GLOBAL ECONOMY

The US economy Non-Farm Payroll Report showed that 143,000 jobs were added in January 2025, below 307,000 in December and forecasts of 170,000. Job gains occurred in health care (44,000), retail trade (34,000), and social assistance (22,000). Also, the US unemployment rate fell by 0.10% point to 4.00% in January 2025, compared to 4.10% in the previous month. The number of unemployed individuals declined by 37,000 to 6.85 million, while employment went up by 2,234 to 163.9 million.

The Bank of England (BoE) cut its benchmark Bank Rate by 25bps to 4.50% in its February 2025 meeting, as expected. All nine members of the Monetary Policy Committee voted for a rate cut, while two members voted for a steeper 50bps cut. The Bank maintained its stance that monetary easing is expected to be gradual this year, but revised its growth forecasts for the current year downward as economic activity has already underperformed compared to expectations from November.

The Euro weakened to €1/$1.02, as US President Donald Trump’s new trade tariffs sparked concerns in Europe as Trump also threatened tariffs on the EU, citing the US trade deficit with Europe. While Canada reacted and Mexico may follow, the EU vowed to respond firmly to any US tariffs. This uncertainty, combined with the European Central Bank’s dovish stance and the possibility of further rate cuts, added downward pressure on the euro.

The Caixin China General Manufacturing PMI stood at 50.10 in January 2025, less than December’s print of 50.50. It was the fourth straight month of growth in factory activity, but the slowest, as foreign orders shrank amid rising challenges in global trade policies. Employment fell the most, but conversely, output rose alongside buying levels, helped by better delivery times, allowing firms to grow stocks of purchases. On the cost side, input prices stabilized, with supplier discounts offsetting rising raw material costs.

Next week in the US, investors will focus on the CPI report and Fed Chair Powell’s testimony before Congress. Key economic releases include Producer Prices, Retail Sales, and Industrial Production.

GLOBAL MARKETS

US stocks declined on Friday as Investors responded to the potential for additional tariffs from the Trump administration, while also processing an increase in inflation expectations and low jobs report. Compared to last week, the Nasdaq index rose slightly by 0.06% to 21,491.31 while the S&P 500 and Dow Jones indices decreased by -0.24% and -0.54% to 6,025.99 and 44,544.66, respectively.

UK major stock indices closed higher this week, compared to last week, driven by positive Investor reaction to the Bank of England’s (BoE) interest rate cut and its dovish outlook despite retreating from a recent record high during the week. The London’s Financial Times Stock Exchange (FTSE) 100, France Cotation Assistée en Continu (CAC) 40 and Germany’s Deutscher Aktien (DAX) indices increased by 0.31%, 0.29% and 0.25% to 8,700.53, 7,973.03 and 21,787.00, respectively.

Chinese stocks rally was fueled by strong gains in artificial intelligence and robotics stocks, driven by excitement surrounding Chinese AI startup DeepSeek’s breakthrough. At the same time, concerns over a global trade war eased, due to Beijing’s countermeasures against the 10% tariffs imposed by the Trump administration on Chinese goods. The Hang Seng index increased by 4.49% to 21,133.54 while the Japanese Topix index fell by -1.84% to 2,737.23.

We expect traders to focus on the US Inflation report and further speeches from Fed Chairman Powell.

DOMESTIC ECONOMY

The Stanbic IBTC Bank Nigeria Purchasing Managers’ Index (PMI) was 52.00 for January 2025. While lower than December’s PMI at 52.70, the index remained above the 50.00 mark, signaling continued expansion in the private sector. The data shows that business activity and new orders grew for the second consecutive month, boosted by improving customer demand. There were increases in output and new orders, although slightly lower than the levels in December 2024. Inflationary pressures eased, with input costs and output prices rising at a much slower rate than in December.

The Gross Domestic Product Per Capita Income in Nigeria has declined to $835.49 in 2025, a 4.74% fall from $877.07 in 2024, an indication of further shrinking of the living standards of citizens, according to new data from the International Monetary Fund (IMF). This drop highlights the continued erosion of household incomes amid the rapid cost-of-living crisis. Gross Domestic Product is the measure of a country’s overall economic activity, while the GDP per capita measures the average standard of living of a country’s citizens. The IMF, however, projects a rise in 2026 and 2027, with the GDP per capita expected to cross the $1,000 mark in 2028.

President Bola Tinubu has revised the proposed 2025 budget upwards, increasing it from ₦49.70trillion to ₦54.20trillion. The adjustment comes on the back of additional revenue inflows from key government agencies, strengthening the government’s fiscal position. In separate letters sent to both the Senate and the House of Representatives, the revenue surpluses from various government bodies were stated as the primary drivers of the adjustment. The revenue boost includes ₦1.40trillion from the Federal Inland Revenue Service (FIRS), ₦1.20trillion from the Nigeria Customs Service (NCS) and ₦1.80trillion from other government-owned agencies. These additional funds have provided the government with the fiscal room to expand the budget and address critical national priorities.

