GLOBAL ECONOMY

The US Non-farm payrolls rose by 147,000 and Unemployment dipped to 4.10% from 4.20% in May, despite private sector jobs falling by 33,000 amidst service sector losses. Job openings surged to 7.77 million, while job quits increased by 3.29 million, reflecting a cooling but resilient labor market. The S&P Global Purchasing Managers’ Index (PMI) rose to 52.90 from 52.00 in May, while Services growth slowed slightly. The trade deficit widened sharply to $71.50billion in May from $60.30billion as exports dropped 4%, as President Trump announced a plan to impose flat tariffs starting July 9, bypassing traditional negotiations.

The Pound weakened toward £1/$1.36 after a strong US jobs report. The UK economy grew by 0.70% quarter-on-quarter in Q1 2025 and 1.30% year-on-year in June, its strongest quarterly pace in a year, driven by services (+1.40%), construction (+1.20%), and strong business investment (+6.10%). However, the current account deficit widened to £23.50billion (3.20% of GDP), due to a sharp drop in primary income and a narrowing services sector surplus. The Purchasing Managers’ Index (PMI) rose to 52.00 from 50.30 in May, signaling modest private sector growth with political reassurance from Prime Minister Starmer and expectations of a Bank of England rate cut as early as August.

The EU Unemployment rate ticked up to 6.30% in May from 6.20% in April, with youth unemployment at 14.40%. PMI data showed modest recovery with the Composite PMI rising to 50.60, Services PMI reaching 50.50, and Manufacturing PMI hitting 49.50, while Construction PMI fell to 45.20. The EU Producer price Index dropped by 0.60% Month-on-Month in May. Business confidence is improving, but trade tensions and weak demand continue to weigh on growth.

The offshore Yuan held steady around ¥7.16/$1 as markets digested the mixed data and awaited further policy signals. China’s Composite PMI rose to 50.70 from 50.40 in May. Foreign sales remained weak, with services exports declining. China raised its Qualified Domestic Institutional Investor (QDII) quota, a program that enables approved domestic investors to access overseas markets, to $170.90billion to ease capital controls, while imposing a five-year anti-dumping tariffs on EU brandy, escalating trade tensions.

Investors globally will monitor trade tensions as US-China 90 days pause comes to an end while watching out for key monetary policies, major economic data, Q2 earnings.

GLOBAL MARKETS

Last week, U.S stocks closed high following the rise in the Non-Farm Payroll. Compared to last week, the Dow Jones, Nasdaq and S&P indices increased by 2.30%, 1.62% and 1.72% to close at 44,828.53, 20,601.10 and 6,279.35 respectively.

In the UK and across Europe, major stocks closed mixed with some closing lower with the trade tensions with the United State. The London’s Financial Times Stock Exchange (FTSE) 100 and France Cotation Assistée en Continu (CAC) 40 indices increased by 0.27% and 0.06% to 8,822.91 and 7,696.27 while Germany’s Deutscher Aktien (DAX) decreased by -1.02% to 23,787.45.

The Asian stock market closed mixed last week with market struggling for clear direction as Investors react to the global trade uncertainties. The Hang Seng and Topix indices decreased by -1.52% and -0.44% to 23,916.06 and 2,827.95 respectively.

This week, Investors will focus on the trade developments in US following the formal letters sent by Trump’s Administration ahead of July 9th deadline.

DOMESTIC ECONOMY

Nigeria’s Private Sector Growth Slows to 7-Month Low at 51.60, But Business Confidence Hits 22-Month High

Nigeria’s PMI fell to 51.60 in June from 52.70 in May, marking the slowest private sector expansion in seven months, driven by a sharp drop in manufacturing output. Despite the slowdown, business confidence surged to 83.90, its highest since August 2022, on expectations of increased investment and operational expansion. Inflationary pressures eased for the second month, with output prices rising at the slowest pace in over two years, though Manufacturing sector still saw the fastest price hikes. Employment remained stable, purchasing activity slowed, and backlogs rose modestly due to supply chain issues and delayed payments.

Private Sector Credit Dips to ₦77.83trillion Despite Surging Liquidity, IMF-Backed Tight Policy

Nigeria’s private sector credit fell slightly to ₦77.83trillion in May 2025 from ₦77.91trillion in April, reflecting a 0.10% decline amid the CBN’s tight monetary stance. This comes despite a 7.11% Year to Date (YTD) surge in broad money supply (M3) to ₦119.01trillion. Credit growth remains sluggish – up just 0.58% YTD – highlighting a disconnect between liquidity and lending. Services dominate credit allocation (₦32.15trillion), while manufacturing and commerce allocations continue to shrink, with Private Sector Credit-to-GDP ratio falling to 27.81%. This shows that the economy is expanding without proportional bank financing, signaling deepening credit constraints despite IMF support for the CBN’s inflation-fighting policies.

