GLOBAL ECONOMY

US President Trump announced tariff rates between 15%-50%, targeting countries without finalized trade deals, while Commerce Secretary Lutnick expressed confidence in reaching an agreement with the EU. Treasury Secretary Bessent emphasized prioritizing American interests in negotiations with Japan and China, with talks in Stockholm aiming to extend the August 12 US-China trade deadline. Manufacturing PMI fell to 49.50, reflecting weakened factory activity and new orders on the back of slowed global economic growth. However, the service sector showed modest improvement, and initial jobless claims dropped to 217,000, the lowest since April, signalling labor market resilience.

The Pound weakened to £1/$1.35 as markets were swayed by a likely Bank of England rate cut in August, shifting focus from inflation to growth concerns. UK public sector net borrowing surged to £20.70billion in June 2025, its highest since April 2021, driven by an £8.40billion spike in debt interest payments amid high inflation, pushing total borrowing for the fiscal year to £57.80billion as Public Debt reached 96.30% of GDP. Car production which is a major component of the UK manufacturing sector dropped by 6.50% year-on-year, with exports down 18.70%, though a new UK-US trade deal offers hope for recovery.

The Euro traded near €1/$1.18, buoyed by the European Central Bank’s (ECB’s) cautious stance and a strong currency. Inflation hit the ECB’s 2.00% target in June, prompting the Central Bank to pause its easing cycle after eight rate cuts, holding the main refinancing rate at 2.15%. Meanwhile the Eurozone Composite PMI climbed to 51, signaling the strongest private sector expansion in nearly a year. Services led the growth (PMI: 51.20), with manufacturing contraction easing to 49.80 due to improved domestic demand. However, business confidence dipped amid ongoing US-EU trade tensions, with potential tariffs of up to 30% looming.

The Yuan weakened to ¥7.15/$1 ahead of high-stakes at the US-China trade talks, following tensions and growing scrutiny of Chinese tech firms in the US, particularly TikTok. China held its key lending rates steady in July at 3.00% for the one-year Loan Prime Rate (LPR) and 3.50% for the five-year Loan Prime Rate (LPR), amid slowing growth, persistent deflationary pressures, and ongoing property sector weakness. Q2 GDP grew by 5.20%, slightly above expectations, while H1 growth reached 5.30%. China’s rare earth magnet exports to the US surged 660% in June primarily driven by the easing of trade restrictions following a new US-China trade agreement, though H1 exports were still down 18.90% year-on-year. The job market remained stable, with 6.95 million urban jobs created in H1 and unemployment holding at 5.00%.

Investors globally will focus on US trade negotiations and the release of the minutes of the FOMC meeting.

GLOBAL MARKETS

This week, US stocks closed high as Investors digested trade developments and corporate earnings with optimism around trade talks. Compared to last week, the Dow Jones, S&P 500 and Nasdaq indices increased by 1.26%, 1.46% and 1.02% to close at 44901.92, 6,388.64 and 21,108.32 respectively.

In the UK and across Europe, major stocks dropped to trim initial gains during the week as Investors digested several corporate earnings. London’s Financial Times Stock Exchange (FTSE) 100 and France Cotation Assistéeen Continu (CAC) 40 indices increased by 1.46% and 0.15% to 9,123.25 and 7,834.58, while Germany’s Deutscher Aktien (DAX) decreased by -0.35% to 24,204.02.

The Asian stock market closed high last week with major stocks closing positive as Investors sentiment albeit cautious, was positive over the renewed US-China trade talks. The Hang Seng and Topix indices increased by 2.27% and 4.14% to 25,388.35 and 2,951.86 respectively.

Next week, Investors will closely watch developments on the US-EU trade front while also on the lookout for US Q2 GDP, PCE Inflation report and other economic data to further guide sentiments.

DOMESTIC ECONOMY

Nigeria’s Economy Grows 3.13% in Q1 2025 Driven by Services and Industry Sectors

Nigeria’s Gross Domestic Product (GDP) expanded by 3.13% year-on-year in real terms in Q1 2025, up from 2.27% in Q1 2024, reflecting economic resilience post-rebasing to 2019 prices. Nominal GDP rose 18.30% to ₦94.05trillion as the services sector led growth with a 4.33% increase, contributing 57.50%, bolstered by Telecoms (7.40%) and Finance (15.03%). Manufacturing Industry grew 3.42%, though the Oil sector slowed to 1.87% growth despite higher output while construction surged 6.21%. Agriculture remained sluggish at 0.07% growth, hindered by insecurity and low mechanization. Notable gains were seen in electricity sector (18.65%), water services (9.43%), and entertainment (9.63%).

