GLOBAL ECONOMY

The Federal Reserve (Fed) held lending rates steady at 4.25%–4.50% in May 2025, for the third consecutive meeting amid concerns that President Trump’s tariffs could fuel inflation and hinder growth. Initial jobless claims in the US dropped by 13,000 to 228,000, below the expectation of 230,000 as continuing claims declined by 29,000 to 1,879,000.

The British pound held steady around £1/$1.33 following President Trump’s announcement of a US-UK trade deal. The Bank of England voted to cut the borrowing rate by 25bps to 4.25% in May as expected. The decision had a voting ratio of 5-4, with two members preferring a large cut to 4.00% and the other two members opting for 4.50%. This signals ongoing disinflation, improving inflation expectations as external shocks subside and supportive policies help stabilize prices.

Euro Area Industrial Producer Price Inflation (PPI) slowed to 1.90% year-on-year in March 2025 from 3.00% in February, slightly below expectations of 2.00%. The decline was led by weaker price growth in energy (3.80% vs. 7.60%) and intermediate goods (0.80% vs. 0.90%), while durable consumer goods inflation remained steady at 0.90%. Meanwhile, increases in prices accelerated for capital goods (1.80% vs. 1.70%) and non-durable consumer goods (1.70% vs. 1.60%).

The Yuan fell to around ¥7.24/$1 on Friday as China’s exports grew by 8.10% year-on-year to $315.70billion in April 2025. Also, China’s trade surplus expanded to $96.18billion in April 2025, surpassing the expected $89billion and rising from $72.04billion in April 2024, driven by the 8.10% surge in Exports. The People’s Bank of China announced a 50bps Reserve Requirement Ratio (RRR) cut on May 7, 2025, the first cut of the year and potentially injecting ¥1trillion in liquidity as Beijing aims to support growth amid rising U.S. trade tensions. China’s Producer Prices also dropped 2.70% year-on-year in April 2025, as against the expected 2.60% decline, following a 2.50% fall in March. This decline was driven by rising trade tensions with the U.S. and weak domestic demand.

Next week, Investors will closely monitor the turn out of the trade negotiations between the US and China in Geneva, and the progress of Donald Trump’s announcement of a trade deal with the UK.

GLOBAL MARKETS

US stocks closed negative near the flatline on Friday as Investors looked ahead to high-stakes trade negotiations between the US and China in Geneva this weekend. Compared to last week, the Nasdaq, S&P 500 and Dow Jones indices decreased by -0.27%, -0.47% and -0.16% to 17,928.92, 5,659.91 and 41,249.38, respectively.

In the UK and across Europe, Investors digested upbeat earnings and fresh trade developments. The London’s Financial Times Stock Exchange (FTSE) 100 and the France Cotation Assistée en Continu (CAC) 40 indices both decreased by -0.48% and -0.34% to 8,554.80 and 7,743.75, while the Germany’s Deutscher Aktien (DAX) index increased by 1.79% to 23,499.32.

The Chinese stocks reversed some gains during the week but closed higher compared to last week as Investors were cautious ahead of the Sino-US trade negotiations scheduled for this weekend. The Hang Seng and Topix indices increased by 1.61% and 1.70% to 22,867.74 and 2,733.49, respectively.

We expect cautious trading from Investors as they digest the outcome of the Sino-US trade negotiations.

DOMESTIC ECONOMY

Nigeria Completes $3.40Billion IMF COVID-19 Loan Repayment

Nigeria has fully repaid its $3.40billion IMF loan, which was obtained in April 2020 under the Rapid Financing Instrument (RFI) to address the economic challenges brought on by the COVID-19 pandemic. The IMF confirmed that the final repayment was made on April 30, 2025, marking Nigeria’s exit from this debt obligation. This repayment strengthens Nigeria’s fiscal credibility, potentially boosting investor confidence, reducing reliance on external debt, and improving the country’s global credit standing.

IMF Removes Nigeria from Debtor List

Nigeria has officially exited the IMF’s debtor list, following the full repayment of its outstanding credit obligations. The latest IMF report, published on May 6, 2025, confirms that Nigeria is no longer among the 91 countries with outstanding debt, which collectively owed $117.80billion at the time.

Over the past two years, Nigeria has consistently reduced its IMF debt, reflecting strong fiscal reforms under President Tinubu’s administration. The country’s repayment trajectory has significantly improved, contributing to a healthier debt profile. Nigeria’s full settlement of obligations signals progress in debt management, with potential positive effects on Investor confidence, credit ratings, and fiscal stability.

Nigeria’s Private Sector Purchasing Managers Index (PMI) dips slightly to 54.20 in April 2025

Nigeria’s Private Sector PMI dipped slightly to 54.20 in April 2025 from 54.30 in March 2025, albeit remaining in the region of expansion for the fifth straight month. Output growth surged, marking its best performance since January 2024, while employment hit an eight-month high as firms scaled hiring to meet rising workloads.

Nigeria’s Oil Production Declines by 4.37% in March Below OPEC’s Quota

The Organization of Petroleum Exporting Countries (OPEC) has reported a decline in Nigeria’s oil production following its April Monthly Oil Market Report (MOMR). Nigeria’s crude oil production fell 4.37% in March 2025 dropping to 1.40 million barrels per day (bpd), below its 1.50 million bpd OPEC quota and 32.00% short of the government’s 2025 target of 2.06 million bpd. The decline stems from underinvestment, aging infrastructure, and oil theft, which continues to challenge output stability.