Nigeria’s Foreign Exchange (FX) reserves declined significantly by $1.16billion in January 2025, as the figures from the Central Bank of Nigeria (CBN) show that reserves fell from $40.88billion at the end of December to $39.72billion as of January 31, 2025. This marks the sharpest monthly decline since April 2024 and raises concerns about the country’s external liquidity position. This drop represents a 2.84% decline, with apprehensions about the country’s ability to sustain external obligations, including debt repayments and import financing. It also follows CBN’s increased dollar sales to Bureau De Change (BDC) operators as part of efforts to stabilize the naira amid ongoing currency volatility.

We expect further strengthening of the Naira, as CBN approves an extension of FX sales to Bureau De Change (BDC) operators.

DOMESTIC MARKETS

The Federal Government has announced plans to issue bonds worth ₦758billion, after approval from the Debt Management Office (DMO) to settle outstanding pension debts. This was revealed by Wale Edun, the Minister of Finance and Coordinating Minister of the Economy, on Tuesday at the 23rd Federal Executive Council meeting in Abuja. He explained that these bonds will clear debts from the old Defined Benefit Scheme, which existed before the Contributory Pension Scheme was introduced in 2004.

MONEY MARKET AND FIXED INCOME

System liquidity opened short at the start of the week, driven by OMO auction settlements from the previous week and further declined due to settlements from the Treasury Bills auction held on Wednesday. Consequently, the Open Repo Rate (ORR) and Overnight Rate (O/N) increased by 328bps and 318bps to 32.42% and 32.75%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 84bps to 22.52% against 23.36% last week. In the Bonds market, the average yield for the Short-tenor and Medium-tenor Bonds decreased by 17bps and 22bps to 21.06% and 20.50%, while the average yield for the Long-tenor Bonds remained unchanged at 18.73%.

The Federal Government Treasury Bills Auction was held on Wednesday, 5th February 2025, with an offer size of ₦670billion across tenors. Total subscription was 4.80x the total offer, at ₦3.22trillion, and total allotment was ₦670billion. The stop rate for the 91-day and 182-day bills remained unchanged at 18.00% and 18.50% while the stop rate for the 364-day bill decreased by 148bps to 20.32%.

We anticipate increased activity in the Bonds market as Investors shift their interest from the Treasury Bills market in expectations of higher yields.

THE EQUITIES MARKET

Market Capitalization and All-Share Index increased by 1.37% and 1.38% to close at ₦65.59trillion from ₦64.71trillion and 105,933.03 from 104,496.12 the previous week.

A total turnover of 3.05 billion shares worth ₦98.35billion in 72,535 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 3.25 billion shares valued at ₦69.20billion that exchanged hands last week in 77,270 deals. On a sectoral basis, the Banking, Oil and Gas, Insurance and Industrial Goods indices closed positive this week, at 4.66%, 0.56%, 1.61% and 0.85%, while the Consumer Goods index was the sole loser, closing at -0.60%.

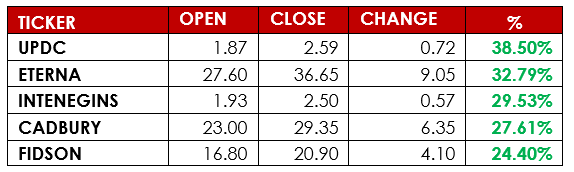

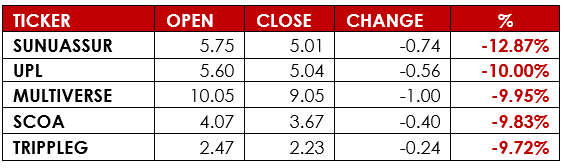

Notable gainers this week were UPDC Plc and Eterna Plc, while notable losers were Sunu Assurance Plc and University Press Plc.

We expect the Bullish sentiments to persist next week, as more companies release their financial statements for the year ended December 2024.

CURRENCY

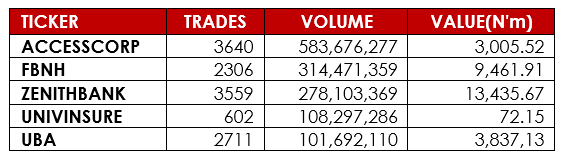

TOP TRADES BY VOLUME

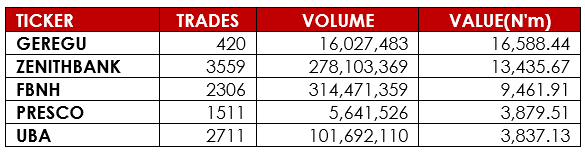

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, BusinessDay, Economic Confidential, Alpha10 Research