GLOBAL ECONOMY

Donald Trump announced plans to impose a 50% import tariff on goods from the European Union from June 1st, 2025, citing stalled trade negotiations as the reason for this decision. The US initial jobless claims fell by 2,000 to 227,000, below expectations of 230,000, signaling continued labor market strength. Fed Chair Jerome Powell reaffirmed the Fed’s commitment to its 2.00% inflation target as US Manufacturing Purchasing Managers Index (PMI) rose to 52.30 in May 2025 compared to 50.20 in April 2025. This is the highest in three months, signaling the strongest improvement in business conditions since June 2022 as growth was driven by a rebound in production.

The UK annual inflation rose to 3.50% in April 2025, up from 2.60% in March and above expectations of 3.30%, with core inflation rate rising to 3.80% in April from 3.40% in the previous month, also exceeding market expectation of 3.60%. The largest upward contribution came from prices for housing and utilities (7.80% vs 1.80%), mostly electricity (4.60% vs -8.80%) and gas (12.20% vs -12%). UK public sector net borrowing (excluding banks) rose to £20.20billion, exceeding expectations and marking one of the highest April borrowings on record. Increased spending on public services and benefits drove the rise, partially offset by lower debt interest costs.

The Euro traded around €1/$1.13, following Trump’s announcement of the 50% tariff on all EU goods to kick off in June. Inflation in the Euro Area was confirmed at 2.20% in April 2025, slightly above the European Central Bank’s 2.00% target with core Inflation climbing to 2.70%, up from 2.50% in March. Wage growth in the Euro Area slowed sharply to 2.38% year-on-year in Q1 2025, down from 4.12% in the previous quarter. The Eurozone Manufacturing PMI rose to 49.40 in May 2025 from 49.00 in April, slightly above market expectations of 49.30. This reinforces the European Central Bank’s view that wage-driven inflation pressures are easing, strengthening expectations of further interest rate cuts next month.

China’s fiscal revenue fell 0.40% year-on-year to ¥8.06trillion in the first four months of 2025, improving from a 1.10% decline in Q1 2025. Tax revenue shrank 2.10%, while non-tax revenue grew 7.70%, showing a shift in revenue composition. China’s Central Bank cut key lending rates as the one-year loan prime rate (LPR), a benchmark for corporate and household loans, dropped by 10bps to 3.00%, while the five-year LPR, which influences mortgage rates, fell to 3.50% marking the first reduction since October 2024.

Next week, Investors will brace themselves for a turbulent week as they monitor the renewed tariff threats by President Trump on EU as well as minutes on the FOMC meeting.

GLOBAL MARKETS

US stocks closed the week on a negative note, amid escalating trade tensions with President Trump’s proposition of a 50% tariff on imports from the European Union. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices decreased by -2.14%, -2.61% and -2.47% to close at 18,737.21, 5,802.82 and 41,603.07, respectively.

In the UK and across Europe, major stocks reversed early gains following the intensification of Trump’s announcement and new tariffs on Apple’s foreign-made iPhone. The London’s Financial Times Stock Exchange (FTSE) 100, closed almost flat increasing by 0.38% to 8,717.97 while France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices decreased by -1.93% and -0.58% to 7,734.4, and 23,629.58.

The Chinese stocks closed mixed with selling pressure persisting despite positive developments on the Sino-US trade front. The Hang Seng index increased by 1.10% to 23,601.26 while the Topix index decreased by -0.18% to 2,735.52.

We expect the bearish sentiments to persist as Investors closely monitor the market and the impact of the new tariffs on the market.

