 220,000. The four-week moving average, which removes week-to-week volatility, fell by 3,750 to 217,750 as Federal Reserve Chair Powell highlighted the resilience of the labor market, despite weaker job growth in October.

Annual inflation rate in the UK went up to 2.30% in October 2024, the highest in six months, compared to 1.70% in September. This exceeded both the Bank of England’s target and market expectations of 2.20%. Public sector net borrowing in the UK also increased to £17.35billion in October 2024 from a revised £16.13billion in September and much higher than forecasts of £12.30billion.

Annual inflation in the Euro Area accelerated to 2.00% in October 2024, up from 1.70% in September. The euro slipped to €1/$1.05, pressured by a strong dollar, as traders follow Donald Trump’s political appointments for his new administration and the potential repercussions of his presidency for Europe, particularly concerning tariffs on the EU and China.

China’s 10-year government bond yield fell to around 2.08%, after the People’s Bank of China (PBoC) left its one-year loan prime rate unchanged at 3.10%, while the five-year loan prime rate also remained steady at 3.60%, in line with market expectations. The decision underlines the Central Bank’s ongoing assessment of earlier stimulus measures, with authorities increasing efforts to stimulate China’s slowing economy and meet the growth rate target of around 5.00%.

US Investors anticipate the release of the Federal Open Market Committee (FOMC) meeting minutes, PCE inflation data, personal income and spending figures, and the second estimate of Q3 GDP growth.

GLOBAL MARKETS

US stocks closed higher this week as Investors rotation from technology into economically sensitive sectors like financials, industrials, and consumer discretionary supported broader market gains. The Nasdaq, S&P 500 and Dow Jones indices all closed positive, increasing by 1.87%, 1.68% and 1.96% to 20,776.23, 5,969.34 and 44,296.51, respectively.

In Europe, Investor sentiment stabilized following four consecutive days of selling as markets assessed a batch of corporate updates, reversing four weeks of losses. The London’s Financial Times Stock Exchange (FTSE) 100 and Germany’s Deutscher Aktien (DAX) indices closed positive, increasing by -2.46% and 0.58% to 8,262.08 and 19,322.59 while the Cotation Assistée en Continu (CAC) 40 index closed slightly negative by -0.20% to 7,255.01.

In Asia, Investors grew increasingly uncertain about the effectiveness of China’s stimulus measures in driving economic growth, while fears of higher tariffs under the incoming Trump administration added further pressure to the economic outlook. The Hang Seng and Topix indices decreased by -1.01% and -0.56% to 19,229.97 and 2,696.53, respectively.

We expect cautious trading in the equities markets as Investors await minutes of the FOMC meeting and PCE inflation reading for October, 2024.

DOMESTIC ECONOMY

The Federation Accounts Allocation Committee (FAAC) has disbursed a total of ₦1.41trillion to the Federal Government, State Governments, and Local Government Councils (LGCs) for October 2024, according to a communiqué issued by the Director of Press and Public Relations, Office of the Accountant-General of the Federation. The communiqué highlighted significant increases in revenue from oil and gas royalties, excise duties, VAT, import duties, petroleum profit tax, and companies’ income tax. Conversely, revenues from the Electronic Money Transfer Levy (EMTL) and Common External Tariff (CET) levies saw considerable declines.

Nigeria’s economy ranked low on weaker currency, rising inflation and other economic challenges, according to the ‘Africa Country Instability Risk Index’ report by SBM Intelligence, released in November 2024. The report revealed that Botswana, Seychelles, Nigeria, Namibia and Zimbabwe were the lowest, with Nigeria’s rank falling following the exit of foreign businesses due to the conditions mentioned above.

Nigeria spent $3.58billion to service external debt for the first nine months of 2024 despite a series of reforms implemented by the Government that were supposed to raise revenue and control borrowings. The surge in the debt servicing represents a 39.77% increase from $2.56billion spent during the same period in 2023, according to data from the Central Bank of Nigeria (CBN) on International Payment Statistics. It also revealed that the highest monthly debt servicing payment in 2024 occurred in May, amounting to $854.37million.