FAAC Disburses ₦1.82trillion in June 2025, Up 9.60% from May

The Federation Account Allocation Committee (FAAC) shared ₦1.82trillion among Nigeria’s Federal, State, and Local Governments for June 2025, a 9.60% increase from May’s ₦1.66trillion. The revenue comprised ₦1.02trillion in statutory revenue, ₦631.50billion from VAT, ₦29.20billion from Electronic Money Transfer Levy, ₦38.80billion from Exchange Gains, and ₦100billion from Non-Mineral Revenue. The Federal Government received ₦645.40billion, States ₦607.40billion, and LGAs ₦444.90billion, while oil-producing states got ₦120.80billion as 13% derivation. The rise was driven by strong collections from Companies Income Tax and Petroleum Profit Tax, despite a drop in VAT and trade-related revenues.

CBN Holds Rates, Confirms 8 Banks Meet Capital Requirements Amid Investor Optimism

At the July 22, 2025 MPC meeting, the Central Bank of Nigeria (CBN) held the Monetary Policy Rate (MPR) at 27.50%, with CRR at 50% for commercial banks and 16% for merchant banks, as the CBN aims to sustain disinflation and stabilize the naira. Cardoso highlighted growing Foreign Investor interest, calling Nigeria’s banking system “fit for purpose” and increasingly attractive to global capital. CBN also confirmed that eight banks have met minimum capital requirements under its temporary forbearance regime, with GTCO notably raising significant capital via the London Stock Exchange. CBN Governor Yemi Cardoso emphasized the sector’s resilience, citing a Capital Adequacy Ratio of 13%, a liquidity ratio of 50%, and Non-Performing Loans within the 5% threshold.

This week, Investors will focus on the release of July’s Purchasing Managers Index data for key insight into economic momentum and direction.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity closed positive this week at ₦1.35trillion due to inflows from FAAC allocations and net NTB maturities. Consequently, the Short-term rates closed lower, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) decreased by 583bps and 575bps to 26.50% and 26.92% respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased further week-on-week by 3bps to 16.20%. In the Bonds market, the average yield for the short-tenor bond remained unchanged at 16.78%, while the mid-tenor and long-tenor bonds decreased by 43bps and 7bps to 16.18% and 15.83% respectively.

This week Investors focus will shift to the FGN Bond Auction happening on 28thJuly 2025, where the DMO is offering ₦20billion on the FGN April 2029 (5yr re-opening) and ₦60billion on the FGN June 2032 (7yr re-opening).

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 2.18% to close the week at 134,452.93 and ₦85.06trillion compared to 131,585.66 and ₦83.24trillion last week.

A total turnover of 3.69 billion shares worth ₦112.26billion in 138,250 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 17.50 billion shares valued at ₦500.76billion that exchanged hands last week in 142,082 deals.

On a sectoral basis, the Banking, Insurance, Consumer Goods, Industrial Goods and Oil and Gas indices all closed positive at 1.84%, 3.07%, 2.81%, 4.66% and 0.87%

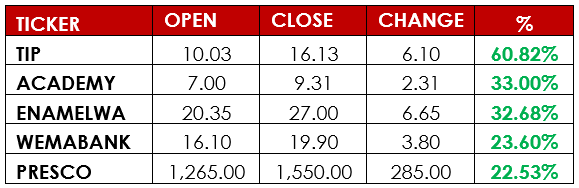

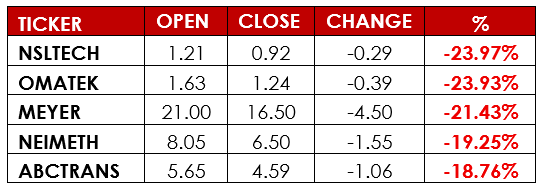

Notable gainers this week were The Initiates PLC and Academy Press PLC, while notable losers were Secure Electronic Technology PLC and Omatek Ventures PLC.

This week, we anticipate the bullishness to continue on the back of strong corporate earnings and improved sentiments from Investors.

CURRENCY

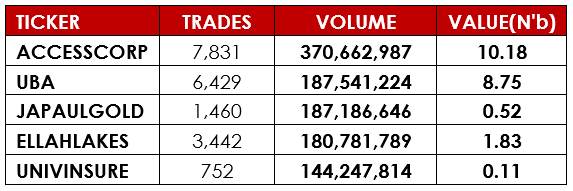

TOP TRADES BY VOLUME

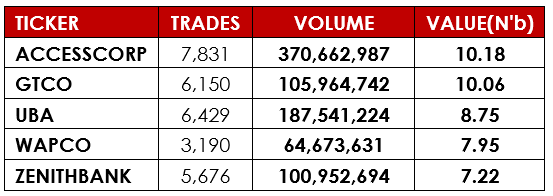

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst utmost care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.