GLOBAL ECONOMY

The US trade deficit narrowed to $60.20billion, the lowest since 2023, as imports dropped by 3.70% and exports fell by 0.50%. Manufacturing orders plunged 4.80% in June, led by a 51.80% drop in aircraft orders, while the Logistics Manager’s Index fell to 59.20, signalling slower inventory growth. President Trump announced sweeping tariffs, up to 250% on pharmaceuticals and 100% on semiconductors, as he also nominated Stephen Miran to the Federal Reserve Board and plans to appoint an interim Fed. Governor.

The British Pound strengthened to £1/$1.34 as the Bank of England cut interest rates by 25bps to 4.00% in a split 5–4 vote. The UK Composite Purchasing Managers Index (PMI) eased to 51.50, with Services expanding modestly (51.80) and Manufacturing contracting (48.00), while private sector employment saw its sharpest drop since February. Inflation is now expected to peak at 4% in September, while growth forecasts for 2025 were revised up to 1.25%. Following the rate cut, though, markets now expect only one more cut this year.

The Euro strengthened above €1/$1.16 amid expectations of slower European Central Bank (ECB) easing, while inflation held steady at 2.00%, matching the ECB’s target. The Hamburg Commercial Bank (HCOB) Composite PMI rose to 50.90, driven by services growth (51.00) and near-stabilisation in manufacturing (49.80). Employment increased for the first time in five months, while input cost inflation eased. Producer prices rose 0.80% month-on-month in June, ending a three-month decline, with annual inflation accelerating to 0.60%, led by energy and consumer goods.

The offshore Yuan edged lower to around ¥7.18/$1, as Investors grew cautious ahead of upcoming inflation data. Exports surged 7.20% year-on-year to $321.80billion from $316.10billion in May, driven by strong shipments to the Association of Southeast Asian Nations (ASEAN) (+16.o6%), Taiwan (+19.20%), and the EU (+9.20%), while exports to the U.S. fell 21.70%. Imports rose 4.10%, lifting the trade surplus to $98.24billion. The current account surplus hit a record $135.10billion in Q2, supported by a goods trade surplus of $219.10billion. The People’s Bank of China (PBoC) pledged to maintain loose monetary policy and formed a financial stability committee to manage risks as S&P affirmed China’s A+ credit rating with a stable outlook, citing strong fiscal support.

Next week, Investors will focus on US–China trade tensions ahead of the August 12 tariff deadline, a possible Trump–Putin meeting on Ukraine-Russia War and key global economic data, including US inflation and retail figures.

GLOBAL MARKETS

This week, US stocks closed high with gains on major stocks driven by strong corporate earnings released and growing optimism about possible interest rate cuts from the Federal Reserve. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices closed higher, increasing by 3.87%, 2.43% and 1.35% to close the week at 21,450.02, 6,389.45 and 44,175.61, respectively.

In the UK and across Europe, major stocks closed positively; however, losing some initial gains following the Bank of England’s rate cut by 25bps to 4.00% in a divided vote, highlighting concerns for inflation, particularly Food Inflation. London’s Financial Times Stock Exchange (FTSE) 100, Germany’s Deutscher Aktien (DAX) and France Cotation Assistéeen Continu (CAC) 40 indices increased by 0.30%, 3.15% and 2.61% to 9,095.73, 7,743 and 24,162.86, respectively.

The Asian stock market closed higher this week, with major stocks closing positive as the market struggled for momentum, with Investors awaiting key inflation figures that could provide fresh insights. The Hang Seng and Topix indices increased by 1.43% and 2.56% to 24,858.82 and 3,024.21, respectively.

Next week, Investors will monitor US–China trade talks and more earnings reports to guide sentiments.

