GLOBAL ECONOMY

In the recent January 2025 meeting, the Federal Reserve (Fed) decided to keep interest rates steady at 4.50%. Fed Chair Powell reiterated the Fed’s cautious stance, emphasizing the lack of urgency concerning further rate adjustment. This decision suggests a cautious approach as the Fed monitors economic conditions and inflation trends.

The British pound hovered around £1/$1.24, as traders digested key monetary policy decisions from major Central Banks and assessed the economic outlook for the UK as the European Central Bank (ECB) lowered borrowing costs by 25bps. The Bank of England is still likely to cut rates by 25bps in February, as British finance minister Rachel Reeves outlined the government’s plans to boost growth through Infrastructure development.

The ECB lowered its key interest rates by 25bps in its January meeting, as expected, reducing the deposit facility rate to 2.75%, the main refinancing rate to 2.90%, and the marginal lending rate to 3.15%. This move reflects the ECB’s updated inflation outlook, with price pressures easing in line with expectations.

The Yuan steadied around ¥7.26/$1 following two consecutive sessions of losses, as investors took a break amid Lunar New Year celebrations. Market sentiment remained cautious, with concerns over President Donald Trump 10% tariff on Chinese imports starting February 1. Domestically, recent economic data painted a concerning picture, with China’s manufacturing activity contracting in January 2025, while services activity slowed sharply from December’s peak.

We await the release of the Jobs report for January 2025 in the US, as well as Institute for Supply Management Purchasing Managers’ Index (ISM PMI) to provide fresh insights into the economy’s Manufacturing and Service sector’s performance.

GLOBAL MARKETS

US stocks closed mixed this week, due to concerns about rumored delay in proposed tariffs and sell-offs in tech stocks triggered by Chinese startup DeepSeek’s announcement of a competitive AI model. The Nasdaq and S&P 500 indices decreased by -1.36% and -1.00% to 21,478.05 and 6,040.53, while the Dow Jones index increased by 0.27% to 44,544.66.

Stocks in the UK closed positive this week, following European markets after the ECB’s rate cut. The market gains were also fueled by US President Trump’s decision to avoid implementing aggressive tariffs on his first day in office, which eased market fears. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices all closed positive this week, increasing by 2.01%, 0.28% and 1.58% to 8,673.96, 7.950.17 and 21,732.05, respectively.

Asian stocks closed positive this week, supported by renewed investors interest as a result of the release of DeepSeek AI model rivalling USA’s OpenAI. The Hang Seng and Topix indices increased by 0.79% and 1.37% to 20,225.11 and 2,788.66, respectively.

We expect traders to closely monitor Trump’s policies, particularly the implementation of a 25% tariff on imports from Canada and Mexico, set to take effect on Feb 1st.

DOMESTIC ECONOMY

The Central Bank of Nigeria (CBN) monthly data on the Purchasing Managers’ Index (PMI) report for December 2024, revealed positive trends across key sectors as the PMI for December 2024 rose to 51.00 index points, compared to 48.90 points in November 2024. This signals a return to expansion in economic activities after two consecutive months of contraction. These include the stabilization of the industry sector, continued growth in the agricultural sector due to increased investment in food production and export-focused farming, and heightened consumer spending during the holiday season, which boosted small-scale manufacturing and trade.

The Debt Management Office (DMO) released a subnational debt report this week, showing that the domestic debt of the 36 states and the FCT stood at ₦4.21trillion on September 30, 2024, reflecting a decrease from ₦4.27trillion recorded on June 30, 2024. Lagos State topped the list of Nigerian states with the highest domestic debt, amounting to ₦853.43billion, followed by Rivers State with ₦389.20billion. Delta State ranked third with ₦342.53billion, while Ogun State and Imo State had domestic debts of ₦201.19billion and ₦155.38billion, respectively.

The Federal Inland Revenue Service (FIRS) reported an increase in Nigeria’s Value Added Tax (VAT) collections to ₦6.72trillion in 2024, an 84.62% increase compared to ₦3.64trillion recorded the previous year at the 2025 FIRS Management Retreat on Thursday. All tax categories recorded significant growth in 2024 compared to 2023, with non-oil taxes driving the majority of the increase.

