GLOBAL ECONOMY

The annual inflation rate in the US slowed for a sixth consecutive month to 2.40% in September 2024, the lowest since February 2021, from 2.50% in August. The number of individuals filing for unemployment benefits in the U.S. rose by 33,000, reaching 258,000 for the week ending October 4th, surpassing market expectations of 230,000. This marks the highest level in 14 months, largely driven by substantial increases in Michigan and states affected by Hurricane Helene.

The British pound traded below £1/$1.31, the lowest level in about a month, prompted by a general dollar strength amid forecasts that the Federal Reserve will lower borrowing costs. In the UK, investors are anticipating a more aggressive stance from the Bank of England on interest rate cuts, following Governor Andrew Bailey’s suggestion at this possibility if inflation pressures continue to ease.

The Euro traded around €1/$1.09, the lowest level in about two months. The European Central Bank (ECB) is expected to lower the deposit rate by 25bps when it meets next week, following similar moves in both September and June. Traders are now betting the central bank will continue to reduce costs by a 25bps at every meeting through March.

The People’s Bank of China (PBoC) launched a ¥500billion swap facility, allowing eligible financial institutions to use assets as collateral to secure liquidity. The initiative, known as the Securities, Funds, and Insurance Companies Swap Facility (SFISF), is part of the Central Bank’s effort to develop a new structural monetary policy tool to support the stock market. This facility enables securities, fund, and insurance companies to obtain liquid assets for stock purchases by using their holdings of bonds, ETFs, and CSI 300 Index constituent stocks as guarantees.

We await the release of the US trade Position data for September and the Jobless Claims information for the week.

GLOBAL MARKETS

US stocks increased to close the week positive, fueled by strong earnings reports from major banks, setting a positive tone for Q3 earnings season. The Nasdaq, S&P 500 and Dow Jones indices all closed positive, increasing by 1.18%, 1.11% and 1.21% to 20,271.97, 5,815.03 and 42,863.86, respectively.

European stocks closed mixed this week, as traders continue to digest the inflation data for the US and await further Chinese stimulus updates over the weekend. The London’s Financial Times Stock Exchange (FTSE) 100, fell by -0.33% to close at 8,253.65 while Germany’s Deutscher Aktien (DAX) and Cotation Assistée en Continu (CAC) 40 in Paris rose by 1.32% and 0.48% to 19,373.83 and 7,577.89, respectively.

Stocks in China ended the week sharply lower as profit-taking and concerns about the effectiveness of monetary stimulus measures in boosting growth increased, as the Hang Seng fell by -6.53% to close at 21,251.98. Japan’s Topix Index rose by 0.45% to close at 2,706.20 from last week.

We expect the market to trade cautiously, as Investors digest the US Initial Jobless claims data released this week and await the release of Jobless Claims data for next week.

DOMESTIC ECONOMY

The National Bureau of Statistics (NBS) released the Capital Importation report this week, showing a significant decline in Q2, 2024. The figures show a 22.85% drop from $3.37billion in the first quarter to $2.60billion. Despite this quarter-on-quarter decrease, the current figure represents a substantial year-on-year increase of 152.8% from $1.03billion in Q2, 2023. Portfolio Investment emerged as the leading type of capital import, accounting for 53.93% of the total at $1.40billion. Other investments totaled $1.17billion, making up 44.92%.

The Federal Government has announced the commencement of zero Value Added Tax (VAT) on pharmaceutical products and medical devices in a bid to reduce drug prices in the country. The Head of Information in the Federal Ministry of Health, Alaba. R. Balogun, noted that the Executive Order on harmonized implementation framework has been cleared to be gazetted. Also, the Ministry noted that following the completion of the process, the Federal Inland Revenue Service (FIRS) and Nigeria Customs Service (NCS) can now begin implementing zero VAT and excise duties on pharmaceutical products and medical devices.

Nigeria’s debt servicing payments have increased by 69.00% in the first half of 2024, reaching ₦6.04trillion, up from ₦3.58trillion recorded in the same period of 2023. The increase in debt service obligations, likely driven by naira devaluation for foreign debt repayments, reflects the growing burden on the Federal Government as debt repayment consumes a significant portion of its financial resources. According to data from the latest statistical bulletin of the Central Bank of Nigeria (CBN), debt service in H1 2024 made up 50.00% of the total expenditure of ₦12.17trillion and 162.00% of ₦3.73 trillion total revenue generated during the period.

