GLOBAL ECONOMY

The U.S economy contracted by 0.50% year-on-year, driven by weak consumer spending and slow export growth due to tariff uncertainties. The current account deficit ballooned to $450.20billion, while the US reached a framework deal with China to resume rare earth shipments. Personal income dropped 0.40% in May with consumer spending declining by 0.10% in May, pulled down by a 1.80% plunge in durable goods, while real disposable income fell 0.70%, tightening household conditions. Initial jobless claims dropped to 236,000, while continuing claims hit 1.97 million. Manufacturing and services activity also remained expansionary, with Composite Purchasing Managers Index (PMI) at 52.80.

The British Pound closed at £1/$1.37, supported by the Bank of England’s caution on rate cuts and persistent core inflation. The UK economy showed tentative signs of recovery, with the Composite PMI rising to 50.70 from 50.30 in May as services expanded (51.30) and manufacturing contraction eased (47.70). Export demand weakened further, largely due to U.S. tariffs and geopolitical uncertainty.

The Euro appreciated past €1/$1.17, buoyed by a weaker Dollar and easing geopolitical tensions. Composite PMI held at 50.20, signaling minimal growth. Services activity stabilized at 50.00, while Manufacturing remained in contraction at 49.40, despite output rising for the fourth month.

The Yuan weakened to ¥7.16/$1, pressured by vague details in a new US-China rare earths deal and disappointing industrial data. The Q1 2025 current account surplus hit a record $165.40billion, driven by a goods trade surplus of $237.50billion amidst weak domestic demand and rising exports. The People’s Bank of China injected ¥300billion via its Medium-Term Lending Facility, resulting in a net liquidity boost of ¥118billion, marking the fourth straight month of easing. On the legislative front, China’s top legislature passed a revised Anti-Unfair Competition Law, effective October 15, 2025, introducing a fair competition review system and stricter rules on platform operators and data rights aiming to curb monopolistic behaviours of large platform companies, aligning China’s market practices with global standards.

Next week, Investors focus on the trade front where China and US agreed on a favourable trade deal on rare earths and other export restrictions.

GLOBAL MARKETS

Last week, U.S stocks closed high last week as there was optimism over pending trade agreements which improved sentiments and raised expectations. Compared to last week, the Dow Jones, Nasdaq and S&P indices increased by 3.82%, 4.25% and 3.44% to close at 43,819.27, 20,273.46 and 6,173.13 respectively.

In the UK and across Europe, major stocks closed higher following signals that the US may likely impose softer tariffs than initially proposed. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices increased by 0.28%, 1.34% and 2.99% to 87,98.91, 7,691.55 and 24,049.82 respectively.

The Asian stock market closed positive last week with market as concrete details on the US-China trade agreement were not made public. The Hang Seng and Topix indices increased by 3.20% and 0.54% to 24,284.15 and 2,771.26 respectively.

This week, Investors will turn attention to trade negotiations and potential deals between US and partnering countries as 9th July deadline for 90-days tariff pause elapses.

DOMESTIC ECONOMY

Nigeria’s Q1 Revenue Soars 33% to ₦6.90trillion on Transparency, Tech Reforms, and Investor Confidence

Nigeria’s revenue surged to ₦6.90trillion in Q1 2025, up from ₦5.20trillion in the same period last year, a 32.70% year-on-year increase driven by improved transparency, exchange rate reforms, and automation across Ministries, Departments and Agencies (MDAs). The Finance Minister Wale Edun highlighted a sharp drop in the debt service-to-revenue ratio from 150% to 60%, with no reliance on Ways and Means. The government’s fiscal discipline and data integrity efforts have boosted investor confidence, exemplified by Shell’s $5.50billion investment. While real GDP growth is improving, the administration is targeting 7% annual growth to outpace population growth and reduce poverty.

Tinubu Signs Landmark Tax Reform Bills to Reshape Nigeria’s Fiscal Landscape

On June 26, 2025, President Bola Tinubu signed four major tax reform bills into law. the Nigeria Tax Bill, Nigeria Tax Administration Bill, Nigeria Revenue Service (NRS Establishment) Bill, and Joint Revenue Board (Establishment) Bill, marking a sweeping overhaul of Nigeria’s tax system. The reforms aim to streamline tax laws, harmonize administration across all government levels, and establish a more autonomous Nigeria Revenue Service (NRS) to replace the FIRS.

- The Nigeria Tax Bill consolidates fragmented tax laws to reduce duplication and ease compliance.

- The Tax Administration Bill creates a unified legal framework for tax operations nationwide.

- The NRS Bill expands the agency’s mandate to include non-tax revenue and enforces transparency.

- The Joint Revenue Board Bill introduces a national governance structure, a Tax Appeal Tribunal, and a Tax Ombudsman.

The laws will take effect on January 1, 2026, allowing six months for planning and stakeholder sensitization. The reforms are expected to boost revenue, improve the business climate, and attract investment, while offering relief to low-income earners and small businesses through simplified tax structures and reduced compliance burdens.

