GLOBAL ECONOMY

Trump declared “Liberation Day” on April 2nd, 2025, with the announcements of comprehensive tariffs aimed at reshaping U.S. trade relationships. The measures include a 10% baseline tariff on imports from all countries, with significantly higher rates imposed on nations with trade surpluses with the U.S., such as China (34%), the European Union (20%), Japan (24%), and others. Additionally, a 25% tariff on all foreign-made automobiles was introduced. Trump justified these tariffs as a strategy to revitalize domestic manufacturing and reduce trade deficits.

The British pound surged to £1/$1.30, boosted by a sharp decline in the US dollar. The move came as traders reacted to the latest round of reciprocal tariffs announced by Donald Trump with 10% tariffs on UK imports. The announcement, however, triggered a flight to safety and a shift toward risk-off assets, as investors grew increasingly concerned about the potential impact on the global economy. Although the UK faced a lower tariff rate with the promise to retaliate against the US, Investors fear that higher duties on other economies such as China and the Eurozone could lead to product dumping, undermining UK export competitiveness, thus, the UK remains vulnerable to the broader impact of global trade tensions.

The Euro hovered around €1/$1.10, as the dollar remained weak and trade war tensions intensified. In Europe, French President Emmanuel Macron urged companies to pause U.S. investments, while the European Commission said it is preparing its own countermeasures in response to the tariffs. Meanwhile, recent economic data showed that Eurozone inflation rate fell to 2.20% in March, the lowest level since November 2024, while Core inflation dropped to 2.40%.

The Yuan strengthened at the end of the week, following China’s announcement of reciprocal tariffs on US imports. The Customs Tariff Commission of the State Council stated that China will impose additional 34% tariff on all American goods, effective April 10, 2025, after President Trump unveiled a 34% tariff on Chinese imports on Wednesday, pushing the total levies on China to 54%. This move represents the largest ever tariff hike on nearly all Chinese exports, potentially crippling China’s shipments to the US. China also announced that it will soon restart negotiations with the EU to improve cooperation between Chinese and European companies, particularly in the electric vehicle sector.

Next week, Investors will closely monitor the CPI and PPI data to gain insights into how tariffs are affecting inflation, while Federal Open Market Committee (FOMC) minutes could provide further clues on the Fed’s policy outlook.

GLOBAL MARKETS

US stocks fell to their lowest this week, extending heavy losses after China announced a 34% tariff on all U.S. goods in retaliation for President Trump’s 54% levy on Chinese imports. The Nasdaq, S&P 500 and Dow Jones indices decreased by -9.77%, -9.08% and -7.86% to 17,397.70, 5,074.08 and 38,314.86, respectively.

The FTSE 100 dropped amid market turmoil from Trump’s tariff plans. European stocks also plunged on Friday from fresh US tariffs and growing recession fears. London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) all decreased by -6.97%, -8.10% and -8.10% to 8,054.98, 20,641.72 and 7,274.95.

Asian stocks had a massive decline following US President Donald Trump’s announcement of a 34% reciprocal tariff on China, escalating the trade conflict between the world’s two largest economies. The Hang Seng and Topix indices decreased by -2.46% and -9.98% to 22,849.81 and 2,482.06.

Next week, the trade war will remain a key focus, with traders evaluating the impact of US tariffs and potential responses from other countries.

DOMESTIC ECONOMY

Nigeria’s Total Public Debt Increases

Nigeria’s total public debt rose to ₦144.67trillion ($94.23billion) as of December 31, 2024, an increase of 48.58% compared to ₦97.34trillion ($108.23billion) recorded at the end of December 2023. This latest figure was released by the Debt Management Office (DMO) on Friday, 4th April 2025. The report also indicated a quarter-on-quarter rise of 1.65% from ₦142.32trillion ($88.89billion) recorded at the end of September 2024, highlighting the continued increase in the Nation’s debt burden within the final quarter of the year.