The Chairman of the Presidential Committee on Fiscal Policy and Tax Reforms, Mr. Taiwo Oyedele, has stated that the Finance Act will become cancelled once the Tax Reform Bills are passed into law by the Legislative and Executive arms of Government. Earlier, the Nigerian Government had introduced four significant tax reform bills aimed at overhauling the tax system. These bills are currently under consideration by the National Assembly and include the Nigeria Tax Bill 2024, Nigeria Tax Administration Bill, Nigeria Revenue Service Establishment Bill and Joint Revenue Board Establishment Bill.

We await the disbursement of FAAC allocations as well as Nigeria’s Gross Domestic Product by Output Report for Q3 2024.

DOMESTIC MARKETS

The Senate on Thursday at plenary, approved the new external borrowing plan request of $2.20billion presented for consideration by President Bola Tinubu. The approval followed the adoption of the report of the Senate Committee on Local and Foreign Debts.

MONEY MARKET AND FIXED INCOME

System liquidity opened positive for the week; however, debits due to the FGN bond and NTB auctions, along with the settlement of the CBN’s FX intervention, reduced liquidity in the system, resulting in a deficit of -₦321.54billion at the end of the week. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) increased by 6.10% and 5.93% to 32.19% and 32.81%, respectively.

The Nigerian Treasury Bills (NT-Bills) market average yield decreased by 11bps to 24.24% against 24.35% the previous week. In the Bonds market, the average yield for the Short-tenor Bonds decreased by 2bps to 19.83%, the average yield for the Medium-tenor Bonds increased by 9bps to close at 19.73% while the average yield for the Long-tenor Bonds remained unchanged at 17.88% on a week-on-week basis.

The Federal Government raised ₦346.16billion at its Bond auction and ₦695.05billion at its Treasury Bills Auctions held this week.

We expect the interbank rates to trend lower next week, as we await the inflow of FAAC credits.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 0.11% to close at ₦59.29trillion from ₦59.22trillion and 97,829.02 from 97,722.28 the previous week.

On a sectoral basis, the Insurance, Consumer Goods and Oil and Gas indices closed higher at 1.10%, 0.46% and 0.33%, while the Banking and Industrial Goods indices closed lower at -1.14% and -0.46%, respectively.

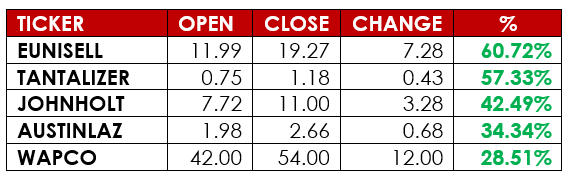

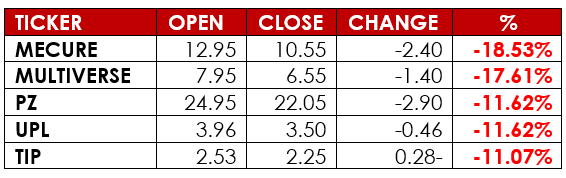

Notable gainers this week were Eunisell Interlinked Plc and Tantalizer Plc, while notable losers were Mecure Industries Plc and Multiverse Mining and Exploration Plc.

We expect the mixed sentiments to persist in the Equities market next week.

CURRENCY

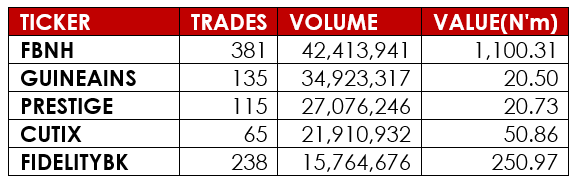

TOP TRADES BY VOLUME

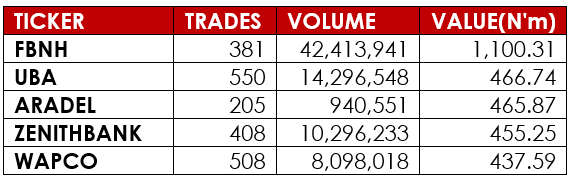

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.