GLOBAL ECONOMY

The US Dollar index rose this week, after President Trump reaffirmed that trade negotiations with China are ongoing despite denials from Beijing. Initial jobless claims in the United States rose by 6,000 from the previous week to 222,000 on the third week of April, in line with market expectations. Outstanding jobless claims fell by 37,000 to 1,841,000.

UK public sector net borrowing rose to £16.40billion in March 2025, exceeding 2024’s figure of £20.70billion and the Office for Budget Responsibility’s (OBR) forecast of £14.60billion. This marks the third-highest borrowing on record as Annual borrowing reached £151.90billion, driven by higher spending on public services, benefits, and debt interest. Net debt was estimated at 95.84% of GDP.

The Eurozone recorded a €24billion trade surplus in February 2025, driven by a 6.20% rise in exports to €249billion, and a 5.71% increase in imports to €225billion, year-on-year. This was due to notable export growth in chemicals (+36%) to Switzerland (+34.83%), and the U.S (+22.45%). Imports rose 7.25%, mainly from South Korea (+21%), China (+13.30%), and Switzerland (+12.50%).

The offshore Yuan steadied at ¥7.28/$1 as investors considered remarks from People Bank of China (PBoC) Governor Pan Gongsheng on maintaining loose monetary policy and reducing global tariff impacts. US-China trade negotiations remain uncertain, with conflicting statements from both sides. However, China is reportedly exploring exemptions for some US imports from its 125% tariffs, fueling hopes of eased trade tensions. The PBoC injected ¥600billion into financial institutions via the medium-term lending facility (MLF) on April 25th, 2025, resulting in a net liquidity boost of ¥500billion.

Next week, Investors will closely monitor developments in the ongoing US-China trade dispute, assessing the likelihood of a potential de-escalation.

GLOBAL MARKETS

US stocks closed positive last week, fueled by strength in Tech Stocks, while President Trump’s latest tariff remarks kept trade tensions in the spotlight. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices increased by 6.73%, 4.59% and 2.48% to 17,382.94, 5,525.21 and 40,113.50, respectively.

In the UK and across Europe, sentiments improved slightly as European stocks closed higher due to optimism around easing US-China trade tensions, strong corporate earnings, and positive market sentiment boosting Investor confidence, driving gains across the region. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices increased by 1.69%, 3.44% and 4.89% to 8,415.25, 7,536.26 and 22,242.45, respectively.

Chinese stock benchmarks closed the week higher, driven by optimism over a potential easing in US-China trade tensions. This followed US President Trump’s remarks asserting that trade negotiations with China are ongoing, despite Beijing’s claims to the contrary. The Hang Seng index and Topix index increased by 2.74% and 3.87% to 21,980.74 and 2,628.03, respectively.

We expect the Quarterly earnings reports from major companies such as Microsoft, Apple and Amazon to influence Investors action next week.

DOMESTIC ECONOMY

Nigeria records $15.20billion net FX inflow in Q1 2025

Nigeria recorded a net Foreign Exchange (FX) inflow of $15.20billion in Q1, 2025, reflecting a stronger FX position driven by sustained market reforms and rising investor and diaspora confidence. In January 2025, FX inflows stood at $9.41billion, with outflows at $4.84billion, resulting in a net inflow of $4.56billion. February had the strongest performance, with inflows of $10.64billion and lower outflows of $3.72billion, a net inflow of $6.92billion. In March however, inflows fell to $8.88billion, while outflows increased to $5.16billion, a net inflow of $3.72billion.

Currency in circulation drops to ₦5trillion in March 2025

Nigeria’s currency in circulation declined to ₦5trillion in March 2025, according to the latest data from the Central Bank of Nigeria (CBN), reflecting a continued drop for the third consecutive month in 2025. The report showed that currency in circulation (CIC) fell by 0.79% month-on-month from ₦5.04trillion in February 2025 from ₦5.24trillion recorded in January 2025. Currency in circulation refers to the total amount of cash – coins and paper currency – that has been issued by CBN and is physically used for transactions by the public and businesses outside of the banking system. A drop in CIC may indicate increased cash mop-up by banks, a shift to digital transactions, or broader macroeconomic tightening.

Money supply rises to ₦114.22trillion in March amid rising inflation

Nigeria’s broad money supply (M3) rose to ₦114.22trillion in March 2025, up by 24% from ₦92.19trillion in the same month of 2024, according to the CBN. The surge in money supply comes amid rising inflation currently at 24.23%. On a month-on-month basis, M3 rose by 3.17% from ₦110.71trillion in February. This was largely driven by a sharp increase in net foreign assets (NFA), by 38.90% to ₦45.17trillion, signaling stronger capital inflows and improved external liquidity.

