GLOBAL ECONOMY

The US Unemployment rate went up to 4.20% in November 2024 from 4.10% in October as the number of unemployed individuals increased by 161,000 to 7.15 million, while employment levels decreased by 355,000 to 161.14 million. Non-Farm Payrolls however, increased to 227,000 in November 2024. US initial jobless claims rose to 224,000 for the week, from 213,000, as the four-week moving average for the US initial jobless claims, rose to 218,250 from a revised 217,500 in the previous week. Despite this rise in Jobless Claims, the results still support the view that the US labor market remains at historically strong levels despite the aggressive tightening cycle by the Federal Reserve in the last quarter.

The UK 10-year gilt yield edged up toward 4.30%, driven by safe-haven demand after South Korea briefly declared martial law, sparking global market tension before lifting it hours later. Meanwhile, Bank of England Governor Andrew Bailey hinted at potential rate cuts if inflation continues to decline, suggesting up to four 25bps reductions over the next year, which could lower the key interest rate to around 3.75% as inflation has declined faster than the BoE projected.

The Euro hovered near €1/$1.06, amid political turmoil in France and anticipation of upcoming European Central Bank (ECB) decisions. President Macron promised to appoint a new prime minister to secure parliamentary approval for the 2025 budget, calming markets after fears of deeper instability. Meanwhile, the ECB is expected to cut rates by 25bps next week, marking its fourth reduction this year as it aims to bring inflation under control. ECB President Christine Lagarde recently outlined a cautious approach, favoring steady cuts to support recovery while monitoring risks.

China’s foreign exchange reserves rose by $4.80billion to $3.27trillion in November 2024, and up from $3.26trillion in October. The increase occurred as the US dollar appreciated against other currencies. Last month, the yuan depreciated by 1.80% against the dollar, while the dollar strengthened by 1.80% against a basket of other major currencies. China’s 10-year government bond yield dropped to almost 2.00%, amid expectations of expanded stimulus from Beijing to support the economy.

We await the release of the US inflation rate for November as well as the Jobless Claims for the week.

GLOBAL MARKETS

Most US stocks closed higher this week fuelled by a stronger-than-expected November jobs report that raised optimism about a Federal Reserve rate cut later this month. The Nasdaq and S&P 500 indices closed positive, increasing by 3.31% and 0.96% to 21,622.25 and 6,090.27, while the Dow Jones index fell slightly by -0.60% to 44,642.52.

Stocks in Europe closed higher this week as Traders shrugged off concerns about the political situation in France, also due to the release of a stronger-than-expected US jobs report that supported the view of a gradual rate-cut by the US Federal Reserve. The London’s Financial Times Stock Exchange (FTSE) 100, Germany’s Deutscher Aktien (DAX) and Cotation Assistée en Continu (CAC) 40 indices all closed positive, increasing by 0.26%, 3.86% and 2.65% to 8,308.61, 20,384.61 and 7,426.88, respectively.

Major Asian stocks closed higher on hopes that Chinese authorities will introduce additional economic support measures at a key policy meeting next week. Investors are particularly focused on the upcoming Central Economic Work Conference, which will outline China’s economic priorities and targets for 2025. However, sentiment remains cautious due to ongoing economic uncertainties in China and escalating trade tensions with the US. The Hang Seng and Topix indices increased by 2.28% and 1.73% to close at 19,865.85 and 2,727.22, respectively.

We expect the bullish sentiments in the Global Equities market to persist next week.

DOMESTIC ECONOMY

The Nigerian Senate has officially approved the 2025–2027 Medium-Term Expenditure Framework and Fiscal Strategy Paper (MTEF-FSP), setting the stage for a ₦47.90trillion budget proposal for 2025. The proposed budget includes ₦16.40trillion allocated to capital projects, while ₦14.20trillion is earmarked for recurrent expenditure. This 2025–2027 MTEF-FSP serves as a guide for budgeting and economic planning over the next three years.

The National Bureau of Statistics Foreign Trade Statistics report released this week showed that Total exports for Q3 2024 reached ₦20.49trillion, representing a 98% increase from ₦10.35trillion in the same period last year. This also marks a 16.76% rise from ₦17.55trillion in the second quarter of 2024. On the import side, Nigeria’s total import bill for Q3 2024 was ₦14.67 trillion, a 62.30% rise from ₦9.04trillion in Q3 2023. This indicates a trade surplus of ₦5.82trillion in the third quarter of 2024, driven by a significant increase in export earnings. China remained Nigeria’s largest import partner, followed by India, Belgium, the United States, and Malta as key imports included motor spirit, gas oil, durum wheat, and used vehicles.

The Stanbic IBTC Bank Nigeria PMI rose to 49.60 in November 2024, up from 46.90 in October 2024. This was primarily due to the return to growth of new orders in November, after having decreased in October. Meanwhile, companies reduced both their purchasing activity and stocks of inputs amid steep price pressures. Higher energy prices, increases in the cost of raw materials, and currency weakness were cited as the main factors.