The Federal Government has set a target to increase oil production per day to 2.30 million per day by mid-2025. Mohammad Badaru Abubakar, the Minister of Defense stated this week. He attributed the projected increase to the military’s efforts in combating crude oil theft in the Niger Delta region and the Presidential administration’s support.

The NBS is set to release data on the Inflation rate for September on Tuesday, 15th October 2024.

DOMESTIC MARKETS

Ecobank Transnational Incorporated (ETI) issued 144a/Reg S Us$-Denominated Benchmark 5-Year (2029) Senior Unsecured Notes at a 10.125% yield, which attracted substantial Investor demand this week.

MONEY MARKET AND FIXED INCOME

System liquidity was negative this week, albeit higher than last week, closing at -₦702.83billion from -₦1.43trillion last week, due to various factors including OMO auction settlements, CBN FX intervention settlements , CBN FX Swaps among others. The Open Repo Rate (OPR) and the Overnight Rate (O/N) increased by 13bps and 23bps to close at 32.36% and 33.00%. The Nigerian Treasury Bills (NT-Bills) market average yield increased by 24bps to 23.07% against 22.83% last week.

In the Bonds market, the average benchmark yield for the Short-tenor and Medium-tenor Bonds increased by 1bps and 4bps to close at 19.07% and 19.56% while the average yield for the Long-tenor Bonds remained unchanged at 17.65% on a week-on-week basis.

At the Treasury Bill auction that held on Wednesday, 9th October, 2024, total subscription was 3.34x the total offer, at ₦273.28trillion. Bid-to-cover ratio was 3.34x and total allotment was ₦81.90billion, equal to the amount initially offered, thus, the auction was fully sold.

We expect the market to trade at the same levels next week as the CBN continues to maintain its monetary policy tightening stance.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 0.09% to close at ₦56.09trillion from ₦56.04trillion and 97,606.63 from 97,520.54 the previous week.

On a sectoral basis, the Banking, Insurance and Oil & Gas indices closed higher at 0.47%, 0.08% and 1.57%, while Consumer Goods and Industrial Goods indices closed lower at -1.25% and -0.13%, respectively.

A total turnover of 2.97 billion shares worth ₦31.51billion in 42,482 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 2.87 billion shares valued at ₦132.81billion that exchanged hands last week in 39,867 deals.

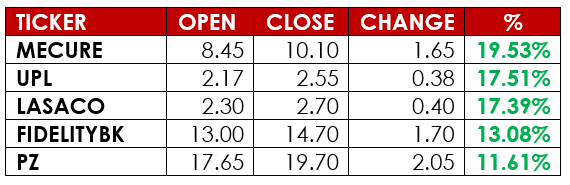

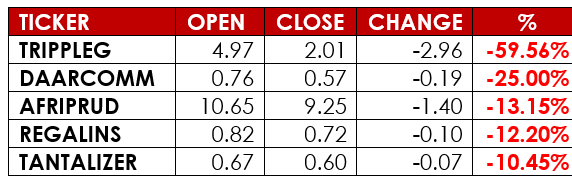

Notable gainers this week were Mecure Industries Plc and University Press Plc, while notable losers were Tripple Gee and Company Plc and Daar Communications Plc.

We expect cautious trading in the Equities market next week, with selected interest in Banking stocks ahead of Q3 earnings season.

CURRENCY

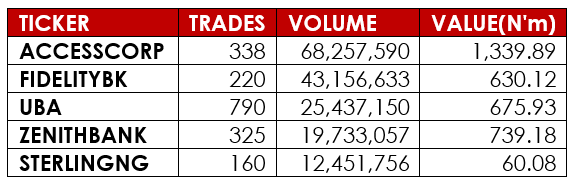

TOP TRADES BY VOLUME

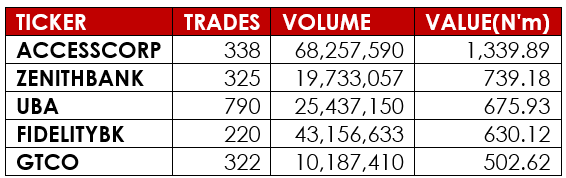

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Trading Economics, Investing.com, CBN, FMDQ, AIICO, NBS, NGX, BusinessDay, Nairametrics, Alpha10 Research.