Nigeria’s Public Debt Hits ₦149.39trillion Amid Rising Borrowing and Currency Pressures

As of March 31, 2025, Nigeria’s total public debt surged to ₦149.39trillion, reflecting a ₦27.72trillion or 22.80% year-on-year increase from ₦121.67trillion in March 2024, and a ₦7.07trillion or 3.30% rise from December 2024. This growth, according to the Debt Management Office (DMO), is driven by fresh borrowings and the impact of Naira depreciation on external debt. External debt stands at $45.90billion (₦70.63trillion), with multilateral lenders like the World Bank ($18.3billion), IMF (fully repaid), and AfDB ($3.5billion) accounting for $22.50billion, while bilateral loans total $6.70billion, led by China ($5.16billion). Commercial debt, mainly Eurobonds, remains at $17.32billion. On the domestic front, debt reached ₦78.76trillion, dominated by FGN Bonds (₦59.80trillion) and Treasury Bills (₦12.70trillion).

This week, Investors will watch out for the release of Q2 GDP and annual GDP growth report.

DOMESTIC MARKETS

Commercial Papers Surge in Nigeria as Firms Seek Cheaper, Flexible Funding

Nigeria’s corporate financing is shifting rapidly as Commercial Papers (CPs) become the go-to short-term funding tool, with issuances ranging from ₦3billion to a record ₦193.25billion by Access Bank at yields up to 24.75%. With the Central Bank’s MPR at 27.50%, CPs offer a cheaper alternative to bank loans, drawing issuers like MeCure (₦10billion at 26%), Daraju (₦4billion at 25%), and FCMB (₦70billion). Total CP programmes now exceed ₦8.19trillion, with quoted CPs at ₦7.23trillion. Investors are also flocking in, attracted by yields of 19% – 30%, far outpacing Treasury Bills and FGN Bonds.

MONEY MARKET AND FIXED INCOME

System Liquidity opened the week strong note but tightened midweek following a ₦600billion OMO auction and corporate tax remittance closing the week positive at ₦811.56billion. Short-term rates closed higher, as the Open Repo Rate (ORR) and the Overnight Rate (O/N) increased by 33bps and 42bps to 26.83% and 27.42% respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 23bps to 18.07% last week. In the Bonds market, the average yield for the short-tenor, mid-tenor and long-tenor bonds decreased by 99bps, 92bps and 98bps to 18.00%, 17.71% and 16.31% respectively.

We anticipate cautious trading next week, amidst buying interest ahead of the release of the Q3 NTB issuance calendar.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 0.83% and 0.50% to close the week at 120,989.66 and ₦76.34trillion, compared to 119,995.76 and ₦75.96trillion last week.

A total turnover of 5.47 billion shares worth ₦108.10billion in 118,570 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 3.90 billion shares valued at ₦102.22billion that exchanged hands last week in 114,484 deals.

On a sectoral basis, the Banking, Insurance, Oil and Gas and Consumer Goods indices closed positive at 0.12%, 5.86%, 0.77%, 4.08%, while Industrial Goods index closed negative at -2.11%.

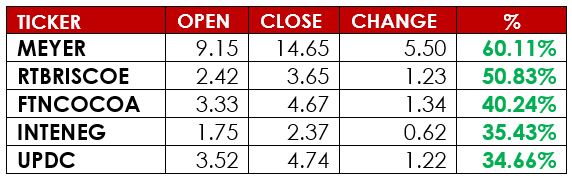

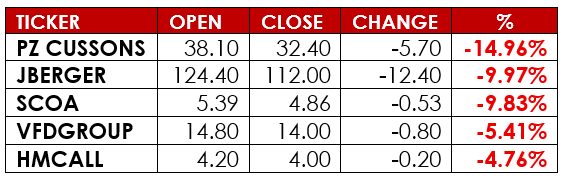

Notable gainers this week were Meyer PLC and RT Briscoe PLC, while notable losers were Julius Berger Nigeria PLC and PZ Cussons Nigeria PLC.

Nigerian Stock Market Gains 16.57% in H1 2025, Led by Consumer Goods and Banking Sectors

Nigeria’s stock market closed the first half of 2025 with a 16.57% gain in the All-Share Index, rising from 102,928.60 in January to 119,978.60 in June. The rally was driven by strong performances in Consumer Goods (+52.21%), Banking (+18.06%), and Insurance (+5.23%), while Industrial Goods posted a modest 1.85% gain. The Consumer Goods sector led the charge with standout stocks like Honeywell Flour Mills (+241.30%) and Vitafoam (+221.74%). Despite gains in select stocks, the Oil and Gas sector declined by 10.12%, weighed down by losses in Seplat, Aradel, and Oando. Total market volume reached 67.08 billion shares, with May and June seeing the highest activity.

This week, Investors will watch out for the release of the half-year earnings to further guide sentiments and decisions.

CURRENCY

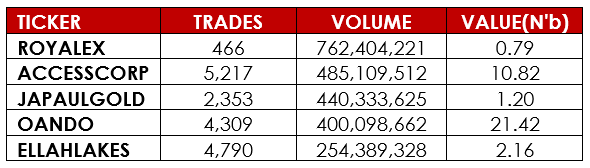

TOP TRADES BY VOLUME

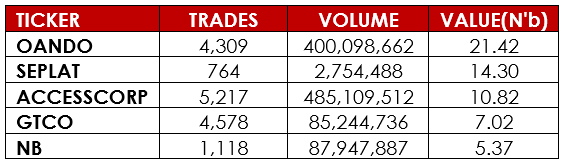

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.