Nigeria’s Q1 2025 Balance of Payments: Trade Surplus Cushions Capital Flight

In Q1 2025, Nigeria’s Foreign Direct Investments (FDI) fell by 19% to $250million, down from $310million in Q4 2024, reflecting fragile investor confidence. The broader financial account which tracks cross-border flows of capital essentially, money moving in and out for investment purposes weakened to $7.58billion, pressured by a $10.60billion reversals in portfolio investments due to investors’ behaviour, from a $5.61billion inflow to a $5.03billion net outflow. Despite capital flight, the current account posted a $3.73billion surplus, supported by a 9.79% rise in exports to $13.91billion, including a 26.70% jump in gas exports and a 30.40% surge in non-oil/electricity exports. Imports declined to $9.75billion, widening the goods trade surplus to $4.16billion. However, the overall balance of payments swung to a $2.77billion deficit, and external reserves dropped to $37.82billion, down from $40.19billion.

Nigeria Leads West Africa in Intra-African Trade with $18.4billion Surge in 2024

Nigeria’s intra-African trade soared 127% to $18.40billion in 2024, up from $8.10billion in 2023, making it West Africa’s top trading nation within the continent, according to Afreximbank’s 2025 African Trade Report. The growth was driven by crude oil exports and a rising share of refined petroleum products, following the launch of the Dangote Refinery (650,000bpd), which began direct supplies to Cameroon and neighboring markets. Total exports hit $50.40billion, aided by exchange rate depreciation and fuel subsidy removal, while total trade volume reached ₦138trillion, a 106% year-on-year increase. Despite strong goods trade, Nigeria’s service imports remain high, straining the current account. Still, the current account posted a $5.14billion surplus in Q3 2024, signaling gradual external balance recovery.

Nigeria’s Pension Assets Hit ₦23.65trillion in April 2025, with Surge in Private Equity and Foreign Investments

Nigeria’s pension fund assets rose 1.40% month-on-month to ₦23.65trillion in April 2025, driven by strategic reallocations despite economic headwinds. FGN securities remained dominant, accounting for ₦14.65trillion (61.94%), with notable gains in Sukuk Bonds (+8.50%) and Agency Bonds (+8.75%), while Green Bonds (-8.19%) and Treasury Bills (-3.08%) declined. Corporate debt dipped 1.38%, but infrastructure bonds jumped 16.81%, and private equity surged 40.10% to ₦230.18billion, reflecting rising risk appetite. Money market instruments rose to ₦2.18trillion, with commercial papers up 10.43%. Domestic equities edged up 0.10%, while foreign equities climbed 5.20%, signaling renewed offshore interest. By fund category, Fund II led with ₦9.83trillion (41.54%), followed by Fund III at ₦6.20trillion. Fund VI (Islamic finance) and micro pensions also gained traction. Overall, PFAs are cautiously diversifying into higher-yield assets amid inflation and FX volatility.

This week, Investors would watch for the June PMI release, evolving monetary and fiscal policy signals and tax reform rollout planning.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System Liquidity closed the week positive at ₦1.58trillion from ₦1.33trillion levels on Thursday due to the additional FAAC inflows to the system. Consequently, short-term rates closed high, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) decreased by 167bps and 192bps to 26.50% and 27.00% respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 16bps to 18.30% last week. In the Bonds market, the average yield for the short-tenor, mid-tenor and long-tenor bonds decreased by 26bps, 6bps and 15bps to 18.99%, 18.63% and 17.29% respectively.

We expect a mild to bullish trend as Investors anticipate the release of the Q3 calendar for Treasury Bills and Bonds Auctions.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 1.57% and 1.92% to close the week at 119,995.76 and ₦75.96trillion, compared to 118,138.22 and ₦74.53trillion last week.

A total turnover of 3.90 billion shares worth ₦102.22billion in 114,484 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 3.57billion shares valued at ₦115.40billion that exchanged hands last week in 99,960 deals.

On a sectoral basis, the Banking, Insurance, Industrial Goods and Consumer Goods indices closed positive at 2.59%, 3.67%, 3.73% and 3.92%, while Oil and Gas index closed negative at -2.23%.

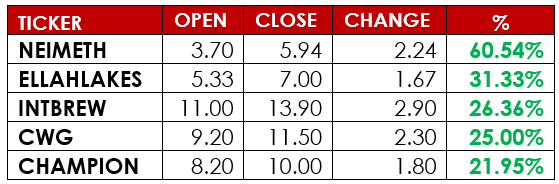

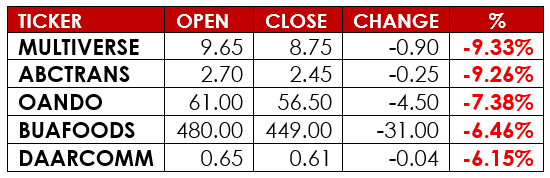

Notable gainers this week were Neimeth international Pharmaceuticals PLC and Ellah Lakes PLC, while notable losers were Multiverse Mining and Exploration and Associated Bus Company PLC.

We expect heightened activities and Investors’ sentiments to remain bullish in the Equities market this week as attention shift to earnings pre-announcements, dividend qualification dates.

CURRENCY

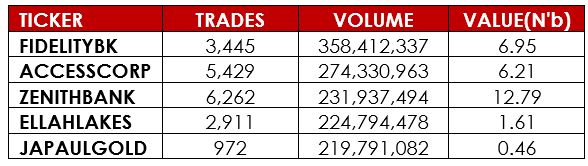

TOP TRADES BY VOLUME

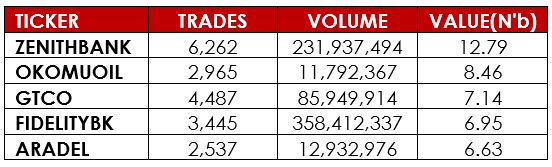

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.