GLOBAL ECONOMY

The US unemployment rate rose to 4.10% in February 2025, up from 4.00% in January and above market expectations of 4.00%, as the number of unemployed individuals increased by 203,000 to 7.05 million, while employment declined by 588,000 to 163.31 million. Exports of goods and services from the U.S. increased by $3.30billion from the previous month, reaching $269.80billion in January 2025, primarily driven by a $2.70billion boost in goods shipments.

Global UK Services PMI rose to 51.00 in February 2025 from 50.80 in the previous month. Despite the activity growth, service providers recorded lower sales volumes for February, with firms citing cutbacks to business investment for clients due to higher economic uncertainty and headwinds against consumer spending. Additionally, sales to foreign consumers fell. The Global UK Composite PMI dipped slightly to 50.50 in February 2025, down from 50.60 in January, signaling marginal economic growth. Expansion in the services sector continued to offset a sharp decline in manufacturing output. Meanwhile, new business volumes fell, reflecting weak demand across both manufacturing and services.

The European Central Bank (ECB) lowered the three key interest rates by 25bps, as expected, reducing the deposit facility rate to 2.50%, the main refinancing rate to 2.65%, and the marginal lending rate to 2.90%. This decision reflects an updated assessment of the inflation outlook and monetary policy conditions. The ECB acknowledges that monetary policy is becoming less restrictive, easing borrowing costs for businesses and households.

China introduced tariffs on US goods and other trade measures on Tuesday in response to US President Donald Trump’s move to raise tariffs on all Chinese imports to 20% from 10%. China’s Finance Ministry announced a 15% tariff on US chicken, wheat, corn, and cotton, while soybeans, sorghum, pork, beef, fruits, vegetables, seafood, and dairy will face a 10% tariff. These measures will take effect on March 10, 2025. Meanwhile, China’s trade surplus surged to $170.52billion in January-February 2025, up from $125.16billion in the same period last year. The sharp increase was largely driven by an unexpected 8.40% fall in imports year-on-year, amid weakening domestic demand at the start of the year. Meanwhile, exports grew 2.30%, slowing significantly from December’s 10.70% increase.

Next week in the US, Investors will closely watch the US inflation rate, producer inflation and the JOLTS job openings for insights into the American economy.

GLOBAL MARKETS

US stocks continued to sell off on Friday, as the uncertainty surrounding Trump’s trade policies increased concerns, while investors showed more skepticism on the future of AI returns. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices decreased by -3.27%, -3.10% and -2.37% to 20,201.37, 5,770.20 and 42,801.72.

In the UK, investors digested a slightly weaker-than-expected US non-farm payrolls report amid confusion about Donald Trump’s tariff plans as the U.S. President signed executive actions on Thursday, postponing tariffs on goods from Mexico and Canada until April 2nd, 2025. The London’s Financial Times Stock Exchange (FTSE) 100 decreased by -1.47% to 8,679.88 while Germany’s Deutscher Aktien (DAX) and France Cotation Assistée en Continu (CAC) 40 indices increased by 2.03% and 0.11% to 23,008.94 and 8,120.80, respectively.

In Asia, Investors bought the dip in Chinese technology and artificial intelligence stocks. China also highlighted its policies to stimulate economic growth, emphasizing plans to advance technological innovation and boost domestic consumption, among other initiatives. The Hang Seng and Topix indices increased by 5.62% and 0.99% to 24,231.30 and 2,708.59, respectively.

We expect cautious trading in the Global Equities market as Investors reassess the impact of Trump’s Trade Tariffs deferral, amidst simmering trade war between the US and China.

DOMESTIC ECONOMY

The Private Sector Purchasing Managers Index (PMI) rose to 53.70 in February, up from 52.00 in January, marking the highest level since January 2024. A PMI reading above 50.00 indicates an expansion in business activity, while a reading below 50.00 signals a contraction. Output levels increased, with businesses attributing the increase to stronger demand conditions, as new orders rose at the sharpest pace in over 12 months. The agriculture, manufacturing, services, and wholesale & retail sectors all recorded growth in output. This is supported by a relatively stable exchange rate and moderation in fuel prices leading to easing in inflationary pressures.

Nigeria, alongside nine other African countries, accounts for 69.00% of Africa’s total external debt stock, according to a new report by the African Export-Import Bank (AFREXIM). The report highlights Nigeria’s significant debt burden, placing it among the top three most indebted countries, with 8.00% of Africa’s total external debt. South Africa is the largest debtor with 14.00%, followed by Egypt at 13.00%, Morocco and Mozambique at 6.00% each, while Angola holds 5.00%. The report attributes the high levels of debt to external borrowing driven by underdeveloped financial markets, volatility in foreign exchange earnings, and the need for infrastructure financing. Nigeria’s share of Africa’s external debt highlights its reliance on international borrowing to finance budget deficits and critical infrastructure as the country has consistently accessed Eurobond markets, concessional loans from multilateral institutions, and other external financing options to bridge revenue gaps.

