GLOBAL ECONOMY

Initial jobless claims in the US rose by 6,000 to 223,000, slightly ahead of market expectations of 220,000, the highest rise in six weeks. The outstanding claims rose by 46,000 to 1,899,000, suggesting that those without jobs find it hard to acquire suitable employment, and pointing to a greater impact of restrictive interest rates by the Federal Reserve (Fed) on the US labor market. The four-week moving average for initial claims, which reduce weekly volatility, also rose by 750 to 213,500.

The United Kingdom’s unemployment rate rose to 4.40% from September to November 2024, compared to 4.30% in the previous two periods. This was driven by an increase in individuals unemployed for up to 12 months. Meanwhile, the number of employed individuals rose by 35,000 to 33.78 million, with year-on-year growth in full-time employees and self-employed workers.

The Euro climbed toward €1/$1.05, its highest level in over a month, supported by a weaker dollar after President Trump appeared to soften his stance on tariffs and advocated for an immediate drop in interest rates. Meanwhile, the European Central Bank (ECB) is expected to implement another 25bps cut to the key deposit rate next week, following four reductions in 2024.

The People’s Bank of China (PBoC) kept its key lending rates unchanged for the third consecutive month in its January meeting, aligning with market expectations. The one-year loan prime rate (LPR), a benchmark for most corporate and household loans, was maintained at 3.10%, while the five-year LPR, which serves as a reference for property mortgages, was retained at 3.60%.

The Fed is expected to take a neutral stance regarding the US interest rate at its next meeting, while the ECB is anticipated to deliver another 25bps cut in borrowing costs.

GLOBAL MARKETS

US markets closed higher after a week of gains to digest mixed corporate earnings and policy signals from President Trump, supported by relief over President Trump’s unexpectedly softer trade measures after his first day in office. The Nasdaq index, S&P 500 and Dow Jones indices increased by 1.55%, 1.74% and 2.15% to 21,774.01, 6,101.24 and 44,424.25, respectively.

The consumer confidence in the British economy fell amid recession fears. In Europe, traders were reassured by news that the incoming Trump’s administration would hold off on imposing trade tariffs for now. The London’s Financial Times Stock Exchange (FTSE) 100 closed almost flat, decreasing by -0.03% to 8,502.35, while the France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices closed positive this week, increasing by 2.83% and 2.35% to 7,927.62 and 21,394.93, respectively.

Chinese stocks finished the week higher, building on gains from the previous week as Beijing revealed new measures to encourage stock market investment. The People’s Bank of China (PBoC) injected CNY 200 billion into financial institutions through a one-year medium-term lending facility (MLF) on January 24th at a rate of 2.00%. The Hang Seng and Topix indices increased by 2.46% and 2.71% to 20,066.19 and 2,751.04, respectively.

We anticipate cautious trading as traders keep a close eye on President Trump’s policy announcements, key Central Bank decisions, and corporate earnings releases.

DOMESTIC ECONOMY

Nigeria’s total public debt rose to ₦142.32trillion as of September 30, 2024, representing an increase of 5.97% (₦8.02trillion) compared to ₦134.30trillion in June 2024, according to the data released by the Debt Management Office (DMO) on Tuesday. This is a result of the combined effects of rising domestic borrowing and the impact of exchange rate depreciation on external debt when converted to naira terms. In Dollar terms, Nigeria’s external debt grew by 0.29%, from $42.90billion in June to $43.03billion in September. The issuance of bonds in naira terms accounted for most of this growth. Also, Nigeria introduced its first domestic dollar-denominated bond, adding ₦1.47trillion to the debt stock.

Manufacturing companies across all sub-sectors of the Manufacturing sector recorded ₦1.40trillion worth of unsold inventories in 2024. The President of the Manufacturers Association of Nigeria (MAN), Mr. Francis Meshioye, attributed the loss to the high inflation rate and a reduction in the purchasing power of Nigerians. He also noted that the sector struggled last year and its contribution to the GDP was severely impacted by numerous challenges, including high energy costs, high inflation rate, high exchange rate, and multiplicity of taxes.

Nigeria’s total debt service costs climbed to ₦3.57trillion in Q3, 2024, up by ₦60billion from ₦3.51trillion in Q2, 2024, in a document released by the DMO. This increase reflects a combination of higher external debt service obligations and the impact of naira depreciation. The rise was primarily driven by obligations to multilateral and bilateral creditors, alongside significant interest payments on commercial loans.

