GLOBAL ECONOMY

Initial jobless claims in the US fell by 9,000 to 211,000 in the last week of 2024, contrasting with the expected increase of 222,000, marking the lowest number of initial claims in eight months. In the previous week, continuing jobless claims fell by 52,000 to 1,844,000, below expectations of 1,890,000. This matches the view that the US labor market remains tight, setting a stance for the Federal Reserve to leave interest rates at high levels should inflation fall slower than the desired pace.

The British Pound dropped to £1/$1.24, its lowest in eight months, due to concerns over the UK’s economic resilience and a stronger US dollar. The UK economy has stagnated, with revised Q3 figures showing no growth, adding to challenges for Prime Minister Keir Starmer’s new government. Additionally, the Bank of England’s (BoE) decision at its final 2024 rate decision further depreciated the Pound sterling. The pound’s weakness also reflects worries about trade tensions, as Trump’s proposed tariffs could disrupt UK trade.

The Euro fell to €1/$1.03, due to concerns about Europe’s economic prospects and optimism around the US economy as markets prepare for Donald Trump’s return to the White House. Europe faces subdued growth expectations, with political instability in Germany and France as Trump’s potential trade tariffs increase the risks of a trade war. Meanwhile, a dovish stance by the European Central Bank has reduced support for the Euro, while the Federal Reserve is expected to cut interest rates less aggressively than anticipated due to inflationary risks from Trump’s policies, supporting the dollar.

China’s 10-year Government Bond yield fell to around 1.60%, following a signal from the People’s Bank of China (PBoC) of a significant shift in its monetary policy approach to stimulate the Chinese economy. On Friday, the Central Bank announced that it would prioritize interest rate adjustments over quantitative targets for loan growth. This initiative is part of a broader interest rate reform program.

We await the release of Initial Jobless Claims for next week, as well as the US Unemployment Rate.

GLOBAL MARKETS

US stock markets opened lower on Monday, as markets continued to assess the Fed’s policy outlook for next year. Major U.S. indices closed lower on Friday, despite a surge in the prices of big tech stocks. The Nasdaq index, S&P 500 and Dow Jones indices fell by -0.70%, -0.47% and -0.60% to 21,323.23, 5,942.60 and 42,731.53, respectively.

In the UK, Investors largely shrugged off a batch of weak economic data, despite ongoing uncertainties as the London’s Financial Times Stock Exchange (FTSE) 100 closed higher this week, increasing by 0.91% to 8,223.98. In the Euro Area, Investors were uncertain given the Trump proposed tariffs as Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices closed negative this week, decreasing by -0.39% and -0.99% to 19,906.08 and 7,282.22.

In Asia, Investors cited growing economic concerns, overshadowing Beijing’s latest efforts to stabilize market sentiment. A lack of concrete policy announcements this month, coupled with the looming trade war with the US ahead of Donald Trump’s inauguration on January 20, contributed to the fall in stock prices as the Hang Seng and Topix indices decreased by -1.64% and -0.59% to close at 19,760.27 and 2,784.92, respectively.

We anticipate increased volatility in the coming week, influenced by factors such as potential trade tensions under the Trump administration and the market’s recent tech-driven rally.

DOMESTIC ECONOMY

The Stanbic IBTC Bank Purchasing Managers Index (PMI) rose to 52.70 in December 2024, up from 49.60 in November 2024, after five months of decline. This indicates a return to growth in the country’s private sector, with all four key sectors reporting increased output. New orders rose for the second consecutive month as firms increased both employment and purchasing activity due to improved business conditions. However, strong inflationary pressures persisted, leading to higher purchase prices driven by currency weakness and rising fuel and transportation costs, which also pushed up staff costs. As a result, companies increased output prices at a slightly faster pace than in November.

The Federal Government’s (FG) deficit spending rose by 28.00% year-on-year to ₦12.10trillion in the first ten months of 2024, according to data from the Central Bank of Nigeria (CBN) Monthly Economic Reports for October 2024. This marks a significant jump from ₦9.80trillion recorded during the same period in 2023. This also indicates that the Federal Government surpassed its 2024 Budget deficit target of ₦9.80trillion by 31.00%. Despite the growth in deficit spending, the Federal Government experienced a 36.00% year-on-year increase in revenue during the period, driven largely by higher inflows into the Federation Account.