Nigeria has officially joined the European Bank for Reconstruction and Development (EBRD) as its 77th shareholder. This membership follows a pivotal decision made at the EBRD’s 2023 Annual Meeting in Samarkand, Uzbekistan where an amendment to the agreement establishing the EBRD was approved, permitting the gradual expansion of the bank’s operations to sub-Saharan Africa and Iraq. As a beneficiary, Nigeria would gain access to the EBRD’s financial resources and policy support, fostering sustainable development.

Nigeria’s foreign exchange reserves dropped by $1.31billion in February 2025, reflecting ongoing external pressures. According to data from the Central Bank of Nigeria (CBN), the reserves declined from $39.72billion on January 31, 2025, to $38.42billion on February 28, 2025, marking a 3.27% drop within the month. The decline leads to speculations about the Central Bank’s strategy in managing foreign exchange (FX) market liquidity and ensuring exchange rate stability.

We await the release of inflation figures for February 2025 next week.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

Interbank liquidity remained positive throughout the week, supported by OMO maturities and FAAC inflows, however, it declined as a result of a CBN OMO auction, which saw allotments of ₦1.677trillion, increasing funding pressure and driving borrowing rates higher, opening on Friday at a deficit of -₦1.32trillion compared to a positive balance of ₦130.94billion last week. Consequently, the Open Repo Rate (ORR) and the Overnight Rate (O/N) increased by 33bps and 34bps to 27.08% and 27.67%, respectively.

The Nigerian Treasury Bills (NTB) market average yield decreased by 103bps to 18.85% against 19.88% last week. In the Bonds market, the average yield for the Short-tenor and Medium-tenor Bonds increased by 1bp and 3bps to 19.23% and 18.56%, while the average yield for the Long-tenor Bonds remained unchanged at 17.60%.

The Nigerian Treasury Bills Auction held this week, with an offer of ₦650billion across tenors. The total subscription was ₦1.92trillion and total allotment was ₦830.44billion, thus, the auction was oversold by ₦180.44billion. Stop rates decreased by 25bps and 61bps to 17.75% and 17.82% for the 182-day and 364-day bills, while the stop rate for the 91-day bill remained unchanged at 17.00%.

We anticipate the Nigerian Treasury Bills auction scheduled to hold next week, where ₦550billion will be offered across the 91-day, 182-day and 364-day tenors, against ₦162.17billion maturing.

THE EQUITIES MARKET

Market Capitalization and All-Share Index decreased by -0.71% and -1.19% to close the week at ₦66.72trillion from ₦67.19trillion and 106,538.60 from 107,821.39 the previous week.

A total turnover of 1.82 billion shares worth ₦47.23billion in 64,222 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 1.85 billion shares valued at ₦51.39billion that exchanged hands last week in 63,090 deals. On a sectoral basis, the Banking, Insurance, Consumer Goods, Oil and Gas and Industrial Goods indices all closed negative this week, at -2.87%, -2.33%, -1.72%, -0.19% and -0.01%, respectively.

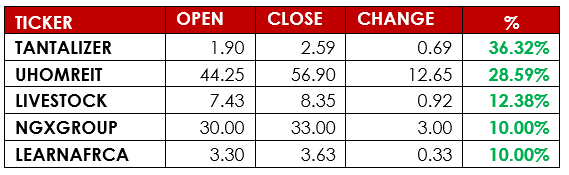

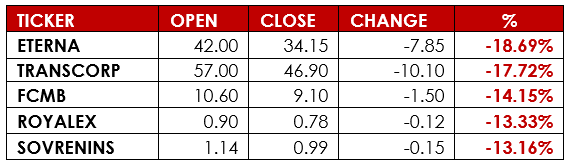

Notable gainers this week were Tantalizers Plc and UH Real Estate Investment Trust Plc, while notable losers were Eterna Plc and Transnational Corporation Plc.

CHANGE OF NAME

The change of name of FBN HOLDINGS PLC (the Company) to FIRST HOLDCO PLC has been implemented by Nigerian Exchange Limited. This is in line with the approval obtained from the shareholders of the Company at its Annual General Meeting held on 14 November 2024 and the receipt by the Company of a new certificate of incorporation from the Corporate Affairs Commission. The Company’s trading symbol has also been changed from FBNH to FIRSTHOLDCO.

We anticipate market participants will stay cautious, though interest may emerge at attractive entry points amid earnings releases and potential corporate actions.

CURRENCY

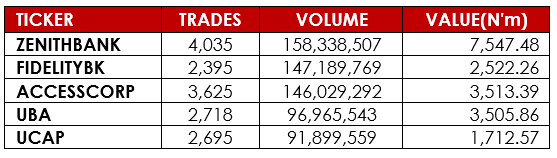

TOP TRADES BY VOLUME

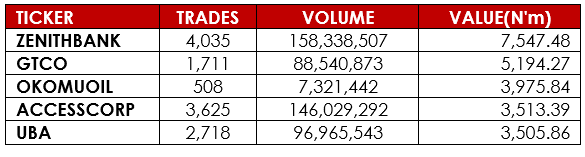

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.

Sources: Investing.com, Trading Economics, Market Insider, CBN, DMO, NBS, NGX, AIICO, Nairametrics, Alpha10 Research