We await the release of the Foreign Reserves report for December 2024 by the National Bureau of Statistics (NBS).

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity improved at the start of the week, boosted by inflows from FGN Bond coupons, net Cash Reserve Ratio (CRR) credits, FAAC payments and Remita Inflows. However, it closed negative at the end of the week, albeit better than last week, due to debits from the NTB auction settlements. The Open Repo Rate (ORR) and Overnight Rate (O/N) fell by 533bps and 525bps to 27.00% and 27.50%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 22bps to 25.01% against 25.23% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor and Long-tenor Bonds decreased by 91bps to 21.21% and increased by 6bps and 66bps to 20.76% and 18.74% respectively.

The Treasury Bills Auction was held on Wednesday, 22nd January 2024, where the Government offered ₦530billon across tenors. The stop rates closed at 18.00%, 18.50% and 21.80% for the 91-day, 182-day and 364-day bills respectively. Total subscription was ₦2.54trillion and total allotment was ₦756.01billion. The Federal Government Bond Auction is scheduled to hold next week on Monday 27th January 2025, with an offer size of ₦450billion across tenors.

We expect cautious trading activity as participants prepare for the Bond Auction next week, where the 2029 and 2031 Bonds would be re-issued, and a new 2035 Bond will be issued.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 1.26% and 1.22% to close at ₦63.65trillion from ₦62.85trillion and 103,598.30 from 102,353.68 the previous week.

A total turnover of 3.13 billion shares worth ₦76.55billion in 61,456 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 2.25 billion shares valued at ₦58.83billion that exchanged hands last week in 63,657 deals. On a sectoral basis, the Banking and Industrial Goods closed positive this week, at 4.09% and 0.12%, while the Insurance, Oil and Gas and Consumer Goods indices closed negative at -1.20%, -0.93% and -1.20%, respectively.

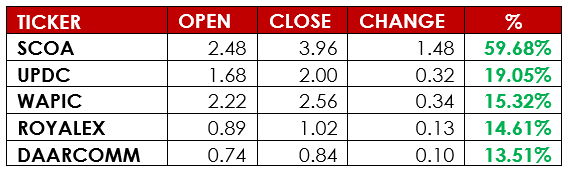

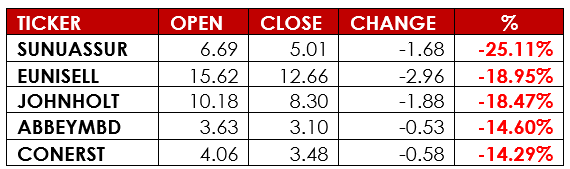

Notable gainers this week were SCOA Nig. Plc and UPDC Plc, while notable losers were Sunu Assurances Nigeria Plc and Eunisell Interlinked Plc.

RIGHTS ISSUE

Stanbic IBTC Holdings PLC announced a rights issue to raise additional equity capital of up to ₦150 billion. The shares on issue are 2,944,772,083 ordinary shares of 50 kobo each with an Issue Price of ₦50.50 per share. The Basis of Issue is 5 new Ordinary Shares for every 22 Ordinary Shares, with a qualification date of 29th October, 2024.

The Right Issue opened on 15th January 2025 and will close on 21st February 2025. Investors who do not wish to exercise their Rights to this issue can trade the Rights in part or in full, on the NGX between Wednesday, 15 January 2025 and Friday, 21 February 2025 at the quoted price.

We expect reduced activities in the equities market as Investors shift their attention to the upcoming FGN Bonds Auction.

CURRENCY

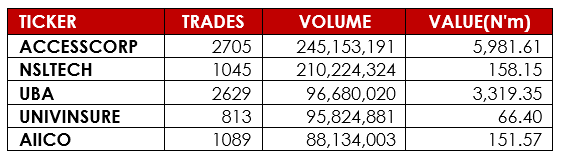

TOP TRADES BY VOLUME

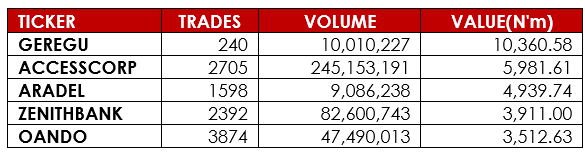

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research