The Governments of Nigerian President Bola Tinubu and French President Emmanuel Macron have committed to engaging in several financial and technical assistance programs worth over €300million, aimed at supporting various investments in Nigeria. This was disclosed in a statement signed by Bayo Onanuga, Special Adviser to the President (Information & Strategy). The commitment is part of two agreements signed by the counterparts on Thursday in Paris, France, aimed at fostering a partnership focused on the development of critical infrastructure and the long-term sustenance of agriculture and food security.

We expect further appreciation in the Naira amid improved supply and weaker demand as official trading resumes next week.

DOMESTIC MARKETS

Nigeria has raised $2.20billion through its latest Eurobond auction, marking a crucial moment in the country’s ongoing efforts to address its growing fiscal deficit. Nigeria recorded a total subscription of over $9billion, while only $2.20billion was allotted. The allotments are $700million for the 6.5-year bond priced at 9.625% and $1.50billion for the 10-year bond priced at 10.375%. The bonds were issued under the Regulation S/144A structure, making them available to both U.S. and international investors.

The CBN introduced the “BMATCH” trading platform, driving improved liquidity throughout the week. Exchange rates ranged between $/₦1,550 and $/₦1,693, with the Naira progressively strengthening. The Naira appreciated steadily due to increased supply from exporters and foreign portfolio investors and weak import demand. The NAFEX rate closed the week at $1/₦1,535.00, marking a significant improvement from the previous sessions.

MONEY MARKET AND FIXED INCOME

System liquidity improved slightly at the start of the week, driven by FAAC disbursements, Remita inflows, and other market credits. However, liquidity tightened following Treasury Bills and OMO Auction settlements, with the liquidity position closing at ₦632.38billion. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) decreased by -2.14% and -2.33% to 27.67% and 28.17% from 29.81% and 30.50% last week, respectively.

The Nigerian Treasury Bills (NT-Bills) market average yield increased by 56bps to 25.82% against 25.26% the previous week. In the Bonds market, the average yield for the Short-tenor and the Long-tenor Bonds increased by 4bps and 1bp to 19.89% and 17.89%, respectively, while the average yield for the Medium-tenor Bonds remained unchanged at 19.85% on a week-on-week basis.

The Federal Government offered ₦583.26billion at its Treasury Bills Auction which held this week on Wednesday, 4th December 2024. The 364-day stop rate decreased by 57 bps to 22.93%, prompting increased secondary market activity, especially for the newly issued 1-year bill. The 91-day and 182-day bills remained the same at 18.00% and 18.50% respectively.

We anticipate cautious trading next week as investors focus on the upcoming NTB auction, which is expected to offer ₦275.71billion across tenors.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 0.72% to close at ₦59.53trillion from ₦59.11trillion and 98,210.75 from 97,506.87 the previous week.

A total of 3.89billion shares worth ₦87.75billion in 43,868 deals were traded this week, compared to 3.19billion shares worth ₦54.85billion in 45,112 deals traded last week. On a sectoral basis, the Banking, Insurance, Consumer Goods, Oil and Gas and Industrial Goods indices all closed positive at 1.30%, 10.50%, 0.13%, 4.84% and 2.52% respectively.

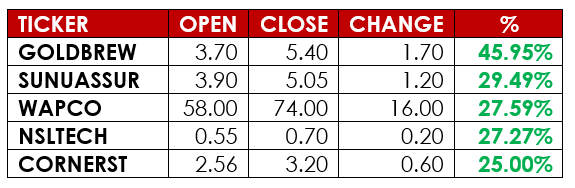

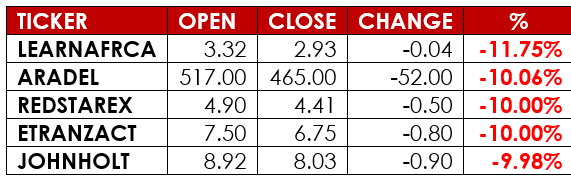

Notable gainers this week were Golden Guinea Breweries Plc and Sunu Assurances Nigeria Plc, while notable losers were Learn Africa Plc and Aradel holdings Plc.

We expect mixed sentiments in the Equities market, as participants position themselves for a potential rally and focus on the NTB auction holding next week.

CURRENCY

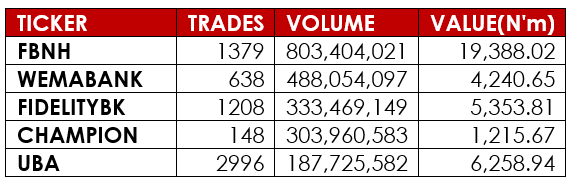

TOP TRADES BY VOLUME

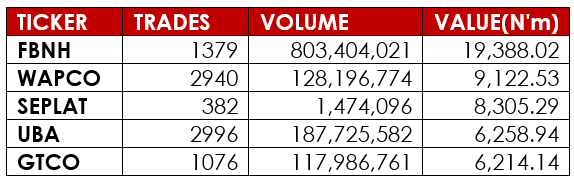

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research