GLOBAL ECONOMY

The US Personal Consumption Expenditures (PCE) price index increased by 0.30% month-on-month in February 2025, the same as the previous month. Prices of goods rose by 0.20%, compared to 0.50% in January while prices of services increased by 0.40%, above 0.20% in the previous month. Meanwhile, the core PCE index, which excludes volatile food and energy prices, increased by 0.40%, compared to 0.30% in the previous month.

The annual Inflation rate in the UK fell to 2.80% in February 2025 from 3.00% in January, in line with the Bank of England’s (BoE) forecast. The largest downward contribution came from prices of clothing, which fell to -0.60% compared to 1.80% in the previous month. Inflation also eased in recreation, falling to 3.40% compared to 3.80%. In contrast, Food Inflation was unchanged at 3.30%, while transport costs rose to 1.80% compared to 1.70%. The annual Core Inflation rate declined to 3.50% from 3.70% in January 2025.

The Euro climbed above €1/$1.08, the highest in one week after weaker-than-expected inflation data in France and Spain fueled expectations of more European Central Bank (ECB) rate cuts. Meanwhile, Investors are closely watching the incoming April 2nd deadline of U.S. President Trump reciprocal tariffs on key trading partners. While uncertainty over tariffs weigh on markets, analysts believe the announcement could lead to further negotiations, potentially softening the final impact of the tariffs.

China’s 10-year Government bond yield dropped to around 1.87% on Friday, as the Government increased debt issuance aimed at stimulating growth and stabilizing the bond market. In the first quarter of 2025, the Ministry of Finance raised ¥1.45trillion through Sovereign Bonds. This surge in debt issuance highlights Beijing’s growing urgency to increase fiscal spending in response to multiple economic pressures. Meanwhile, external pressures have intensified, as US President Donald Trump’s new tariffs on Chinese goods have added to the economic uncertainty. In response, Chinese policymakers have unveiled plans to issue ¥11.86trillion in new bonds this year.

Next week, Investors will closely monitor the trade war, as reciprocal tariffs on imports to the US are set to take effect on April 2nd, including a 25% levy on autos.

GLOBAL MARKETS

Stocks in the US closed sharply lower on Friday, weighed down by rising inflation concerns and growing trade policy uncertainty. The Nasdaq, S&P 500 and Dow Jones indices decreased by -2.39%, -1.53% and -0.96% to 19,281.40, 5,580.94 and 41,583.90, respectively.

The FTSE 100 closed almost flat this week as Investors assessed economic data. European stocks declined on Friday, as Investors reacted to U.S. economic data, putting pressure on European markets, which had already been weighed down by U.S. President Donald Trump’s announcement of a 25% tariff on foreign-made cars. London’s Financial Times Stock Exchange (FTSE) 100 increased by 0.14% to 8,658.85 while France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) decreased by -1.88% and -1.58% to 22,461.52 and 7,916.08.

China stocks declined amid tariff concerns as Investors braced for the new US tariffs. Lingering economic uncertainties and the lack of policy support in China also weighed on sentiment. The Hang Seng and Topix indices decreased by -1.11% and -1.67% to 23,426.60 and 2,757.25.

We expect the current volatility to persist in the Global Equities Market as Investors react to the reciprocal tariffs set to begin next week.

DOMESTIC ECONOMY

Nigeria’s money supply fell for the first time in 2025, dropping to ₦110.32trillion in February from ₦110.94trillion in January. The 0.56% decline is a result of continued liquidity management by the Central Bank of Nigeria (CBN), following earlier signs of monetary tightening and exchange rate adjustments. However, this is a 15.45% increase year-on-year compared to ₦95.56trillion in February 2024. The fall in M3, which includes both Net Foreign Assets (NFA) and Net Domestic Assets (NDA), reflect changes in both foreign reserves and domestic credit flows. It also reflects a shift in Nigeria’s liquidity structure, as the fall in NFAs dragged down the overall money supply, despite a rise in domestic credit and demand deposits.

The Federal Government, State Governments, and Local Government Councils shared a total of ₦1.68trillion as Federation Account revenue for February 2025, according to a communiqué issued after the Federation Account Allocation Committee (FAAC) meeting held in Abuja. This is a 0.12% decrease compared to ₦1.70trillion shared in January, reflecting a drop in key revenue streams including Value Added Tax (VAT), Petroleum Profit Tax (PPT), and Companies Income Tax (CIT).

The Minister of Finance and Coordinating Minister of the Economy, Wale Edun, engaged in discussions with the European Union (EU) Ambassador to Nigeria, Mr. Gautier Mignot, on a strategic investment portfolio package in Nigeria this week. The Ambassador proposed the establishment of a structured trade and investment dialogue framework to enhance collaboration in critical sectors such as infrastructure, green finance, and sustainable development, spotlighting the EU’s active €1.30billion investment portfolio in Nigeria, alongside recent engagements by the European Bank for Reconstruction and Development (EBRD) and the EU’s Global Gateway Investment Strategy designed to boost infrastructure and sustainable development across Africa.

We anticipate the release of the Purchasing Managers Index (PMI) for the Public and Private Manufacturing Sector for March 2025, to provide insights on the level of manufacturing activities in the Country.