DOMESTIC ECONOMY

Nigeria’s Money Supply Falls to ₦117.40trillion in June Amid Tight Liquidity and FX Pressure

Nigeria’s broad money supply (M3) declined for the third straight month in 2025, dropping 1.27% to ₦117.40trillion in June from ₦119trillion in May, according to the Central Bank of Nigeria (CBN). Despite the monthly dip, year-on-year growth stood at 15.81%, up from ₦101.40trillion in June 2024. The decline reflects tight liquidity conditions, driven by monetary tightening and reduced government spending. Net foreign assets fell to ₦40.70trillion, while net domestic assets rose to ₦76.80trillion, partially offsetting the external contraction. M2 and M1 also declined, signalling reduced cash availability and early success in curbing inflation through high interest rates and aggressive Open Market Operations (OMO).

FDI into Nigeria Plunges 70% in Q1 2025 Despite Surge in Capital Inflows

Despite a 67% surge in total capital importation to $5.64billion in Q1 2025, Foreign Direct Investment (FDI) into Nigeria plunged by 70.06% quarter-on-quarter to $126.29million, down from $421.88million in Q4 2024, according to the National Bureau of Statistics (NBS). This sharp decline underscores a growing preference among foreign investors for short-term, high-yield instruments such as Open Market Operation (OMO) bills and Treasury Bills, which accounted for $4.21billion (74.6%) of total inflows. FDI made up only 2.24% of total capital inflows, reflecting waning long-term investor confidence and raising concerns about the sustainability of Nigeria’s economic growth. Equity investments comprised $124.31million of the FDI, while “other capital” contributed $1.98million. Although the naira stabilised below ₦1,550/$, analysts warn that Nigeria’s reliance on volatile “hot money” leaves it vulnerable to external shocks, emphasising the urgent need for structural reforms to attract stable, growth-oriented investment.

Nigeria’s Oil Output Hits 1.78 Million barrels per day (bpd), Meets OPEC Quota Amid Security Gains.

Nigeria’s oil production surged to an average of 1.78 million barrels per day (bpd) in July 2025, surpassing 1.80 million bpd at peak, driven by enhanced security in the Niger Delta. This marks a significant recovery, with June output at 1.51 million bpd, meeting OPEC’s quota for the second time this year. Despite challenges like oil theft and underinvestment, gas production rose to 7.58 billion standard cubic feet per day, while crude sales dipped to 21.68 million barrels. The Nigerian National Petroleum Company Limited (NNPCL) reported ₦4.57trillion in revenue and ₦905billion profit in June. Meanwhile, eight OPEC+ nations plan to raise output by 547,000 bpd in September, signalling improved global oil market conditions.

Private Sector Credit in Nigeria Drops to ₦76.12 Trillion Amid Tight Monetary Conditions.

Nigeria’s private sector credit fell to ₦76.12trillion in June 2025, marking the fourth monthly decline this year, according to the Central Bank of Nigeria (CBN). This represents a ₦1.60trillion drop from May and a continued downward trend since February, despite a brief rebound in April. While year-on-year credit rose from ₦73.20trillion in June 2024, analysts warn that the repeated monthly declines reflect liquidity constraints, high interest rates, and tight lending criteria. With the benchmark MPR at 27.50%, borrowing has become more expensive, especially for SMEs. The slowdown in credit growth could hamper investment, job creation, and GDP expansion, despite government interventions like the Nigerian Consumer Credit Corporation. Sectoral data shows Manufacturing, Commerce, and Oil & Gas remain top recipients, while Agriculture lags.

Nigeria’s Economy Rebased to ₦372.80trillion GDP, Revealing Stronger Services and Real Estate Growth.

Nigeria’s rebased Gross Domestic Product (GDP) now stands at ₦372.80trillion for 2024, a 35.40% increase from previous estimates, according to the National Bureau of Statistics (NBS). The rebasing reflects a more accurate economic structure, with the Services sector expanding to 53.10%, Agriculture rising to 25.80% and Industry declining to 22.10%. Real estate emerged as the third-largest contributor, behind Crop Production (17.60%) and Trade (17.40%). In Q1 2025, real GDP grew 3.13%, driven by the Non-oil sector, which accounted for 96% of GDP. Fastest-growing sectors include Finance & Insurance (15%), Transportation (14.10%), and ICT (7.40%). The rebasing incorporates high-growth areas like fintech and creative industries, enhancing planning, Investor confidence, and alignment with global standards.