Nigeria’s Business Performance Index rises to +12.29 in April 2025

Nigeria’s Business Performance Index (BPI) climbed to +12.29 in April 2025, improving from +6.58 in March, signaling private sector resilience. Business confidence continues to recover cautiously, fueled by stronger operational outlook, production growth, and macroeconomic stability. However, challenges persist, with power shortages remaining the biggest constraint to business expansion. Other hurdles include high commercial lease costs, limited access to finance, unclear policies, and forex scarcity.

Nigerian Senate Completes Passage of Tax Reform Bills

The Nigerian Senate has approved the final two tax reform bills, marking the completion of legislative work on four key fiscal measures proposed by President Bola Tinubu. The Nigeria Tax Bill 2024 and the Joint Revenue Board Establishment Bill were passed during plenary on Thursday. The next step involves harmonization between the Senate and the House of Representatives before the unified versions are sent to the president for signing into law. These reforms are expected to enhance tax administration, improve revenue collection, and strengthen Nigeria’s fiscal framework.

We await the release of the Inflation report for April 2025 by the National Bureau of Statistics (NBS), on 15th May 2025.

DOMESTIC MARKETS

MONEY MARKET AND FIXED INCOME

System Liquidity remained positive throughout the week, despite the ₦598.33billion NTB settlement. Consequently, short-term rates remained stable, with the Overnight Policy Rate (OPR) unchanged at 26.50%, while the Overnight Rate (O/N) increased slightly by 12bps to close at 26.95%.

The Nigerian Treasury Bills (NTB) market average yield decreased by 5bps to 20.98% last week. In the Bonds market, the average yield for the Short-tenor and Long-tenor Bonds increased by 20bps and 3bps to 19.07% and 17.82%, respectively while the average yield of the Medium-tenor bonds decreased by 7bps to 19.15%.

The Treasury Bills Auction held this week on Wednesday, 7th May 2025. The auction witnessed strong demand, as total subscription was 1.98x the total offer, at ₦1.09trillion. The bid-to-cover ratio was 1.82x and total allotment was ₦598.33billion, slightly above the ₦550billion initial offer. The Stop rates for the 91-day and 182-day bills remained unchanged at 18.00% and18.50%, while the 364-day bills increased by 3bps to 19.63%.

We expect current sentiments to persist next week as Investors cherry-pick high-yield Instruments.

THE EQUITIES MARKET

The NGX All-Share Index and Market Capitalization increased by 2.54%to close the week at 108,733.40 and ₦68.34trillion respectively from 106,042.57 and ₦66.65trillion last week.

A total turnover of 2.65 billion shares worth ₦77.01billion in 86,110 deals was traded this week by investors on the floor of the Exchange, in contrast to a total of 2.20 billion shares valued at ₦75.41billion that exchanged hands last week in 70,329 deals. On a sectoral basis, the Banking, Insurance, Oil and Gas, Consumer Goods and Industrial Goods indices all closed positive, at 3.09%, 0.99%, 3.98%, 5.41% and 1.09%, respectively.

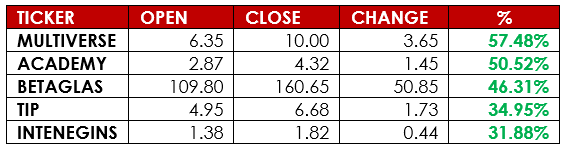

Notable gainers this week were Academy Press Plc and Multiverse Mining and Exploration Plc while notable losers were Meyer Plc and Abbey Mortgage Bank Plc.

We anticipate continued positive momentum, supported by strong earnings reports.

CURRENCY

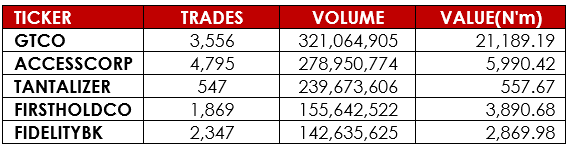

TOP TRADES BY VOLUME

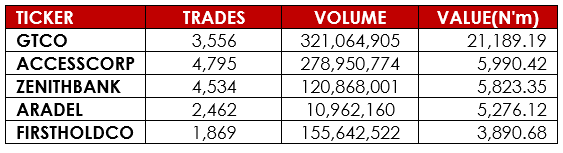

TOP TRADES BY VALUE

TOP GAINERS

TOP LOSERS

DISCLAIMER

This publication is produced by Alpha10 Group solely for the information of users who are expected to make their own investment decisions without undue reliance on any information or opinions contained herein. The opinions contained in the report should not be interpreted as an offer to sell, or a solicitation of any offer to buy any investment. Alpha10 Group may invest substantially in securities of companies using information contained herein and may also perform or seek to perform investment services for companies mentioned herein. Whilst every care has been taken in preparing this document, no responsibility or liability is accepted by any member of the Group for actions taken as a result of information provided in this publication. Alpha10 Group. 13, Mambolo Street, Zone 2, Wuse, Abuja. Visit us at www.alpha10group.com.