Nigeria’s Broad Money Supply (M2) increased by 51.00% year-on-year to ₦108.96trillion in November 2024, fueled by increasing domestic borrowings by the Federal Government, compared to ₦72.03trillion recorded in the same period of 2023, according to the CBN’s Money and Credit Statistics released on Monday. M2 encompasses cash and demand deposits, savings deposits, money market deposits, and time deposits, serving as a broad measure of liquidity in the economy.

Market participants await the Central Bank of Nigeria’s economic plans for 2025, which is expected to provide key insights into the country’s Monetary Policy direction for the year.

DOMESTIC MARKETS

FMDQ Exchange temporarily suspended Security Admission Services in the Nigerian Commercial Paper (CP) Market following new rules released last month by the Nigerian Securities and Exchange Commission. The Suspension is effective from December 30, stating that all ongoing CP offers by Prospective Issuers/Registration Members of the Exchange, are currently suspended. The SEC’s new rule stipulates fresh conditions for CP Issuance outlining strict measures to be adhered to by exchanges, including approval from the Commission regarding proposed issuances and Investment grade credit ratings of the Issuer.

MONEY MARKET AND FIXED INCOME

System liquidity opened the year positive, with the absence of major inflows or debits, as the Open Repo Rate (ORR) and Overnight Rate (O/N) rose by 25bps and 14bps to 26.75% and 27.25%, respectively.

The Nigerian Treasury Bills (NT-Bills) market average yield increased by 6bps to 25.57% against 25.51% last week. In the Bonds market, the average yield for the Short-tenor Bonds increased by 15bps to close at 20.15%, while the average yield for the Medium-tenor Bonds decreased by -59bps to 20.08%. The average yield for the Long-tenor Bonds remained unchanged at 17.94% on a week-on-week basis.

The Federal Government will be offering ₦515billion across tenors at its Treasury Bill Auction, which is scheduled to hold on Wednesday, 8th January 2025.

We anticipate increased activity in the Fixed Income market next week, as the FG prepares to hold its first Treasury Bill auction for the year.

THE EQUITIES MARKET

The market opened for four trading days this week as the FG declared Wednesday January 1, 2025, as Public Holiday to commemorate the New Year Day Celebration.

Market Capitalization and All-Share Index increased by 2.02% and 1.42% to close at ₦63.17trillion from ₦61.91trillion and 103,586.33 from 102,133.30 the previous week.

A total turnover of 2.62 billion shares worth ₦69.74billion in 47,953 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 1.39 billion shares valued at ₦52.02billion that exchanged hands last week in 33,411 deals. On a sectoral basis, the Banking, Insurance, Consumer Goods and Industrial Goods indices all closed positive at 0.58%, 26.91%, 2.16% and 0.50%, respectively. The Oil and Gas index was the sole loser for the second time, closing at -0.45%.

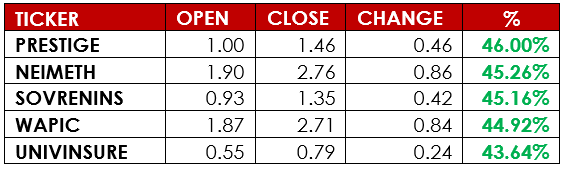

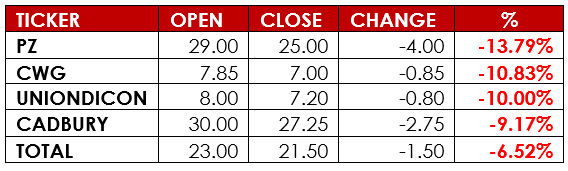

Notable gainers this week were Prestige Assurance Plc and Neimeth International Pharmaceuticals Plc, while notable losers were P Z Cussons Nigeria Plc and CWG Plc.

We expect that the Nigerian equities market will continue its modest positive trend next week.

CURRENCY

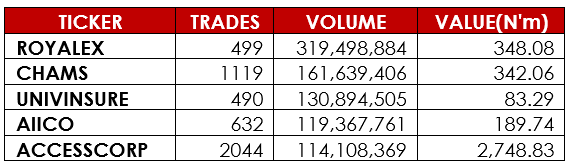

TOP TRADES BY VOLUME

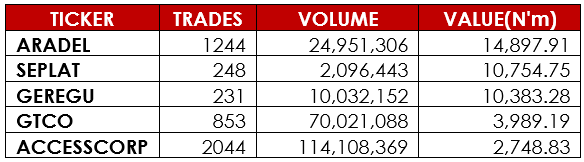

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSER

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research