GLOBAL ECONOMY

The US unemployment rate remained steady at 4.20% for the second consecutive month in May. The number of unemployed persons increased by 71,000, reaching 7.24 million while the US Nonfarm Payrolls increased by 139,000, lower than 147,000 in April. The US Balance of Trade (BoT) gap narrowed significantly to $61.60billion, down from $138.30billion in March with US imports declining by 16.30% to $351billion in April 2025. Goods imports fell by $68.90billion to $277.90billion, mainly due to drops in pharmaceuticals and passenger cars imports while services imports edged up $0.50billion to $73.10billion. Exports hit a record high of $289.40billion, rising by 3% as Goods exports climbed by $6.20billion to $190.50billion, while declines were seen in crude oil, passenger cars and trucks.

The British Pound traded at £1/$1.36 as Investors confidence received a boost following a positive trade-focused call between US President Trump and China’s President Xi, which Trump characterized as “very good.” UK consumers’ credit borrowing rose to £1.58billion, surpassing March’s £1.10billion and market expectations of £1.10billion. May’s Manufacturing Purchasing Managers Index (PMI) rose up to 46.40 points, improving from April’s 45.40 points, but still indicating challenging conditions.

Eurozone Consumer Price Inflation (CPI) eased to 1.90% year-on-year in May 2025, down from 2.20% in April and below market expectations of 2.00%. This marks the first time inflation has fallen below the European Central Bank’s (ECB) 2.00% target since September 2024. Subsequently, the ECB reduced key interest rates by 25bps this week, reflecting updated inflation and economic forecasts. In Q1 2025, the Eurozone economy expanded by 0.60%, doubling the earlier 0.30% estimate and marking the strongest growth since Q3 2022, fueled by Ireland’s exceptional 9.70% surge and stronger-than-expected performance from Germany (0.40%). Spain also grew by 0.60%, while Italy (+0.30%), France (+0.10%), and the Netherlands (+0.10%).

The Yuan fell below ¥7.18/$1, as optimism over renewed US-China trade talks failed to lift market sentiment. China’s foreign exchange reserves climbed $3.60billion to $3.29trillion, hitting their highest level since September 2024. The increase was driven by a weaker US Dollar against other major currencies and asset price fluctuations. The General Manufacturing PMI unexpectedly fell to 48.30, down from April’s 50.40, marking the first contraction in eight months and the sharpest decline since September 2022. Despite challenges, business sentiment improved, supported by expectations of better trade conditions ahead.

Next week, Investors will navigate uncertainty from US tariff negotiations and the Trump-Musk rift, focusing on its potential impact on the US economy.

GLOBAL MARKETS

Last week, US stocks rallied after a stronger-than-expected jobs report eased worries about the state of the economy. Compared to last week, the Dow Jones, S&P 500 and Nasdaq indices increased by 1.17%, 1.50% and 2.18% to close at 42,762.87, 6,000.36 and 19,529.95 respectively.

In the UK and across Europe, major stocks closed positive boosted by strong gains in gold mining stocks and sentiments improved following good reports from the US-China trade negotiations. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices increased by 0.75%, 0.68% and 1.28% to 8,837.91, 7,804.87 and 24,304.46 respectively.

The Asian stock market was laced with uncertainty this week as stocks struggled for clear direction following a high-level call between US President Donald Trump and Chinese President Xi Jinping. The Hang Seng index increased by 2.16% to 23,792.54 while the Topix index decreased by -1.15% to 2,769.33.

We anticipate cautious trading this week, as Investors monitor the tariff trade war and inflation reports, trade data, and economic indicators across China, Europe, and the Asia-Pacific region.

DOMESTIC ECONOMY

Moody’s upgrade of Nigeria’s credit rating to B3

Moody’s upgraded Nigeria’s credit rating from Caa1 to B3, citing improved fiscal and external positions. The economic outlook shifted from positive to stable, with further growth expected despite inflation concerns. Fitch Ratings also raised Nigeria’s outlook to stable, praising reforms like exchange rate liberalization, tighter monetary policy, and subsidy removal, which boosted Investor confidence. The Central Bank’s FX reforms narrowed the market gap and improved liquidity after last year’s 40% Naira depreciation.