Next week, we anticipate the release of the Inflation figure for July 2025 by the NBS on 15th August 2025.

EUROBOND MARKET

The Sub Sahara African Eurobond market traded bullish at the start of the week, as strong early buying momentum drove yield declines across maturities. Nigerian Eurobonds mirrored this bullish trend, further supported by the CBN’s announcement of the settlement of all outstanding FX forwards, which boosted Investor confidence in Nigeria’s economic reforms and spurred a rally. Midweek, we saw profit-taking as Investors were cautious following Trump’s announcement of more tariffs and the upcoming deadline of the US-China tariff pause. Consequently, the average benchmark yield fell 21bps w/w to 8.04%.

We expect activities next week to be determined by global risk sentiments on U.S. rate expectations, oil price movements and developments from the tariff war.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System liquidity closed positive this week at ₦750.31billion. Consequently, the Short-term rates closed low, as the Open Repo Rate (ORR) remained unchanged at 26.50% while the Overnight Rate (O/N) increased by 10bps to 27.00% respectively.

The Nigerian Treasury Bills (NTB) market average yield increased week-on-week by 15bps to 16.42%. The Bonds market traded mixed through the week. Early sessions saw selling pressure in the short to mid-tenor maturities, with notable yield increases on the FGN 2029, FGN 2031 and FGN 2034. The average yield for the short-tenor and mid-tenor bonds increased by 9bps and 17bps to 16.56% and 16.72%, while long-tenor bonds’ average yields decreased by 4bps to 15.70%.

The Nigerian Treasury Bills Auction was held on Wednesday, 6th August 2025. The auction witnessed strong demand for the long tenor bill, as total subscription was 1.67x the total offer, at ₦366.55billion. The bid-to-cover ratio was 2.12x and total allotment was ₦173.25billion, which was lower than the initial offer of ₦220billion; thus, the auction was undersold by ₦46.75billion. Stop rates for the 91-day and 182-day bills remained unchanged, while the 364-day bill increased by 62bps to 16.50%.

We expect current sentiments to persist in the market next week.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalisation appreciated by 3.18% to close the week at 145,754.91 and ₦92.22trillion compared to 141,263.05 and ₦89.37trillion last week.

A total turnover of 8.74 billion shares worth ₦134.58billion in 180,290 deals was traded this week by Investors on the floor of the Exchange, in contrast to a total of 4.85 billion shares valued at ₦149.76billion that exchanged hands last week in 174,267 deals.

On a sectoral basis, Consumer Goods, Industrial Goods, Insurance and Oil and Gas indices closed positive at 8.27%, 8.73%, 41.00%, and 0.17% while the Banking closed negative at -0.75% respectively.

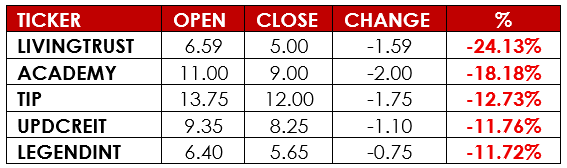

Notable gainers this week were Mutual Benefits Assurance PLC and AIICO Insurance PLC, while Notable losers were Academy Press PLC and Livingtrust Mortgage PLC.

We anticipate bullish sentiments to persist on the back of strong corporate announcements, even as more companies release their earnings reports amidst profit-taking.

CURRENCY

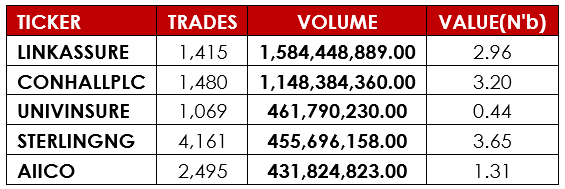

TOP TRADES BY VOLUME

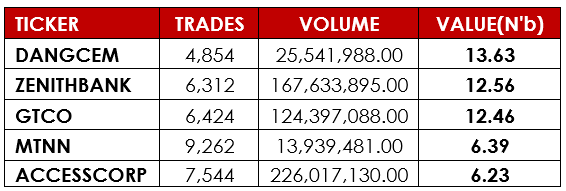

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst utmost care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication.

Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.