The Central Bank of Nigeria (CBN) has approved the 2025 license renewal fee waiver for Bureau De Change (BDC) operators with immediate effect, as part of the Regulatory and Supervisory Guidelines for Bureau De Change Operations in Nigeria, 2024; and the ongoing transition to the new BDC regulatory structure. This announcement was made in a circular signed by the CBN’s Acting Director of the Financial Policy and Regulation Department, John Onojah, who advised BDC operators who had already paid the 2025 license renewal fee to apply for a refund to the account from which the payment was made.

We await the release of the Stanbic IBTC PMI which tracks the Private Sector Manufacturing Performance for January 2025.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity improved at the start of the week, driven by CRR credits, OMO maturities, and FAAC inflows but tightened midweek, following settlement debits after the FGN bond auction and a ₦600 billion OMO auction, with an oversubscription of ₦2.89trillion. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) increased by 214bps and 207bps to 29.14% and 29.57%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 175bps to 23.36% against 25.01% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor and Long-tenor Bonds increased by 2bps to 21.23% and decreased by 4bps and 1bp to 20.72% and 18.73% respectively.

The Federal Government Bond Auction was held on Monday 27th January 2025, with an offer size of ₦450billion across tenors. Total subscription was 1.49x the total amount that was offered, at ₦669.94billion, and total allotment was ₦606.46billion. The stop rate for the 19.30% FGN APR 2029 and 18.50% FGN FEB 2031 bonds increased by 65bps and 50bps, while the newly issued Jan 2035 bonds had a stop rate of 22.60%.

We anticipate cautious trading next week as investors shift their focus to the NTB auction, where ₦670billion will be offered across three tenors against ₦955.37billion maturing in the same week.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 1.67% and 0.87% to close at ₦64.71trillion from ₦63.65trillion and 104,496.12 from 103,598.30 the previous week.

A total turnover of 3.25 billion shares worth ₦69.20billion in 77,270 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 3.13 billion shares valued at ₦76.55billion that exchanged hands last week in 61,456 deals. On a sectoral basis, the Banking, Oil and Gas and Consumer Goods indices closed positive this week, at 2.54%, 0.97% and 4.01%, while the Insurance and Industrial Goods indices closed negative at -2.86% and -0.52%, respectively.

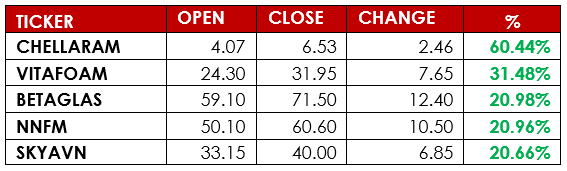

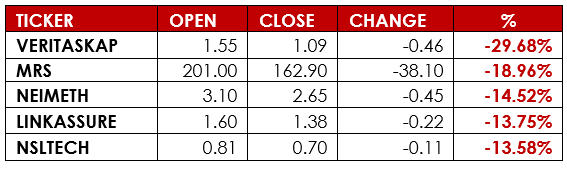

Notable gainers this week were Chellarams Plc and Vitafoam Nig. Plc, while notable losers were Veritas Kapital Assurance Plc and MRS Oil Plc.

DELISTING

The securities of the two (2) companies below have been delisted from the Nigerian Exchange Limited (NGX) effective Friday, 31 January 2025 on the grounds that they are operating below the listing standards of NGX, and their securities are no longer considered suitable for continued listing and trading in the market.

- Tourist Company of Nigeria Plc;

- Union Homes Savings and Loans Plc.

We expect the Equities market to trade with mixed sentiments next week.

CURRENCY

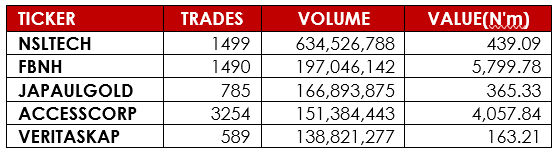

TOP TRADES BY VOLUME

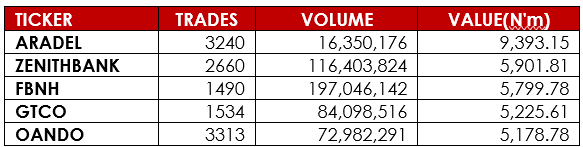

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research