Private Sector PMI Drops as Business Growth Slows

Nigeria’s private sector headline PMI fell to 52.70 points from April’s 54.20 points, marking the weakest expansion since January. Despite staying above 50.00, growth momentum softened, with output and new orders rising at their slowest pace in four months. Inflation pressures persisted, fueled by higher raw material prices, currency weakness, and increased transport costs. Staff costs rose, but at a slower pace due to declining employment, leading firms to pass costs to customers. Still, firms remained optimistic about future growth, driven by expansion efforts, marketing, and restocking plans.

Nigeria’s Business Performance Index Holds Positive Momentum Despite Challenges

Nigeria’s Business Performance Index (BPI) remained positive for the fifth consecutive month in 2025, with May’s index at +9.78, though lower than April’s +12.29 highlighting power shortages as the top business constraint, alongside financing issues and economic policy uncertainties. With Manufacturing (+14.43), Trade (+14.13), and Services (+4.49) showing resilience, Agriculture declined (-1.77) due to climate-related disruptions. Business confidence weakened, with investment sentiment (-25.61) and price levels (-18.15) declining.

We await the release of the Q1 2025 GDP growth figures from the Central Bank of Nigeria (CBN).

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System Liquidity stayed strong during the week with Infrastructure Inflows and Bond Coupon payments offering relief despite the CBN’s ₦1.51trillion OMO allotment causing a ₦1.14trillion liquidity withdrawal, reducing system liquidity to ₦706.49billion during the week. Consequently, short-term rates remained stable, as the Open Repo Rate (ORR) remained unchanged at 26.50% while the Overnight Rate (O/N) increased slightly by 1bps to close at 26.96% respectively.

The Nigerian Treasury Bills (NTB) market average yield increased by 18bps to 18.79% last week. In the Bonds market, the average yield for the short-tenor bond increased by 1bp to 19.23%, while mid-tenor and long-tenor bonds decreased by 5bps and 7bps to 18.98% and 17.70% respectively.

The Nigeria Treasury Bills Auction held last week witnessing strong demand on the 364-days bill, as total subscription was 2.90x the total offer, at ₦1.309trillion. The bid-to-cover ratio was 3.27x and total allotment was ₦400.05billion, slightly lower than the initial offer of ₦450billion, thus, the auction was undersold by ₦49.95billion. Stop rate for the 182-day bill remained unchanged at 18.50% while the 91-day and the 364-day bills decreased by 2bps and 21bps to close at 17.98% and 19.35% respectively.

We expect the current sentiment to persist this week.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization appreciated by 2.57% to close the week at 114,616.75 and ₦72.28trillion respectively, compared to 111,742.01 and ₦70.46trillion last week.

A total turnover of 3.21billion shares worth ₦76.35billion in 64,156 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 3.79billion shares valued at ₦119.39billion that exchanged hands last week in 89,636 deals. On a sectoral basis, the Banking, Insurance, Consumer Goods, Industrial Goods and the Oil and Gas indices all closed positive at 4.69%, 3.36%, 2.33%, 1.18% and 3.33% respectively.

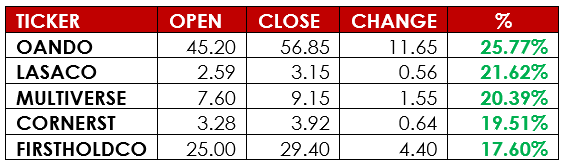

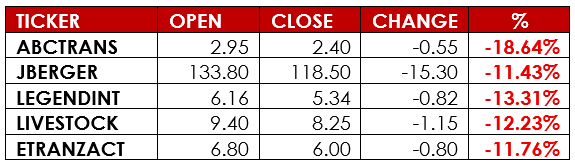

Notable gainers this week were Oando PLC and Lasaco Assurance PLC, while notable losers were Associated Bus Company PLC and Julius Berger Nig. PLC.

We anticipate bullish trading in the Equities market next week following the improved ratings from Fitch and Moody.

CURRENCY

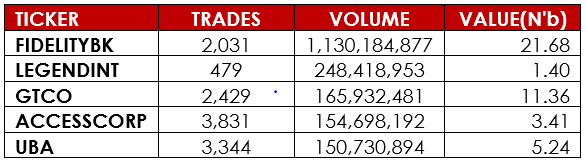

TOP TRADES BY VOLUME

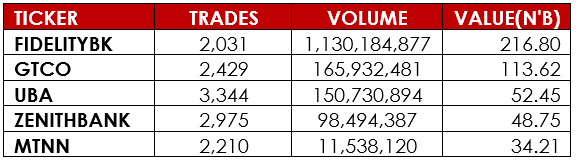

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.