GLOBAL ECONOMY

The US economy expanded by 2.30% in Q4 2024, down from 3.10% in Q3 2024. Personal consumption remained the main driver of growth, increasing by 4.20%. The US Personal Consumption Expenditures (PCE) price index also increased by 0.30% month-on-month in January 2025, the same as December 2024, as prices for goods increased by 0.50%, following a 0.10% rise in December. Meanwhile, the core PCE index, which excludes volatile food and energy prices, rose 0.30%, slightly above 0.20% recorded in the previous month.

The British Pound traded at £1/$1.26 on Friday, as investors weighed upcoming US tariffs and Bank of England (BoE) policy signals as the BoE Deputy Governor Dave Ramsden, speaking in South Africa this week, highlighted uncertainty around the UK labor market and global risks. President Trump confirmed 25% tariffs on imports from Mexico and Canada, along with a 10% duty on Chinese goods, however, he suggested a potential tariff-free trade deal with the UK.

The Euro weakened to €1/$1.04, as investors assessed economic data ahead of next week’s European Central Bank (ECB) policy meeting and reacted to US President Donald Trump announced plans to impose a 25% tariff on EU imports, including cars and other goods. Meanwhile, inflation in both Italy and Spain for February 2025 increased to 1.70% and 3.00%, from 1.50% and 2.90% in the previous month. The ECB is expected to cut interest rates for a fifth consecutive time on Thursday, with projections of further reductions amid slowing inflation and weak economic growth.

China’s official NBS Manufacturing PMI rose to 50.20 in February 2025 from 49.10 in January 2025. The latest reading highlighted that Beijing’s stimulus measures have supported recovery of the economy, which has been impacted by US tariffs, persistently weak domestic demand, and lingering deflation risks. The Non-Manufacturing PMI was at 50.40 in February 2025, up from 50.20 in the previous month.

Next week in the US, investors will focus on key economic data releases, including the Non-Farm Payrolls and Unemployment rate figures for February 2025.

GLOBAL MARKETS

Major US stocks closed lower this week, leading to a decline in major indexes driven by a selloff in technology and artificial intelligence stocks due to low earnings report which failed to impress investors, the President’s proposed 25% reciprocal tariffs on European autos and other goods, and rising concerns over escalating geopolitical risks after a tense exchange between President Donald Trump and Ukraine President Volodymyr Zelenskyy in the Oval Office. Compared to last week, the Nasdaq and S&P 500 indices decreased for the second week in a row by -3.38% and -0.98% to 20,884.41 and 5,954.50, while the Dow Jones Index increased by 0.95% to 43,840.91.

UK stocks outperformed other European markets as European stocks declined after US President Trump announced 25% tariffs on EU imports. Also, the equity markets witnessed a global selloff driven by growing fears of a trade war, further dampening market sentiment. The London’s Financial Times Stock Exchange (FTSE) 100 and the Germany’s Deutscher Aktien (DAX) indices increased by 1.74% and 1.18% to 8,809.74 and 22,551.43 while France Cotation Assistée en Continu (CAC) 40 index decreased by -0.53% to 8,111.63.

Chinese stocks closed lower as US President Donald Trump imposed an additional 10% tariff on imports from China, set to take effect on March 4. The escalating tariffs are expected to significantly impact China’s economy, which relies heavily on exports and free trade. The Hang Seng and Topix indices decreased by -2.29% and -1.99% to 22,941.32 and 2,682.09, respectively.

We expect cautious trading in the Global Equities market as Investors assess the impact of Trump’s Trade Tariffs set to take effect next week.

DOMESTIC ECONOMY

Nigeria’s economy grew by 3.84% year-on-year in the fourth quarter of 2024, according to the latest GDP data from the National Bureau of Statistics (NBS). This marks a 0.38%-point increase from 3.46% recorded in both the same period of 2023 and the previous quarter. Growth was driven by the Services sector, which expanded by 5.37% and contributed 57.38% to the country’s total GDP. Meanwhile the agriculture sector recorded a slower growth rate of 1.76%, a decline from 2.10% in Q4 2023. The industry sector also experienced slow growth, at 2.00%, lower than 3.86% in Q4 2023. For the full year 2024, Nigeria’s GDP grew by 3.40%, an increase from 2.74% in 2023.

President Bola Tinubu has signed the ₦54.99trillion 2025 appropriation bill into law, marking a 99.96% increase from the 2024 budget of ₦27.50trillion. The bill was approved by the National Assembly after revisions to the initial budget proposal of ₦49.70trillion, an increase of 10.64%. The key breakdown of the 2025 budget include: statutory transfers of ₦3.65trillion, recurrent (non-debt) expenditure of ₦13.64trillion, capital expenditure of ₦23.96trillion, debt servicing totaling ₦14.32trillion and a Fiscal Deficit of ₦13.08trillion.