DOMESTIC ECONOMY

CBN Maintains Key Interest Rates Amid Inflation Moderation

The 300th Monetary Policy Committee (MPC) meeting of the Central Bank of Nigeria (CBN), held on 19th & 20th May 2025, with the MPC reaffirming its commitment to stabilizing the economy amid ongoing inflationary pressures and structural reforms. The Committee unanimously decided to retain the Monetary Policy Rate (MPR) at 27.50%, alongside a Cash Reserve Ratio (CRR) of 50% for commercial banks and 16% for merchant banks, and a Liquidity Ratio of 30% while the asymmetric corridor was also maintained at +500/-100 basis points. With all twelve members present, the Committee conducted a comprehensive review of global and domestic economic trends, assessing potential risks to the outlook before reaching its decision which was also impacted by recent data from the National Bureau of Statistics (NBS), indicating a decline in headline inflation to 23.71% in April, a 52bps drop from 24.23% in March.

Nigeria’s External Debt Servicing Rises to $2.01billion, Consuming 77% of FX Outflow

Nigeria spent $2.01billion on external debt servicing between January and April 2025, a 50% increase from the same period in 2024. Debt service now accounts for 77.10% of total foreign payments, up from 64.50% last year, according to CBN data. Total international payments for the first four months of 2025 stood at $2.60billion, with FX reserves depleting by $3billion due to mounting obligations. Debt servicing saw sharp spikes in March and April, totaling $1.20billion, as repayments intensified, raising concerns over Nigeria’s external debt burden and foreign exchange stability.

CBN Reports Sharp Decline in Currency Volatility as FX Market Stabilizes

Governor Olayemi Cardoso announced that Foreign Exchange (FX) volatility in Nigeria has dropped below 0.50%, a major improvement from over 4% a year ago. He attributed this progress to monetary and fiscal reforms, including exchange rate unification, market-based FX supply measures, and transparency initiatives. He emphasized that restored investor confidence and improved foreign reserves are reinforcing stability in the macroeconomic environment. The sharp decline in volatility suggests that CBN’s policy consistency and tightening measures are beginning to yield significant results.

We await the release of the Q1 2025 GDP growth figures from the Central Bank of Nigeria (CBN), to provide insight into the pace of economic recovery and inform policy making.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System Liquidity stayed stable during the week despite midweek tightening due to the CBN’s OMO auction which was oversubscribed on Tuesday. Consequently, short-term rates remained stable, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) decreased slightly by 8bps and 4bps to close at 26.42% and 26.92%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 14bps to 20.79% last week. In the Bonds market, the average yield for the Short-tenor, Mid-tenor and Long-tenor Bonds decreased by 4bps, 1bp and 148bps to 19.21%, 19.13% and 17.77% respectively.

The Nigerian Treasury Bills Auction held on Wednesday 21st May 2025. The auction witnessed strong demand, as the total subscription was 2.34x the total offer, at ₦1.17trillion. The bid-to-cover ratio was 1.90x and total allotment was ₦615.80billion. Stop rates remained unchanged for the 91-day and 182-day bills and decreased by 7bps for the 364-day bill.

Next week Investors would turn their attention to the Bonds market where the DMO is reopening bids for the FGN 2029 and FGN 2033 Bonds on Monday 26th May 2025.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization depreciated by 0.62% and 0.29% to close the week at 109,028.62 and ₦68.75trillion from 109,710.37 and ₦68.95trillion last week.

A total turnover of 3.93 billion shares worth ₦74.81billion in 105,220 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 2.61 billion shares valued at ₦63.79billion that exchanged hands last week in 77,593 deals. On a sectoral basis, the Banking, Oil and Gas indices closed negative at -1.52% and -3.44%, while Insurance, Consumer Goods and Industrial Goods indices all closed positive at 0.73%, 2.18% and 0.72%, respectively.

Notable gainers this week were Cutix Plc and Custodian Investment Plc while notable losers were Neimeth International Pharmaceuticals Plc and Associated Bus Company Plc.

We anticipate a rebound in the market after selloffs and profit taking last week

CURRENCY

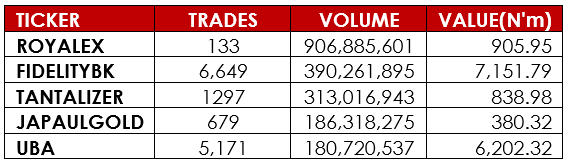

TOP TRADES BY VOLUME

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.