DOMESTIC MARKETS

President Bola Ahmed Tinubu has signed into law the Investment and Securities Act (ISA) 2024. The new legislation, which repeals the former Investments and Securities Act No. 29 of 2007, is aimed at strengthening the legal and regulatory framework for investments and Capital Market activities in the country. A major achievement of the ISA 2024 is the expansion of SEC’s regulatory powers to meet the standards of global bodies such as the International Organization of Securities Commissions (IOSCO), allowing it to maintain its “Signatory A” status under IOSCO’s Enhanced Multilateral Memorandum of Understanding (EMMoU), a critical benchmark for credibility in global financial markets.

MONEY MARKET AND FIXED INCOME

System liquidity experienced fluctuations throughout the week, closing at ₦969.77billion from -₦1.96trillion last week. It stayed negative at the start of the week, despite FAAC inflows, FGN bond maturities worth ₦562billion, and coupon payments of ₦38billion. Midweek, more FAAC inflows slightly eased funding pressure but reversed when the FGN bond auction settlement of ₦271billion plunged liquidity lower. By the end of the week, additional inflows from the NLNG dividend refund, treasury bills maturities worth ₦1.18trillion, additional bond coupon payments of ₦164billion, and 13% derivation funds provided additional liquidity. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) decreased by 590bps and 594bps to 26.50% and 26.96%, respectively.

The Nigerian Treasury Bills (NTB) market average yield increased by 9bps to 18.97% against 18.88% last week. In the Bonds market, the average yield for the Short-tenor Bonds decreased by -1bp to 19.23%, while the average yield for the Medium-tenor and Long-tenor Bonds increased by 16bps and 3bps to 18.83% and 17.60%, respectively.

The FGN Bond auction held this week, with the DMO allotting ₦271.23billion competitively, and ₦152.45billion non-competitively from an offer of ₦300billion. The stop rates for the APRIL 2029 and May 2033 bonds were 19.00% and 19.99%, respectively. The Nigerian Treasury Bills Auction also held this week, with an offer of ₦700billion across tenors. The total subscription was ₦1.43trillion and total allotment was ₦808.73billion, thus, the auction was oversold by ₦108.73billion. Stop rates were unchanged for the 91-day and 182-day bills and declined by 31bps to 19.63% for the 364-day bill.

We anticipate further boosts in System Liquidity, following a ₦652.40billion OMO maturity next week.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 0.66% to close the week at ₦66.26trillion from ₦65.82trillion and 105,660.64 from 104,962.96 the previous week.

A total turnover of 7.52 billion shares worth ₦398.95billion in 61,312 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 2.90 billion shares valued at ₦48.06billion that exchanged hands last week in 57,044 deals. On a sectoral basis, the Banking, Consumer Goods, Insurance and Industrial Goods indices closed positive, at 5.61%, 0.33%, 1.89% and 0.22%, while the Oil and Gas Index was the sole loser at -1.65%.

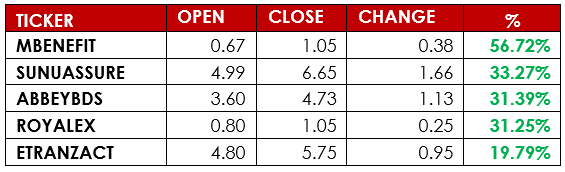

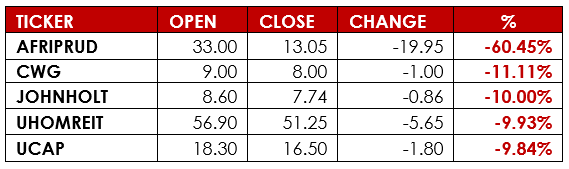

Notable gainers this week were Mutual Benefits Assurance Plc and Sunu Assurances Nigeria Plc, while notable losers were Africa Prudential Plc and CWG Plc.

DELISTING

MRS Oil Nigeria Plc has announced plans to voluntarily delist its shares from the Nigerian Exchange Limited (NGX) following a robust financial performance in 2024. The Company reported a 71.20% increase in revenue, reaching ₦312.20billion, and a profit after tax of ₦6.49billion. The decision to delist was approved by shareholders during an Extraordinary General Meeting (EGM) held on June 25, 2024. This move aims to provide the company with greater operational flexibility and reduce the costs associated with maintaining a listing on the NGX. Post-delist, MRS Oil intends to list its shares on the NASD OTC Securities Exchange to facilitate trading for interested investors.

We expect the rally to persist into the new week, with earnings announcements and potential corporate actions being key drivers of market sentiment.

CURRENCY

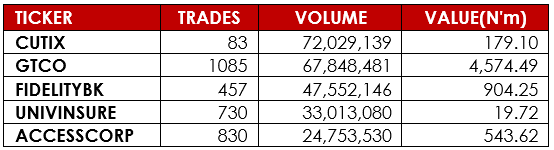

TOP TRADES BY VOLUME

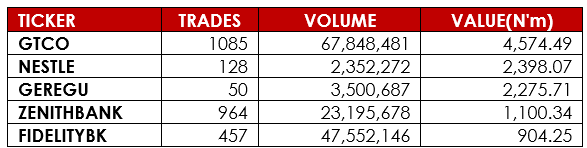

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research