The Central Bank of Nigeria (CBN) has reported a significant decline in credit given to the Government, which fell to ₦24.52trillion in January 2025, according to the latest data from the CBN’s Money and Credit Statistics, compared to ₦39.62trillion in November 2024 and ₦39.39trillion in October 2024. The downward trend in government credit is reflective of ongoing fiscal measures aimed at curbing excess borrowing and maintaining economic stability. On a year-on-year basis, credit to the government in January 2025 is slightly higher than the ₦23.52trillion recorded in January 2024, indicating a modest increase in government borrowing over the past one year.

The Federal Government, States, and Local Government Councils shared a total of ₦1.70trillion from the Federation Account revenue for January 2025, a 19.72% increase compared to ₦1.42trillion shared in December 2024. The distributable revenue includes ₦749.73billion in statutory revenue, ₦718.78billion in Value Added Tax (VAT) revenue, ₦20.55billion from the Electronic Money Transfer Levy (EMTL), and ₦214billion in augmentation. The FAAC report also highlighted increased collections from VAT, Petroleum Profit Tax, Companies Income Tax, Excise Duty, Import Duty, and CET Levies. However, it noted a decline in collections from the Electronic Money Transfer Levy (EMTL) and Oil and Gas Royalty receipts.

We await the release of the PMI for private sector and Balance of Trade figures for November 2024.

DOMESTIC MARKETS

The Securities and Exchange Commission (SEC) has announced a significant reduction in its Offer Approval time for companies, from over a year to two weeks. In a statement released on Monday, the SEC stated that approvals would now be granted within two weeks once all documents are complete, aiming to enhance the efficiency of the capital market and better support the development of Nigeria’s economy.

MONEY MARKET AND FIXED INCOME

System liquidity fluctuated throughout the week, opening negative which kept rates elevated. However, liquidity improved significantly midweek following an OMO maturity inflow of ₦813.25billion, easing funding pressures and causing rates to decline. Despite the FGN bond auction settlement of ₦910.30 billion on Wednesday, conditions improved by the end of the week, as liquidity closed at ₦130.94billion from -₦722.58billion last week . Consequently, the Open Repo Rate (ORR) and the Overnight Rate (O/N) decreased by 558bps and 550bps to 26.75% and 27.33%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 35bps to 19.88% against 20.23% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor and Long-tenor Bonds decreased by 56bps, 92bps and 67bps to 19.22% and 18.53% and 17.60%.

The FGN Bond Auction held this week, with an offer of ₦350billion across the APR 2029 and FEB 2031 Bonds. The total subscription was ₦1.63trillion and total allotment was ₦910.39billion, thus, the auction was oversold by ₦560.39billion. Stop rates decreased by 259bps and 317bps to 19.20% and 19.33% for the 19.30% FGN APR 2029 and 18.50% FGN FEB 2031 bonds respectively.

We anticipate the Nigerian Treasury Bills auction scheduled to hold next week, where ₦650billion will be offered across the 91-day, 182-day and 364-day tenors, against ₦1.30trillion maturing.

THE EQUITIES MARKET

Market Capitalization and All-Share Index decreased by -0.62% to close the week at ₦67.19trillion from ₦67.61trillion and 107,821.39 from 108,497.40 the previous week.

A total turnover of 1.85 billion shares worth ₦51.39billion in 63,090 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 2.00 billion shares valued at ₦49.49billion that exchanged hands last week in 70,853 deals. On a sectoral basis, the Banking, Insurance, Consumer Goods and Industrial Goods indices closed negative this week, at -3.08%, -4.56%, -0.36% and -0.51%, while the Oil and Gas index was the sole gainer, at 0.60%.

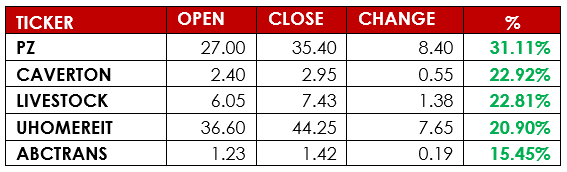

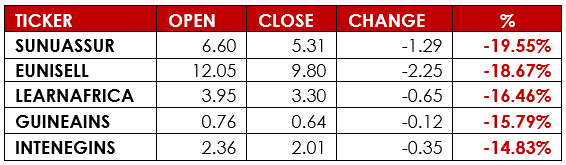

Notable gainers this week were PZ Cussons Nigeria Plc. and Caverton Offshore Support Grp Plc, while notable losers were Sunu Assurance Nigeria Plc and Eunisell Interlinked Plc.

We expect mixed sentiments to persist next week, albeit with a slightly negative tilt.

CURRENCY

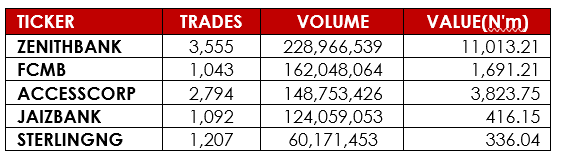

TOP TRADES BY VOLUME

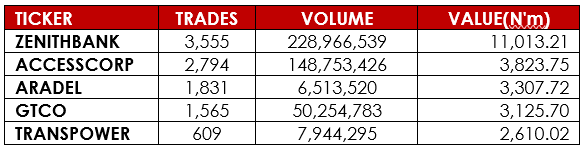

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.