GLOBAL ECONOMY

The US economy contracted by 0.20% in Q1 2025, compared to a 2.40% increase in Q4 2024. This is the first quarterly GDP contraction in three years as the US trade deficit in goods also fell significantly to $87.60billion, a 46% decline from $162.30billion in March. This was primarily driven by a 19.80% drop in imports, as new tariffs imposed by the Trump administration took effect. The US Personal Consumption Expenditures (PCE) price index increased by 0.10% from the previous month as goods prices rebounded slightly by 0.10% after a 0.50% decline in March, while service prices saw a 0.10% rise.

The British Pound traded at £1/$1.35 as Investors weighed growth and trade developments, following weak US economic data, Trump’s extension of the proposed 50% tariff to the EU and the upgrade of the UK’s growth forecast to 1.20% by the International Monetary Fund (IMF). In April 2025, UK major activity – car production – fell 15.80% year-on-year, influenced by multiple factors, including weakening demand in key export markets. Exports, which make up most of UK car production, dropped 10.10%, while domestic production declined 3.30%.

The Euro reversed losses to trade at €1/$1.13 following President Trump delay in the planned hike in tariffs on the EU, easing trade tension concerns as Investors processed economic data from Europe’s largest economies and developments in US trade policy. The Euro Area consumer confidence indicator rose by 1.40 to -15.20 in May 2025 from -16.60 in April as Inflation data showed Germany Consumer Price Index held steady at 2.10% in May, and inflationary pressures continued to ease in Italy, Spain, and France, reinforcing market expectations that the European Central Bank will cut interest rates by 25bps at its policy meeting next week.

The Yuan fell below ¥7.19/$1, as Investor caution grew amid stalled US-China trade negotiations China’s official NBS Non-Manufacturing PMI dipped to 50.30 in May 2025 from 50.40 in April, falling short of market expectations of 50.60 points and marking its lowest level since January. The decline reflected concerns over the impact of rising US tariffs on China’s service sector, despite a temporary pause in the trade war. Foreign Direct Investment (FDI) in China fell by 10.90% year-on-year to ¥320.8billion in the first four months of 2025, extending the 10.80% decline recorded in Q1. Despite the drop in total investment, the number of newly established Foreign-Invested Enterprises rose 12.10% to 18,832, signaling continued interest in China’s market.

Next week, Investors will tread carefully, weighing decisions with development on the tariff wars amidst growing consumer anxiety and a slowing US economy.

GLOBAL MARKETS

US stocks reversed earlier gains during the week, but closed on a positive note, as trade tensions escalated with trade negotiation stalling between US and China. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices increased by 2.01%, 1.88% and 1.60% to close at 19,113.77, 5,911.69 and 42,270.07 respectively.

In the UK and across Europe, major stocks closed positive despite persisting doubts about the tariff situation. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices increased by 0.62%, 0.23% and 1.56% to 8,772.38, 7,751.89 and 23,997.48 respectively.

Chinese stocks closed mixed with selling pressure persisting amidst uncertainty in the tariff wars between China and US. The Hang Seng index decreased by -1.32% to 23,289.77 while the Topix index increased by 2.41% to 2,801.57.

We anticipate cautious trading this week, amidst Investors’ optimism that the trade war tensions would ease.

DOMESTIC ECONOMY

Nigeria’s Debt Burden Deepens: AfDB Speaks on 75% of Revenue Spent on Interest Payment

The African Development Bank (AfDB) has warned that Nigeria’s debt burden is intensifying, with projections showing that 75% of Federal Revenues will be spent on interest payments in 2025. Despite a moderate debt-to-GDP ratio of 47%, the country faces significant financial strain as a large share of its income is allocated to servicing debt. While several African nations saw declining debt levels in 2022–2023 due to favorable economic conditions, the AfDB cautions that this trend remains fragile.

Foreign Portfolio Investment in Nigerian Equities Drops by 92.39% Amid Global Uncertainty

Foreign Portfolio Investment (FPI) into Nigeria’s stock market plummeted 92.39% in April 2025, as inflows fell to ₦26.64billion, down from ₦349.97billion in March. The decline was largely due to the absence of block trades that had boosted market activity earlier, coupled with global uncertainty discouraging foreign participation. Total foreign transactions dropped by 90.99%, from ₦699.89billion in March to ₦63.07billion in April, with Net Foreign Outflows standing at ₦9.79billion for the month. Foreign participation shrank to just 13.08%, compared to 62.74% in March. Meanwhile, Domestic Investors maintained their market dominance, accounting for 86.92% of total trade in April, with institutional activity rising 8.77% and Retail activity declining by 8.02%.