World Bank Plans $10.50 Million Grant to Strengthen Nigeria’s Central Bank

The World Bank has unveiled a plan to provide Nigeria with a $10.50million grant, aimed at bolstering the technical capacity of the Central Bank of Nigeria (CBN). The initiative forms part of the Finance for Development Multi-Donor Trust Fund and is set to revolutionize Nigeria’s domestic payment infrastructure. This grant focuses on integrating advanced technologies and enhancing risk-based supervision processes within the CBN. Key objectives include improving operational efficiency, data accuracy, and modernizing payment systems, particularly for remittances. The grant seeks to facilitate safer and more reliable transactions while encouraging the formalization of informal remittance channels.

Trump Imposes 14% Tariff on Nigerian Exports

The United States announced a 14% tariff on Nigerian exports, signalling a major change in trade relations. This policy, primarily targeting crude oil—a key export for Nigeria—has significant implications for the country’s economy. Reduced competitiveness in the U.S. market could force Nigeria to seek alternative buyers, likely at lower prices, potentially impacting revenue generation and economic stability.

Private Sector Purchasing Managers’ Index (PMI) hits 54.30

The Private sector PMI for March 2025 reached 54.30 from 53.70 in February, a sign of strong private sector growthdriven by rising new orders and softer inflation. The recovery in the Nigerian private sector saw increases in output, new orders and employment as firms enjoyed softening inflationary pressures, with input costs rising slowly compared to the previous months.

We expect CBN to intervene in the FX market, as offshore demand intensifies against the pressures of declining global oil consumption and rising OPEC+ production.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity remained robust throughout the week, opening at ₦1.50trillion, but declined due to CBN’s Cash Reserve Ratio (CRR) debits. Mid-week, liquidity improved largely driven by ₦651billion in OMO maturities, closing at ₦969.64billion from ₦969.77billion last week. Consequently, the Open Repo Rate (ORR) remained unchanged at 26.50% while the Overnight Rate (O/N) decreased by 10bps to 26.86%.

The Nigerian Treasury Bills (NTB) market average yield increased by 63bps to 19.99% against 19.36% last week. In the Bonds market, the average yield for the Short-tenor, Medium-tenor and Long-tenor Bonds remained unchanged at 18.98%, 19.00% and 17.83%, respectively.

We anticipate cautious trading this week, as Investors await the release of Q2 2025 Treasury Bills Auction calendar.

THE EQUITIES MARKET

The Equities market opened for three trading days this week as the Federal Government of Nigeria declared Monday 31st March and Tuesday 1st April 2025 as Public Holidays to commemorate 2025 Eid el Fitr celebration.

Market Capitalization and All-Share Index decreased by -0.17% and -0.14% to close the week at ₦66.15trillion from ₦66.26trillion and 105,511.89 from 105,660.64 the previous week.

A total turnover of 1.18 billion shares worth ₦28.87billion in 42,397 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 7.52 billion shares valued at ₦398.95billion that exchanged hands last week in 61,312 deals. On a sectoral basis, the Oil and Gas, Consumer Goods, Insurance and Industrial Goods indices closed negatively, at -1.18%, -0.91%, -4.13% and -0.22%, while the Banking Index was the sole gainer at 0.22%.

Notable gainers this week were VFD Group Plc and Union Dicon Salt Plc, while notable losers were UACN Plc and Sunu Assurances Nigeria Plc.

DELISTING

The securities of the three (3) companies were delisted from the facilities of Nigerian Exchange Limited (NGX) effective on Thursday, 3 April 2025 on the grounds that they are operating below the listing standards of NGX, and their securities are no longer considered suitable for continued listing and trading in the market:

- Capital Oil Plc

- Goldlink Insurance Plc

- Medview Airline Plc

We expect cautious trading in the equities market, as Investors seek reinvestments opportunities.

CURRENCY

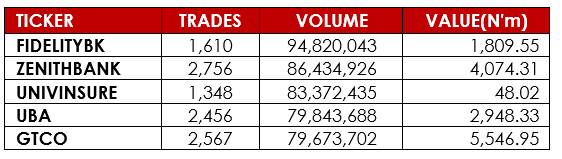

TOP TRADES BY VOLUME

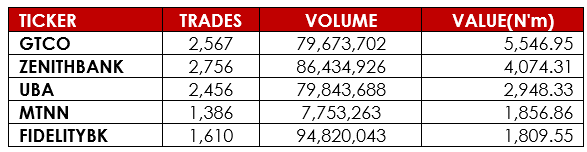

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research