IMF Warns Nigeria of Economic Risks Amid Global Uncertainties

The IMF has warned Nigeria about potential declines in commodity export earnings due to global trade tensions and tightening financial conditions. Despite steady GDP growth, Nigeria remains vulnerable to external risks due to its reliance on oil and gas exports. The IMF projects a significant narrowing of the current account surplus and elevated inflation rates in the coming years, as they project the inflation rate to average 26.50% in 2025 and rise further to 37% in 2026.

We expect CBN to carry out OMO auctions and FX sales next week to sustain its market stabilization efforts.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity opened the week positive with a surplus of ₦262.61billion. It remained positive despite the significant outflow ₦714.38billion for the Treasury Bills auction settlement and improved significantly to ₦1.79trillion, driven by inflows from FAAC, FX swaps, and bond coupons. The Open Repo Rate (ORR) remained unchanged at 26.50%, while the Overnight Rate (O/N) increased by 3bps to 26.88%.

The Nigerian Treasury Bills (NTB) market average yield decreased by 29bps to 19.42% against 19.71% last week. In the Bonds market, the average yield for the Short-tenor bonds, increased by 1bp to 19.06% while the Medium-tenor bonds decreased by 2bps to 19.22% and the average yield for the Long-tenor Bonds remained unchanged at 17.81%.

The Treasury Bills auction held this week, with an offer of ₦400billion and a total subscription of ₦1.54trillion. The bid-to-cover ratio was 2.15x and total allotment was ₦714.38billion, higher than the initial offer, thus, the auction was oversold by ₦314.38billion. Stop rates decreased by 50bps, 100bps and 3bps to 18.00%, 18.50% and 19.60%, for the 91-day, 182-day and 364-day bills, respectively.

We anticipate cautious trading in the Fixed Income space as Investors await the Debt Management Office (DMO) Bond Auction with an offer of ₦350billion for two tenors: 19.30% APR 2029 and 19.89% MAY 2033 papers.

THE EQUITIES MARKET

The market opened for four trading days this week as the Federal Government of Nigeria declared Friday 18th April and Monday 21st April 2025 as Public Holidays to commemorate 2025 Easter celebration.

The NGX All-Share Index and Market Capitalization increased by 1.46% and 1.47%to close the week at 105,752.61 points and N66.47trillion, from the previous week figure of 104,233.81points and ₦65.50trillion, respectively.

A total turnover of 1.85 billion shares worth ₦56.03billion in 51,386 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 1.53 billion shares valued at ₦43.01billion that exchanged hands last week in 51,156 deals. On a sectoral basis, the Banking, Insurance and Consumer Goods indices closed positive, at 5.06%, 7.30% and 8.65%, while the Oil and Gas and Industrial Goods indices both closed negative at -0.70% and -3.44%, respectively.

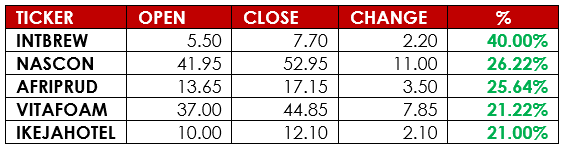

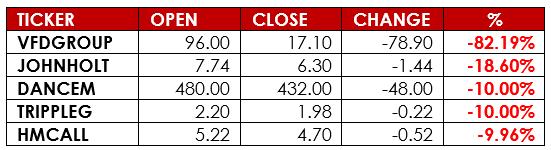

Notable gainers this week were International Breweries Plc and Nascon Allied Industries Plc, while notable losers were VFD Group Plc and John Holt Plc.

We expect Investors sentiment to be shaped by the Q1 earnings being released, amidst profit-taking.

CURRENCY

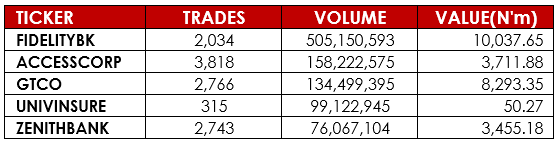

TOP TRADES BY VOLUME

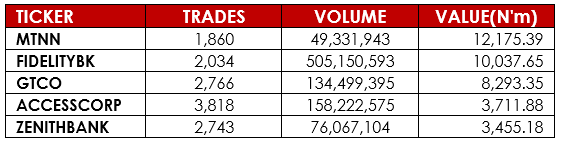

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, BusinessDay, Alpha10 Research