Nigeria’s Broad Money Supply (M3) Hits Record ₦119trillion Amid CBN’s Rate Pause

Nigeria’s broad money supply (M3) surged to ₦119.11trillion in April 2025, marking a 22.90% year-on-year increase and a 4.30% rise from March. The expansion comes as the Central Bank of Nigeria (CBN) maintains a tight monetary stance, holding the Monetary Policy Rate (MPR) at 27.50% in May. The liquidity boom was driven by a 66.30% rise in Net Foreign Assets (NFA), reflecting strong FX inflows from Crude Oil Sales, Multilateral Funding, and Diaspora Remittances. Meanwhile, Net Domestic Assets (NDA) grew at a modest 4.50% year-on-year, suggesting that government borrowing and private sector lending played a secondary role. Consumer liquidity also increased, with narrow money (M1) rising 6.40% from March, indicating heightened economic activity and short-term cash demand. However, concerns remain over whether this rapid money supply growth could rekindle inflation pressures, despite April’s marginal easing to 23.71%.

We await the release of the Q1 2025 GDP growth figures from the Central Bank of Nigeria (CBN), and the release of the Purchasing Managers Index for May to further guide economic outlook and sentiments.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System Liquidity stayed strong during the week despite the Sukuk Bond settlement, Omo auctions and net Cash Reserve Ratio (CRR) debits during the week. Consequently, short-term rates remained stable, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) increased slightly by 8bps and 3bps to close at 26.50% and 26.95%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 218bps to 18.61% last week. In the Bonds market, the average yield for the Short-tenor bond increased by 1bp to 19.22%, while Mid-tenor bonds decreased by 10bps to 19.03% and Long-tenor Bonds remained unchanged at 17.77%.

Next week Investors would turn their attention to the Treasury Bills market where the Federal government is offering ₦450billion across tenors against ₦321.31billion maturing.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization increased by 2.49% to close the week at 111,742.01 and ₦70.46trillion, compared to 109,028.62 and ₦68.75trillion last week.

A total turnover of 3.79 billion shares worth ₦119.39billion in 89,636 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 3.93 billion shares valued at ₦74.81billion that exchanged hands last week in 105,220 deals. On a sectoral basis, the Banking, Insurance, Consumer Goods and Industrial Goods indices all closed positive at 0.66%, 1.02%, 3.78% and 0.35%. The Oil and Gas index was the sole loser, closing at -2.05%.

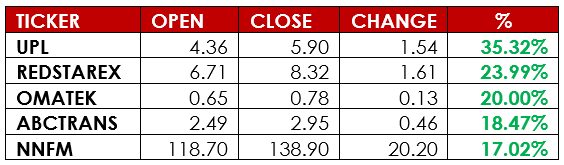

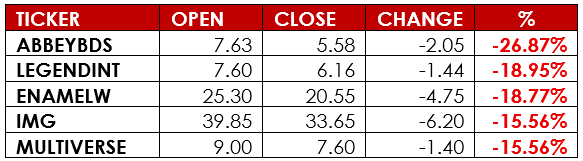

Notable gainers this week were University Press Plc and Red Star Express Plc while notable losers were Abbey Mortgage Bank Plc and Legend Internet Plc.

We anticipate Bullish Trading in the Equities market next week.

CURRENCY

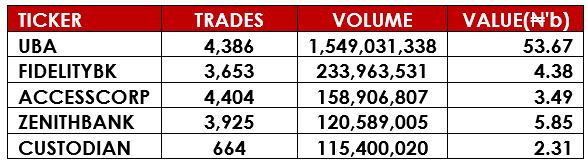

TOP TRADES BY VOLUME

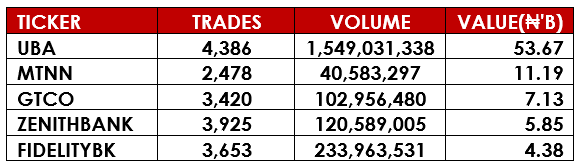

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.